The global automotive casting market is valued at USD 6 billion in 2025 and is projected to reach nearly USD 11.6 billion by 2035, expanding at a CAGR of 6.8%. With demand nearly doubling over the next decade, the industry is witnessing rapid transformation fueled by electric vehicle (EV) adoption, stringent emission norms, and advanced casting technologies such as high-pressure die casting and digital simulation.

Full Market Report available for delivery. For purchase or customization, please request here – https://www.futuremarketinsights.com/reports/sample/rep-gb-23471

Market Trends Highlighted

- Lightweight Materials at the Forefront – Aluminum and magnesium castings are steadily replacing steel, supporting automakers’ fuel efficiency and emission goals.

- EV-Driven Growth – Battery housings, motor casings, and lightweight structures are emerging as core demand drivers in electric mobility.

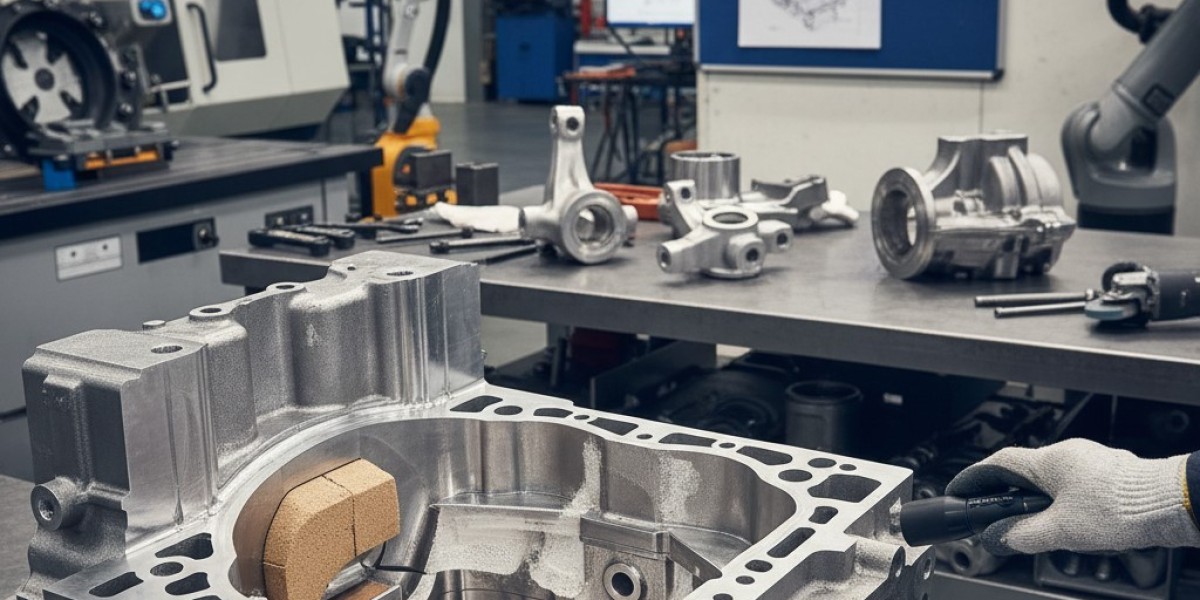

- Digital & Automated Foundries – Robotics, AI-based monitoring, and additive manufacturing are improving efficiency, defect reduction, and design flexibility.

- Aluminum Dominance – Aluminum holds nearly 50% market share, reinforced by recycling initiatives and its suitability for precision parts.

- Die Casting Leadership – Die casting remains the leading process with a 45% share, favored for engine blocks, transmission housings, and structural parts.

Recent Developments

- Leading players such as Nemak, Endurance Technologies, and Ryobi are investing in aluminum and magnesium alloys for lighter and more durable components.

- Strategic alliances between automakers and foundries are accelerating integrated die-casting projects.

- Digital transformation in casting processes is reducing rejection rates and enhancing cycle times.

- In December 2024, Dongfeng Electronic Technology launched its Integrated Die-Casting Industrialization Project in Wuhan, showcasing weight reduction and improved body rigidity for new energy vehicles.

Key Takeaways of the Report

- Market size to nearly double from USD 6B (2025) to USD 11.6B (2035).

- Asia Pacific remains the largest growth hub, followed by North America and Europe.

- Passenger vehicles (65% share) dominate demand, while commercial vehicle casting grows steadily at 6–7% annually.

- Engines account for the largest application share (40%), supported by cylinder heads, blocks, and manifolds.

- Aluminum casting demand in EVs is rising by 11–13% annually.

Market Drivers

- Rising Global Vehicle Production: More than 95 million units produced in 2024, increasing casting demand across powertrain, body, and structural components.

- Lightweight Engineering: Magnesium castings reduce weight by 10–12% beyond aluminum, supporting emission compliance.

- Electric Vehicle Surge: EV components such as battery housings projected to account for 12–14% of total aluminum casting output by 2030.

- Technological Advancements: Robotics integration lowers defect rates below 2%, while 3D printing accelerates mold customization.

Regional Insights

- Asia Pacific leads as the manufacturing powerhouse, with China and India driving demand through strong automotive production and EV adoption.

- North America focuses on lightweight alloys and aftermarket demand for replacement parts.

- Europe emphasizes precision engineering and advanced die-casting technologies, led by Germany’s R&D in alloys.

Country-wise CAGR Analysis (2025–2035)

- China: 6.6% CAGR – Driven by EV adoption and high-volume aluminum/magnesium casting facilities.

- India: 5.8% CAGR – Growth supported by domestic vehicle production and rising export demand.

- United States: 5.4% CAGR – Moderate growth from lightweight casting and strong aftermarket demand.

- Germany: 5.2% CAGR – Focused on alloy research, die-casting precision, and EV structural components.

- United Kingdom: 5% CAGR – Slow but steady modernization with export-driven opportunities.

Competition Outlook

The global market is characterized by established leaders and innovative newcomers, strengthening their positions through R&D, partnerships, and automation.

Key Players:

- Gibbs Die Casting – Expanding lightweight aluminum casting portfolio for engine and transmission components.

- RegensburgerDruckgusswerk Wolf GmbH – Specialist in precision casting for European automakers.

- CFS Foundry – Investing in high-performance materials and advanced processes.

- Endurance Technologies – Expanding Asian operations to serve domestic and international OEMs.

- Zetwerk – Supporting automakers with integrated supply chain and contract manufacturing.

- Zollern GmbH – Focusing on drivetrain and engine casting applications with high-precision solutions.

Key Segments of the Market Report

By Process

- Die Casting (45% share) – Favored for high-volume production, precision, and complex geometries.

By Application

- Engines (40% share) – Cylinder blocks, heads, and manifolds dominate casting requirements.

By Material

- Aluminum (50% share) – Lightweight, recyclable, and critical for EV battery and motor housings.

By Vehicle Type

- Passenger Vehicles (65% share) – Strong demand from ownership growth and aftermarket replacement cycles.

Stay Ahead – Grab the Report: https://www.futuremarketinsights.com/reports/brochure/rep-gb-23471

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: [email protected]

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube