Switzerland Fintech Market Overview

Base Year: 2024

Historical Years: 2019-2024

Forecast Years: 2025-2033

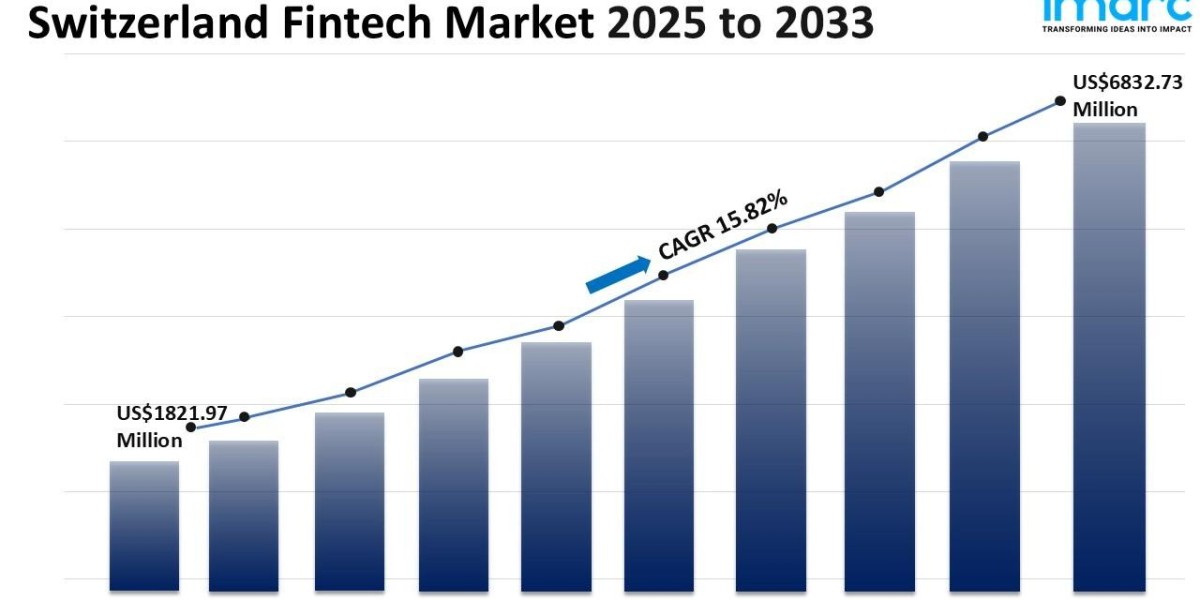

Market Size in 2024: USD 1,821.97 Million

Market Forecast in 2033: USD 6,832.73 Million

Market Growth Rate (2025-33): 15.82%

The Switzerland fintech market size reached USD 1,821.97 Million in 2024. The market is projected to reach USD 6,832.73 Million by 2033, exhibiting a growth rate (CAGR) of 15.82% during 2025-2033. The market is experiencing robust growth, driven by increasing digital adoption, innovation in financial services, and supportive regulatory frameworks. Key trends include the rise of AI, blockchain integration, and mobile banking solutions, reshaping how consumers and institutions interact with finance. Deployment modes, applications, and user preferences continue to diversify, enhancing competitiveness across the sector. As technology evolves and demand for streamlined financial solutions increases, the industry is poised for sustained development. These factors collectively influence the Switzerland fintech market share.

For an in-depth analysis, you can refer sample copy of the report:

https://www.imarcgroup.com/switzerland-fintech-market/requestsample

Switzerland Fintech Market Trends and Drivers:

The Switzerland Fintech Market is undergoing a deep transformation because of how financial services are being smoothly integrated within non-financial platforms with Embedded Finance. The maturation of Banking-as-a-Service largely fuels this trend in which licensed institutions use APIs in order to provide regulatory infrastructure and technological infrastructure to third parties. This impacts the B2B and industrial sectors in Switzerland greatly beyond a consumer-facing phenomenon. For example, top Swiss logistics firms now include trade finance plus insurance products inside their supply chain software since this lets business clients get funding for global deliveries when required. In the same way, accounting software providers are common for Swiss SMEs, and they are incorporating BaaS-powered business banking with lending services in order to create a unified financial management experience. This change forces typical banks to transform into key infrastructure providers that remain unseen however. Here, it grows substantially, along with industry analysts suggesting Swiss entities could grow revenue via Embedded Finance channels at a compound annual rate outpacing customary banking products in the coming years. This dynamic fundamentally redefines the point about sale for financial products. A focus on API robustness, partnership strategies, along with a deep comprehension concerning niche vertical markets is therefore demanded.

