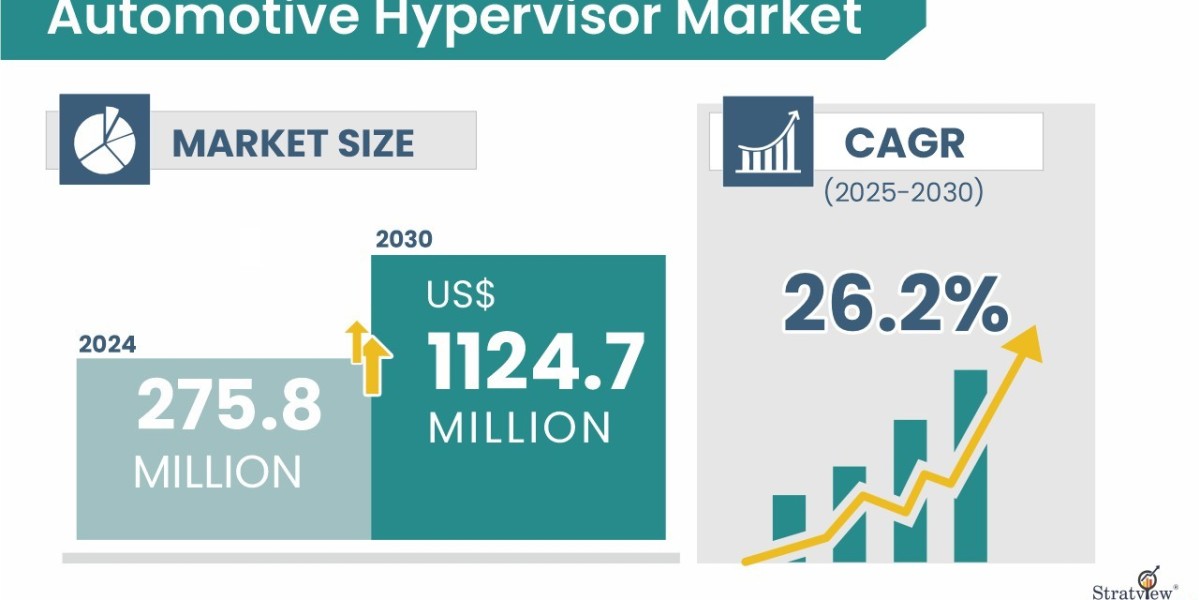

Automotive hypervisors—virtualization layers that let multiple operating systems and safety domains run securely on the same automotive-grade SoC—are becoming foundational to software-defined vehicles. Stratview Research sizes the automotive hypervisors market at USD 275.8 million in 2024 (up from USD 218.5 million in 2023) and projects growth from USD 349.2 million in 2025 to USD 1,780.1 million by 2032, a 26.2% CAGR (2025–2032).

Request a sample report to preview our in-depth analysis:

https://www.stratviewresearch.com/Request-Sample/4075/automotive-hypervisor-market.html#form

Drivers

- ECU consolidation & domain/zonal architectures. As OEMs replace dozens of standalone ECUs with domain and zonal controllers, hypervisors safely partition infotainment, ADAS, and vehicle control workloads on shared compute—cutting weight, wiring, and cost while improving updatability. (Market sizing/period per Stratview.)

- Safety & cybersecurity by design. Hypervisors enforce strong isolation (e.g., separating ASIL-rated functions from non-critical apps), which supports compliance with functional-safety and security requirements as software content in vehicles accelerates. (Scope/need aligned to Stratview’s market framing.)

- Platform breadth across vehicle tiers. Stratview segments demand by end use (economy, mid-priced, luxury), vehicle type (passenger, LCV, HCV), and level of autonomy (semi-autonomous, autonomous)—indicating that virtualization is scaling beyond premium programs.

- Connectivity & OTA lifecycle. Always-connected cars and continuous software updates favor virtualization, which helps OEMs deliver new features without disrupting safety-critical functions. (Drivers consistent with Stratview’s segmentation of sales via OEM and aftermarket channels.)

Trends

- Type 1 vs. Type 2 hypervisors. Stratview analyzes both Type 1 (bare-metal) and Type 2 (hosted) approaches, reflecting different trade-offs in determinism, footprint, and reuse across infotainment, telematics, and ADAS stacks.

- In-vehicle networks evolve. The report tracks hypervisor deployments alongside CAN, LIN, FlexRay, and Automotive Ethernet, underscoring the migration to high-bandwidth backbones that pair well with consolidated compute.

- Broad competitive bench. Stratview’s company coverage spans BlackBerry, Continental, Green Hills Software, Infineon, NXP, Panasonic, Renesas, Sasken, Siemens, and Visteon—illustrating collaboration across OS vendors, Tier-1s, and silicon suppliers.

- Global footprint. Regional analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, down to major country views—highlighting where regulatory frameworks, supply chains, and model mix shape adoption timelines.

Conclusion

Hypervisors are moving from niche to necessity as vehicles become software platforms. With Stratview projecting a climb to USD 1.78 billion by 2032 at 26.2% CAGR, expect rapid adoption across end-use tiers, steady migration to Ethernet-centric E/E, and tight co-development among OS vendors, silicon makers, and Tier-1s. Programs that design isolation, safety, and updateability in from day one will capture the most value as ECU consolidation accelerates.