Tactical Communication Systems Market: Overview & Forecast

Market Size & Growth Outlook

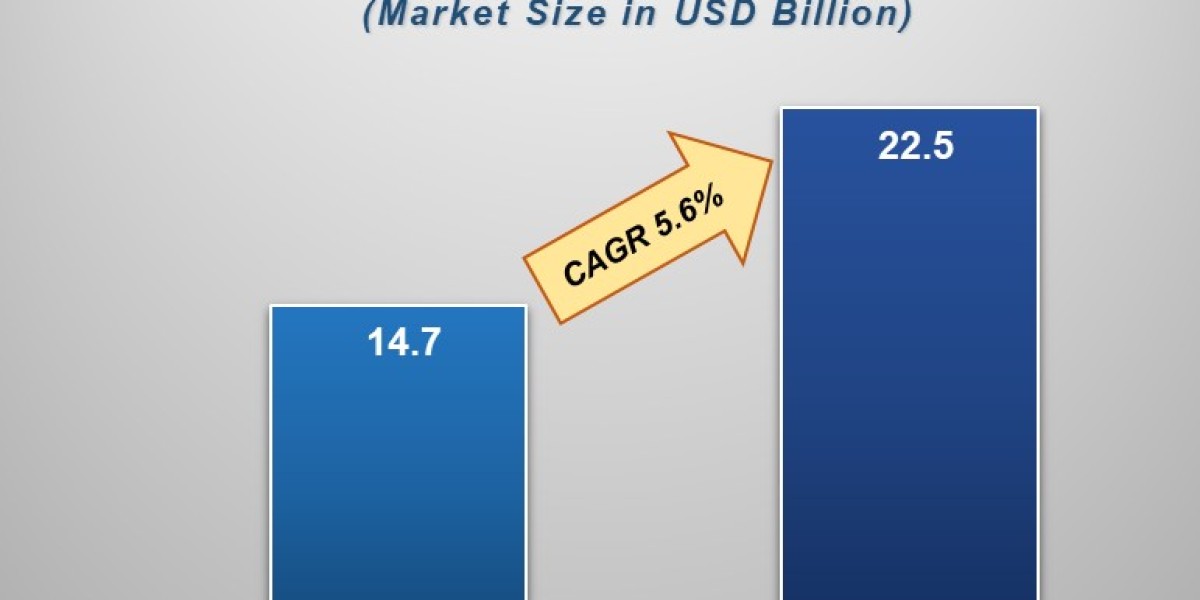

The Tactical Communication Systems (TCS) Market is anticipated to experience substantial growth from 2025 to 2033, fuelled by increasing demand for electric vehicle fuel market growth. With an estimated valuation of approximately USD 14.7 billion in 2025, the market is expected to reach USD 22.5 billion by 2033, registering a robust compound annual growth rate (CAGR) of 5.6% over the decade.

- Get PDF LINK : https://m2squareconsultancy.com/purchase

- Get REPORTS LINKS : https://m2squareconsultancy.com/reports/tactical-communication-systems-tcs-market

Key Drivers Fueling Market Expansion

Rising global defense modernization efforts and transition to network-centric warfare, requiring robust connected communications across platforms and allied forces

Surge in defense budgets, particularly in North America, Asia‑Pacific and Europe; e.g., doubled R&D investment and procurement orders in 2023–25

Growing demand for secure, resilient high-bandwidth links to support real‑time data, ISR (Intelligence, Surveillance, Reconnaissance), and video communications across domains

Integration of AI and ML, enabling cognitive radios, dynamic spectrum access, predictive network routing, and anti‑jamming resistance

Technological Trends & Innovation Drivers

Software‑Defined Radios (SDRs): gaining traction due to flexibility and interoperability; they can be re‑programmed on‑the‑fly for different waveforms and theaters

5G and satellite-backed communications (NTN, SATCOM): leveraging Low Earth Orbit (LEO) constellations and beyond‑line‑of‑sight links to enable high‑bandwidth, low‑latency coverage even in remote theaters