Switzerland improves its standing as global digital finance leader since it regulates to encourage safe institutional adoption of digital assets plus Decentralized Finance (DeFi) principles. The Digital Assets Act is as the foundation for this effort of ours providing legal clarity that is unmatched. It does so through classifying tokens into payment, utility, and asset tokens which are three distinct categories. The institutional investors gain all of the certainty that is required for them to allocate meaningful capital. This accurate system comes joined with the present Distributed Ledger Technology (DLT) Law. Digital asset banks and securities dealers in Switzerland with licenses appear now since they provide custodial, trading, also lending services for cryptocurrencies and tokenized normal assets like bonds plus equities. Furthermore, “DeFi 2.0” gains importance as a theory. The underlying protocols of decentralized finance are adapted in order to be used for regulated wholesale finance, which enables an atomic settlement of transactions that are of a large scale, and they also create digital securities that are programmable. This move toward tokenization of real-world assets (RWA) beyond crypto-assets represents the most meaningful growth vector. The projections do indicate that the volume of tokenized assets that are held in Switzerland, which spans from fine art to private equity, will expand at an exponential rate as major financial institutions leverage this very technology in order to improve liquidity and operate with efficiency.

Fintech innovators tactically fuse into Switzerland's wealth management heritage, which defines a trend. This fusion specifically aims at a new set of investors, toward an increasingly wealthy digital-native population. This convergence creates an advanced class of B2B2C as well as direct-to-consumer platforms that blend automated robo-advisory services with access to human financial experts, a model often termed “hybrid advice.” These platforms distinguish themselves through the offering of highly personalized portfolio management that extends beyond customary securities to include sustainable (ESG) investments, thematic portfolios, and also even fractional ownership of alternative assets. Fintechs are partnering with pension funds so as to offer intuitive digital platforms as such growth is pronounced in serving employee needs by way of corporate pension solutions (B2B2E) that provide transparency, educational resources, and greater control over pension assets. People can now actively control their savings for the future solving a key market deficiency. Hyper-personalization will drive future demand because it leverages advanced analytics with AI to deliver proactive financial guidance, tax optimization, also holistic financial planning. Switzerland tailors its skill to modern demands, protecting its continuing leadership within worldwide asset administration.

Switzerland Fintech Market Industry Segmentation:

Deployment Mode Insights:

- On-Premises

- Cloud-Based

Technology Insights:

- Application Programming Interface

- Artificial Intelligence

- Blockchain

- Robotic Process Automation

- Data Analytics

- Others

Application Insights:

- Payment and Fund Transfer

- Loans

- Insurance and Personal Finance

- Wealth Management

- Others

End User Insights:

- Banking

- Insurance

- Securities

- Others

Regional Insights:

- Zurich

- Espace Mittelland

- Lake Geneva Region

- Northwestern Switzerland

- Eastern Switzerland

- Central Switzerland

- Ticino

Competitive Landscape:

The competitive landscape of the industry has also been examined along with the profiles of the key players.

Ask Our Expert & Browse Full Report with TOC & List of Figure:

https://www.imarcgroup.com/request?type=report&id=41652&flag=C

Key highlights of the Report:

- Market Performance (2019-2024)

- Market Outlook (2025-2033)

- COVID-19 Impact on the Market

- Porter’s Five Forces Analysis

- Strategic Recommendations

- Historical, Current and Future Market Trends

- Market Drivers and Success Factors

- SWOT Analysis

- Structure of the Market

- Value Chain Analysis

- Comprehensive Mapping of the Competitive Landscape

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302