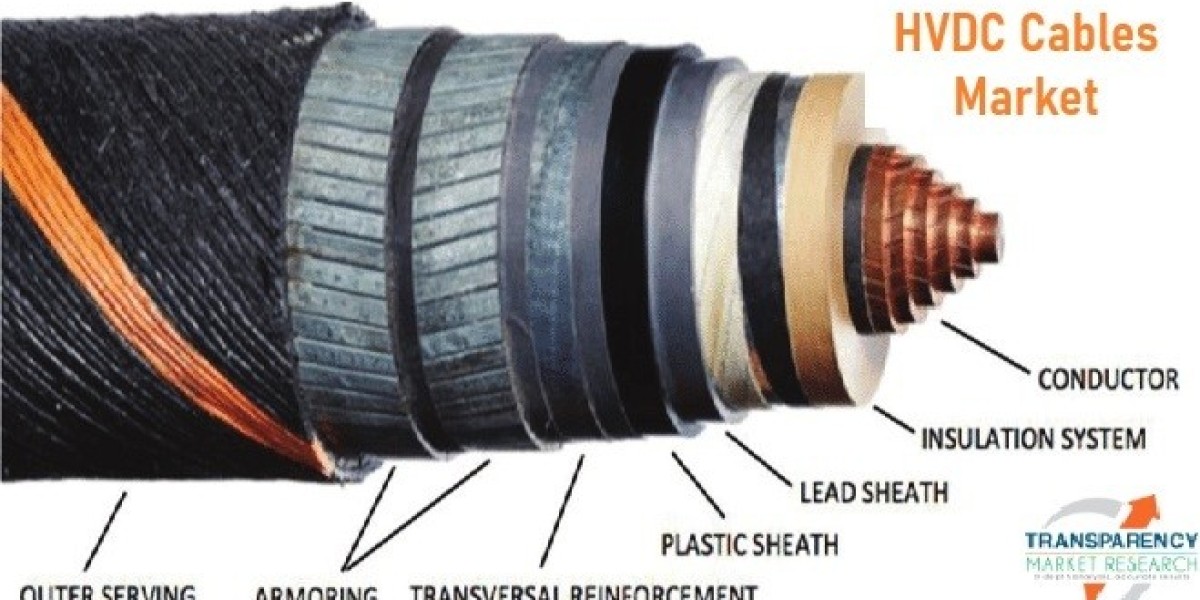

The global high-voltage direct current (HVDC) cables market is a critical enabler of the clean energy transition, facilitating the efficient, long-distance transmission of electricity with minimal losses compared to traditional alternating current (AC) systems. HVDC cables, typically made of copper or aluminum conductors insulated with cross-linked polyethylene (XLPE) or mass-impregnated paper, are pivotal in connecting renewable energy sources like offshore wind farms to grids, supporting intercontinental power exchanges, and enhancing grid stability. Valued at US$ 2.4 billion in 2024, the market reflects robust demand driven by global decarbonization goals, urbanization, and the integration of renewables, with an estimated 12,000 km of HVDC cables installed worldwide. Forecasts project a compound annual growth rate (CAGR) of 6.3% from 2025 to 2035, elevating the market to US$ 4.6 billion by 2035, corresponding to over 25,000 km of new cable deployments. This growth is fueled by investments in green energy infrastructure, advancements in cable insulation technologies, and supportive policies like the EU’s Green Deal. Despite challenges such as high installation costs and complex submarine installations, HVDC cables are poised to underpin the global shift to sustainable energy. This analysis explores the market’s size and growth, segmentation, regional dynamics, drivers and challenges, trends, competitive landscape, future outlook, and key study points to guide stakeholders in this high-stakes sector.

Market Size and Growth

The HVDC cables market’s 2024 valuation of US$ 2.4 billion highlights its role in modern energy systems, with revenues primarily from submarine cables for offshore wind and interconnectors, accounting for 60% of sales (US$ 1.44 billion). Historical growth averaged 5.8% annually from 2019 to 2024, driven by a 30% surge in global offshore wind capacity to 70 GW and cross-border grid projects like the 1,400 MW NordLink. The projected 6.3% CAGR from 2025 to 2035, reaching US$ 4.6 billion, reflects an expected doubling of installed cable length, driven by renewable integration and grid modernization. Sub-segments show submarine cables growing at 7% CAGR, fueled by 50 GW of planned offshore wind by 2030, while underground cables, at 40% share (US$ 0.96 billion), advance at 5.5% for urban grid upgrades. Economic models factoring in energy demand—projected to rise 25% globally by 2035—and stable copper prices (down 8% since 2023) validate this trajectory. Annual R&D investments of US$ 200 million in high-voltage insulation and superconducting cables ensure scalability, positioning HVDC as a backbone for 20% of global renewable energy transmission by 2035.

