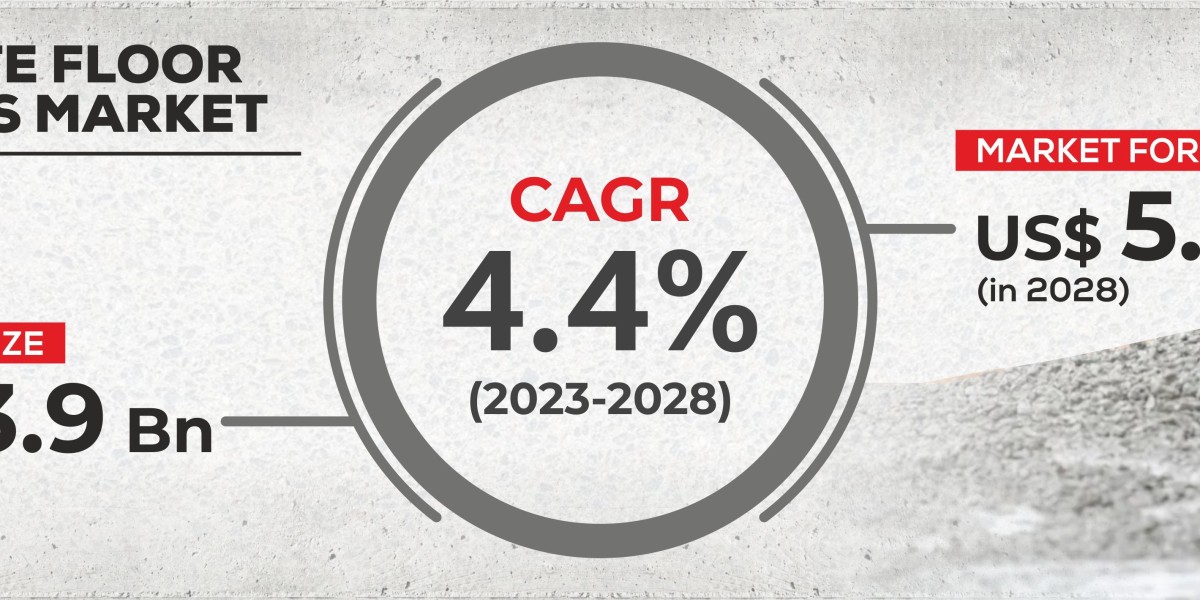

Beyond protection, today’s floor coatings are experience and compliance tools—defining zones, improving light reflectance, and meeting hygiene standards. Stratview projects the concrete floor coatings market to reach US$5.1B by 2028 (4.4% CAGR) from a US$3.9B base in 2022.

Download the Free Sample Report:

https://www.stratviewresearch.com/Request-Sample/1360/concrete-floor-coatings-market.html#form

Drivers

- Operations & lifecycle economics: Owners seek longer service life and lower maintenance, advancing upgrades from bare concrete to coated systems.

- Sectoral adoption: F&B plants, healthcare facilities, and warehouses standardize coatings for hygiene, safety, and throughput.

- Greener specs: Broader preference for eco-friendly, VOC-compliant products.

Trends

- What’s winning: Epoxy leads overall; PU grows in temperature- and abrasion-intensive settings (freezers, hospitals, airports). MMA and others fill speed-of-cure niches.

- Where it’s used: Industrial manufacturing remains the largest application; F&B is the fastest-growing—from wineries to dairy processing.

- Who buys: Industrial end-users dominate; commercial/residential projects extend runway via renovations.

- Geography: Europe holds the lead; Asia-Pacific is the fastest-growing, with China controlling over half of APAC’s market and expanding share.

- Ecosystem: Global brands—including Sika, Sherwin-Williams, BASF, PPG, Jotun, RPM, Covestro, Ardex—compete on portfolio breadth, cure profiles, and local channel strength.

Conclusion

The market’s next leg is defined by hygiene-critical and energy-/time-efficient solutions: fast-curing, low-VOC systems with proven resistance profiles. With Europe setting the deployment pace and APAC accelerating, Stratview’s US$5.1B by 2028 forecast looks durable—especially for suppliers aligning chemistry, compliance, and contractor-friendly application.