The vascular patches market forecast indicates a promising trajectory, fueled by increasing cardiovascular disease prevalence, rising demand for vascular surgeries, and continuous innovation in patch materials and surgical techniques. As healthcare systems across the globe expand and modernize, the use of vascular patches is set to become more integral in treating vascular disorders, particularly in aging populations and regions with high incidence of arterial diseases.

Over the forecast period, the global vascular patches market is expected to witness consistent growth due to several interrelated factors. Among the most significant is the rising global burden of cardiovascular diseases (CVDs), including conditions like atherosclerosis, aneurysms, and peripheral arterial disease. These health issues often require surgical interventions such as carotid endarterectomy and vascular bypass procedures, where vascular patches are used to repair or reconstruct damaged arteries. The increasing frequency of these surgeries directly contributes to the growing demand for vascular patches.

Another key driver forecasted to influence market expansion is the rapid development of healthcare infrastructure in emerging economies. Countries in Asia-Pacific, Latin America, and the Middle East are investing heavily in advanced medical facilities and technologies. As a result, access to complex surgical treatments is improving, creating significant opportunities for vascular patch manufacturers. Markets in India, China, Brazil, and South Africa are expected to witness the fastest growth due to expanding patient populations and government support for cardiac care programs.

From a technological standpoint, innovation in patch materials and designs will continue to shape market dynamics. Manufacturers are expected to introduce next-generation vascular patches that are more biocompatible, resistant to infections, and easier to use in both open and minimally invasive procedures. Bioengineered patches incorporating regenerative properties and tissue integration capabilities are expected to gain traction, especially in high-risk cardiovascular surgeries.

The forecast also reflects a growing trend toward minimally invasive surgeries, where vascular patches that support rapid healing and reduce post-operative complications are in high demand. As surgical techniques evolve to become less invasive and more efficient, there is a growing need for patches that are easy to manipulate, offer reduced suture bleeding, and conform well to natural tissue. This shift in procedural preference is expected to propel innovations in patch construction and performance.

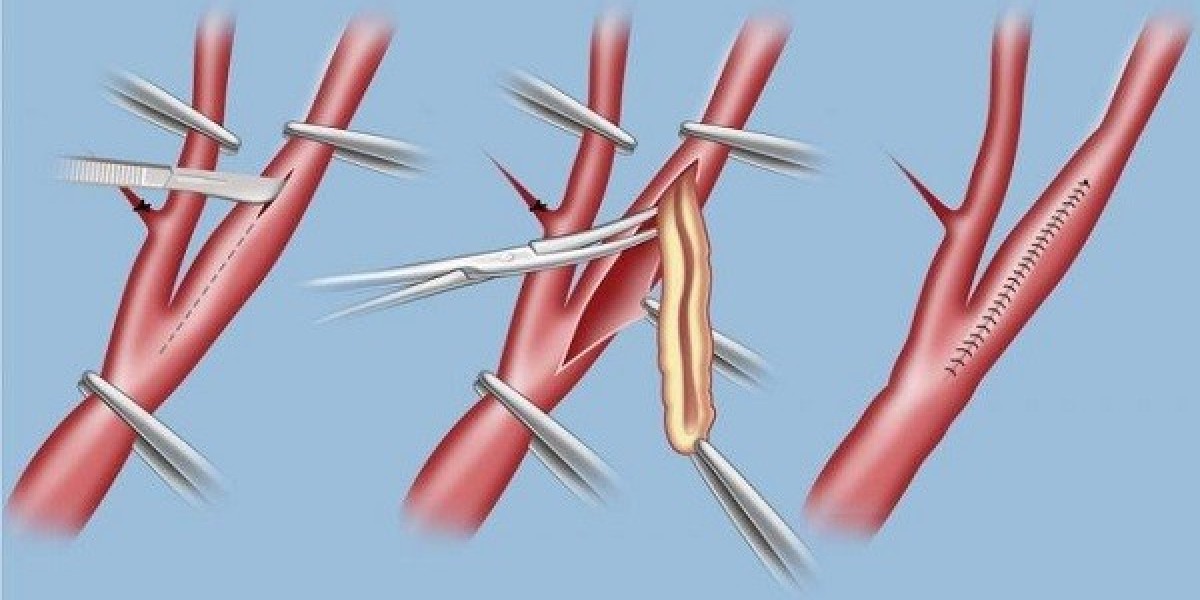

In terms of market segmentation, biologic patches are projected to grow at a faster rate compared to synthetic alternatives. Biologic patches, derived from animal tissues, are often preferred for their superior integration with human tissue and reduced immune response. Although they are typically more expensive than synthetic options, their clinical benefits make them attractive in complex and critical vascular procedures.

From a geographical perspective, North America is expected to maintain a leading position in the vascular patches market during the forecast period. This is primarily due to the presence of advanced healthcare infrastructure, high healthcare expenditure, and strong awareness among surgeons about the advantages of patch angioplasty. The United States is anticipated to be the key contributor within this region.

Europe will also play a significant role, with countries like Germany, France, and the United Kingdom continuing to invest in cardiovascular care and adopting innovative surgical tools. Meanwhile, Asia-Pacific is forecasted to exhibit the highest compound annual growth rate (CAGR) due to an aging population, lifestyle changes increasing CVD risk, and the progressive expansion of healthcare services across both urban and rural areas.

Competitive strategies among manufacturers will also influence the vascular patches market forecast. Companies are likely to focus on expanding their portfolios with technologically advanced products, entering new regional markets, and forging partnerships with hospitals and surgical centers. Mergers and acquisitions may become more common as companies seek to strengthen their positions and leverage synergies to increase market share.

In addition, regulatory environments will continue to shape the market outlook. Countries with streamlined and supportive regulatory systems will likely see faster adoption of new products, while regions with complex approval processes may experience delays in market entry. Therefore, companies will need to align product development and commercialization strategies with regulatory expectations to succeed globally.

Healthcare professionals' training and product familiarity will remain critical for adoption. Educational programs, workshops, and surgeon support are expected to play a growing role in building confidence and increasing the uptake of newer vascular patch solutions, particularly in emerging markets.

In conclusion, the vascular patches market forecast presents a clear picture of robust and sustainable growth, driven by technological advancements, demographic trends, and expanding surgical capabilities. As healthcare continues to evolve, vascular patches will remain vital components in vascular repair, offering life-saving benefits to millions worldwide. Stakeholders must stay ahead of innovation and regional demands to fully capitalize on the growth opportunities in this dynamic and essential segment of the medical device industry.