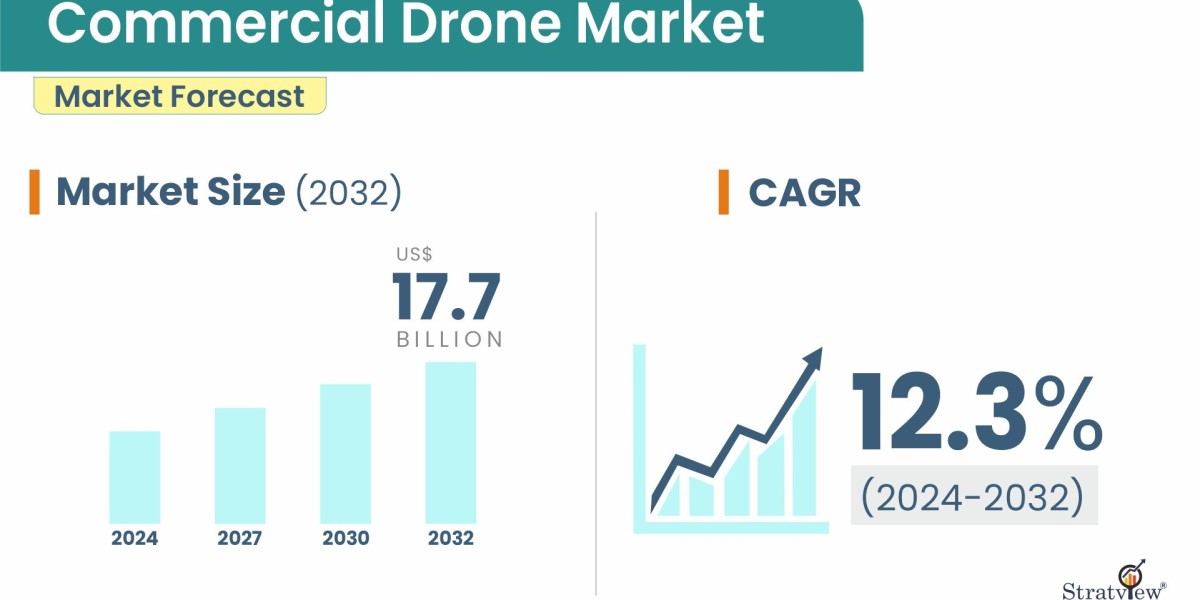

The commercial drone story is increasingly a software story. Yes, airframes and batteries matter—but the real value sits in sensing, autonomy, edge processing, and the analytics that turn pixels and point clouds into decisions. Stratview Research pegs the commercial drone market at USD 5.5 billion in 2023, on track for USD 17.7 billion by 2032 (12.3% CAGR), as drones become standard equipment across asset-heavy sectors.

Request the sample report here:

https://stratviewresearch.com/Request-Sample/2588/Commercial-Drone-Market.html#form

Drivers

Use-case breadth is the first catalyst. Stratview’s segmentation shows a wide front: filming & photography, mapping & surveying, inspection & maintenance, surveillance & monitoring, and precision agriculture. Among these, surveillance & monitoring currently leads—reflecting cross-industry needs for routine site awareness—while precision agriculture is the fastest-growing as farms institutionalize drone-enabled, data-driven agronomy.

End-use momentum is the second. Agriculture remains the largest end user, but delivery & logistics is the fastest-growing as retailers, healthcare systems, and remote communities test and scale last-mile networks. This split signals a market maturing beyond imagery into recurring, operational workflows.

Technology tailwinds are the third—and decisive—driver: AI autonomy reduces pilot workload; LiDAR and multi-sensor fusion widen what can be “seen” and measured; and 5G/edge computing compress time-to-insight for inspections and emergency response. These advances, highlighted by Stratview, tilt value toward integrated platforms that pair flight stacks with analytics, APIs, and enterprise IT hooks.

By platform, rotary-blade craft remain the workhorse for close-in, maneuver-heavy tasks; hybrids are the up-and-comer for long corridors and delivery; fixed-wing holds for area mapping. Expect multirotor to keep share leadership while hybrid climbs fastest.

Regionally, Asia-Pacific dominates and should grow the quickest through 2032—benefiting from manufacturing hubs (notably China) and vast agricultural acreage that accelerates precision-farming adoption.

Competition features a scaled leader and a long tail of specialists. DJI’s scale underpins aggressive pricing and rapid product cycles; challengers like Skydio, Parrot, AeroVironment, Draganfly, AgEagle, JOUAV, Teal, Yuneec, and EHang compete via autonomy stacks, niche payloads, secure supply, or domain focus.

Challenges

Enterprise scale brings enterprise hurdles. Regulatory variance (especially BVLOS and remote ID), pilot training standards, and insurance requirements can slow rollouts and complicate multi-country operations. Power density gains are steady but incremental; many missions still face endurance limits, particularly with heavier sensors. Harsh-weather tolerance (wind, rain, dust, heat/cold) remains a gating factor for year-round use. And as fleets grow, organizations must solve for cybersecurity, data residency, and integration—moving from SD cards and ad-hoc apps to encrypted links, centralized fleet management, and SOC-aligned controls. Supply-chain exposure is another risk: dependence on specific origin countries for key components can trigger procurement or compliance constraints, nudging buyers toward multivendor, “trusted supply” strategies.

Conclusion

The next leg of commercial drone value will be captured by companies that think beyond airframes—toward complete data platforms with autonomy, analytics, compliance, and support built in. Stratview’s outlook—USD 17.7 billion by 2032 at 12.3% CAGR—frames ample headroom, especially in surveillance/monitoring, precision ag, and logistics. Asia-Pacific will set the manufacturing and adoption pace; rotary blades will remain the default; hybrids will sprint. To win, vendors should bundle domain-specific playbooks (e.g., transmission-line inspection, inventory mapping, crop-health scoring), harden security and reliability, and help customers clear regulatory and IT hurdles. That is how drones graduate from cameras on propellers to indispensable, integrated field systems.