The construction electric vehicle market forecast points to a period of significant transformation, with projections indicating robust growth over the next decade. As governments, corporations, and societies globally pursue carbon neutrality goals, the construction industry—a traditionally high-emission sector—is under increasing pressure to adopt clean technologies. Electric construction vehicles are emerging as a practical solution, combining environmental benefits with long-term operational efficiencies.

Looking ahead, the market is expected to witness compound annual growth driven by several converging forces. One of the primary drivers is the growing implementation of government regulations targeting emissions in urban construction zones. Many cities are already mandating zero-emission equipment usage in sensitive areas such as schools, hospitals, and residential neighborhoods. These regulations are anticipated to become stricter and more widespread, creating strong demand for electric alternatives to diesel-powered construction machinery.

Another major factor contributing to the forecasted growth is the surge in public and private investment in green infrastructure. Stimulus packages, climate funds, and sustainability initiatives are encouraging large-scale infrastructure projects that align with low-emission construction practices. Governments across Europe, North America, and Asia-Pacific are allocating billions toward projects that prioritize clean energy, sustainable materials, and electrified construction equipment.

Technological advancements are also a cornerstone of this market outlook. Improvements in battery technology, such as enhanced energy density, fast charging, and thermal stability, are addressing the core limitations of electric construction vehicles. Future electric fleets will likely feature longer operational hours, better durability, and optimized performance under varying environmental conditions. As battery costs continue to decline, the price gap between electric and conventional equipment will narrow, accelerating adoption even further.

The forecast also predicts a rising trend in full-fleet electrification among major construction firms. Large contractors are increasingly setting internal sustainability targets that include reducing equipment-related emissions. To meet these goals, many are planning to replace entire diesel fleets with electric alternatives over the next 5 to 10 years. This trend is expected to gain traction, particularly in regions where climate regulations are more stringent and environmental, social, and governance (ESG) compliance is critical for winning contracts.

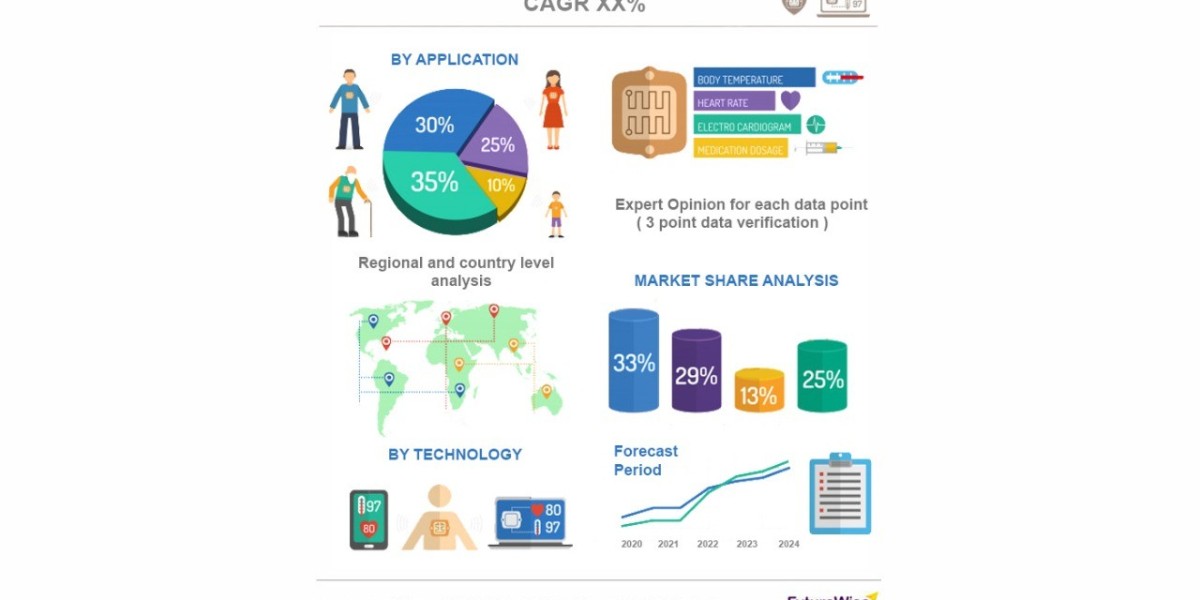

In terms of market segmentation, the forecast anticipates strong adoption across various vehicle types, including electric excavators, loaders, dump trucks, and cranes. Compact electric machines are projected to dominate the short term due to their suitability for indoor and urban construction projects. However, as technology matures, demand for medium- and heavy-duty electric construction vehicles is expected to rise substantially, expanding the market's scope and scale.

Regionally, Europe is likely to remain at the forefront of market growth, driven by proactive legislation and high environmental awareness. Countries like Norway, Germany, and the Netherlands are setting benchmarks for zero-emission construction practices. North America is also forecasted to witness considerable growth, particularly in progressive states like California and New York that are offering incentives for the adoption of electric construction equipment.

Meanwhile, Asia-Pacific is expected to experience rapid expansion due to fast-paced urbanization, infrastructure development, and strong domestic manufacturing capabilities. China, in particular, is investing heavily in electrifying its construction equipment sector, supported by national policies aimed at reducing air pollution and strengthening local production of electric components.

The market forecast also suggests increased collaboration between construction companies and equipment manufacturers. OEMs are investing in research and development to create versatile and high-performance electric machines tailored to diverse construction needs. At the same time, contractors are providing real-world feedback that helps manufacturers fine-tune the performance, charging logistics, and integration of smart technologies into these vehicles.

Challenges, however, are expected to persist during the forecast period. High capital costs, especially for large machinery, could deter small and mid-sized enterprises from transitioning quickly. Additionally, the lack of charging infrastructure at remote or temporary job sites remains a barrier that will need strategic solutions such as mobile charging units or on-site battery swapping systems. Nevertheless, as adoption increases, economies of scale and government support are expected to mitigate these obstacles over time.

In conclusion, the construction electric vehicle market forecast underscores a pivotal decade of transition. With policy support, financial incentives, and ongoing technological innovation, electric construction machinery is set to redefine the future of building and infrastructure development. The coming years will be marked by increased deployment, diverse applications, and a reshaped competitive landscape as stakeholders adapt to the green transformation of construction operations. Those who embrace this shift early will not only meet regulatory expectations but also unlock efficiency gains and sustainability-driven market advantages.