Cybersecurity and anti‑jamming resilience: advanced encryption, zero‑trust frameworks, self‑healing mesh architecture, and secure authentication protocols confirm importance under electronic warfare conditions

AI‑driven network operations: autonomous spectrum and beam steering, electronic counter‑measure detection and avoidance, cognitive modulation and power management for improved efficiency

Miniaturization & soldier‑worn mesh devices: wearable tactical radios, helmet‑integrated comms, and body-conforming units offer increased mobility and endurance

Market Segmentation Breakdown

By Platform:

Land forces lead (~48% share in 2023) and remain dominant buyers

Airborne and naval segments growing steadily, with space/LEO platforms poised for rapid expansion (9% + CAGR)

By Component:

Hardware still dominates (~60% in 2024), but software and services (integration, training, maintenance) are growing faster (~8% CAGR)

By Technology/Frequency:

VHF/UHF platforms had ~32% share in 2024; SATCOM systems expected to grow at ~7.5% CAGR through 2030

HF systems (for BLOS redundancy) remain crucial due to infrastructure‑independence and anti‑jamming resilience

Regional Insights

North America (~35%+ share in 2023): leads overall with highest CAGR projected (~5.9%) driven by U.S. defense tech investments, JADC2 initiatives, and Pentagon mandates

Asia‑Pacific: fastest-growing region (~34% revenue share in 2024), boosted by growing defense budgets and adoption in countries like India, China, Australia, and Southeast Asia

Europe: modernization programs and NATO standardization influence procurement; Germany recently partnered Nokia and Rheinmetall/blackned on 5G‑based tactical networks

Major Players & Competitive Landscape

Leading firms include Thales, L3Harris Technologies, Northrop Grumman, General Dynamics, Elbit Systems, BAE Systems, Leonardo, Rockwell Collins and others

Thales (~18% share) and Harris (~15%) are front-runners in market share

Recent dominant contract awards:

Thales and L3Harris won multi‑billion‑dollar defense contracts

General Dynamics introduced ultra-low latency radios (2024)

Rockwell Collins added blockchain encryption modules to modern systems

Elbit launched satellite‑hybrid extended range platforms

Challenges & Market Restraints

High development and deployment costs of advanced systems (AI‑based SDRs, SATCOM radios) may limit adoption, especially among smaller or budget-constrained defense forces

Interoperability challenges persist due to differing waveforms and legacy systems across services and agencies; standardization remains a key enabler

Opportunities on the Horizon

Networked data‑centric comms enabling integrated ISR, battlefield awareness, and decision-making at the tactical edge

Emerging networking platforms: high‑bandwidth satellite relays, mesh‑networked soldier radios, integrated AI systems, and multi-domain tactical links (e.g., Link 16/22 and beyond)

Public–private partnerships and offset programs (e.g., India’s $1.2 billion offsets in 2023) offer avenues for indigenous production, local manufacturing, and regional adoption

Frequently Asked Questions (FAQ)

1. What are Tactical Communication Systems (TCS)?

Tactical Communication Systems (TCS) are secure, resilient communication networks and devices used by military and defense forces for real-time voice, data, and video exchange in combat and mission-critical environments. They enable situational awareness, command coordination, and mission execution across land, air, sea, and space domains.

2. What technologies are driving the TCS market?

Key technologies include:

Software-Defined Radios (SDRs)

Low Earth Orbit (LEO) satellite communications

5G-enabled battlefield networks

AI-driven network management

Anti-jamming & secure encryption protocols

3. Who are the major players in the TCS market?

Leading companies include:

Thales Group

L3Harris Technologies

General Dynamics

Elbit Systems

Northrop Grumman

BAE Systems

Leonardo

Collins Aerospace (Raytheon Technologies)

4. Which region dominates the tactical communications market?

North America, particularly the United States, dominates the market due to advanced military modernization programs and high defense spending. However, Asia-Pacific is the fastest-growing region, led by countries like India, China, South Korea, and Australia.

5. What are the main challenges in the TCS market?

High development and integration costs

Interoperability issues across allied forces

Vulnerability to cyber and electronic warfare

Slow modernization in some regions due to budget constraints