Market Segmentation

Segmentation reveals a market tailored to diverse transmission needs. By type, submarine cables dominate with 60% share (US$ 1.44 billion in 2024), critical for offshore wind and cross-sea interconnectors like the 720 km Viking Link, offering 30% lower losses than AC. Underground cables, at 40% (US$ 0.96 billion), grow at 5.5% CAGR for land-based grids, minimizing visual impact. By technology, line-commutated converters (LCC) hold 55% (US$ 1.32 billion) for cost-effective bulk power transfer, while voltage-source converters (VSC), at 45%, surge at 7.5% CAGR for flexible renewable integration. By voltage, high-voltage (>400 kV) cables lead with 50% (US$ 1.2 billion), driven by long-distance projects, followed by medium-voltage (100-400 kV) at 30% and ultra-high-voltage (>800 kV) at 20%, growing fastest at 8% for ultra-long interconnectors. By application, renewable energy integration commands 50% (US$ 1.2 billion), with grid interconnectors (30%) and urban power supply (20%) following. This segmentation drives innovations like XLPE-insulated cables, enhancing efficiency by 15%, aligning with global energy transition needs.

Regional Analysis

Asia-Pacific leads with 45% share (US$ 1.08 billion in 2024), driven by China’s 5,000 km of HVDC lines and India’s 20 GW offshore wind target, growing at 7.5% CAGR. Europe, at 30% (US$ 0.72 billion), advances at 6% CAGR, with Germany and the UK deploying 3,000 km for North Sea wind under REPowerEU. North America, holding 15% (US$ 0.36 billion), grows at 5.8% via U.S. grid upgrades backed by US$ 65 billion in IRA funding. Latin America and Middle East/Africa, at 5% each (US$ 0.12 billion), show 7% CAGR, with Brazil and Saudi Arabia scaling interconnectors. Regional tech transfers, like Europe’s VSC expertise to Asia, enhance global deployment and address grid disparities.

Market Drivers and Challenges

Drivers include renewable energy growth, with 30% of global electricity from renewables by 2035, necessitating HVDC for low-loss transmission over 1,000 km. Urbanization, with 60% of populations in cities, and grid modernization investments (US$ 2 trillion globally) boost demand. Policies like EU’s 42% renewable target and advancements in XLPE insulation, cutting costs by 10%, drive adoption. Challenges include high installation costs—US$ 2 million/km for submarine cables—and complex seabed permitting, delaying 20% of projects. Raw material volatility (copper up 12% in 2024) and skilled labor shortages raise costs by 15%. Environmental concerns over seabed disruption and competition from HVAC systems, capturing 5% share, pose risks. Mitigating these via modular designs and green certifications is key.

Market Trends

Trends include superconducting cables, boosting efficiency by 20%, with 10% adoption by 2024. Dynamic line rating systems, optimizing capacity by 15%, grow at 8% CAGR. Sustainable insulation materials, like bio-XLPE, reduce emissions by 25%, aligning with ESG goals in 30% of projects. Hybrid HVDC-AC grids and digital monitoring via IoT, cutting downtime by 30%, reshape the market toward efficiency and sustainability.

Competitive Landscape

Prysmian Group leads with 20% share via its P-Laser cables, followed by Nexans at 15% with submarine expertise. Sumitomo Electric and NKT hold 12% each, focusing on VSC systems. Strategies include M&A (e.g., Prysmian’s US$ 150 million acquisition) and R&D (6% of revenues) for high-voltage insulation. Partnerships with utilities like TenneT drive 25% of projects, ensuring scalability amid 8% margin pressures.

Future Outlook

By 2035, the US$ 4.6 billion market will reflect 25,000 km of cables, with Asia-Pacific at 50% share. Superconducting and hybrid systems will claim 20%, though supply chain risks may trim CAGR to 6% in volatile years. HVDC will support 25% of renewable energy, advancing net-zero goals.