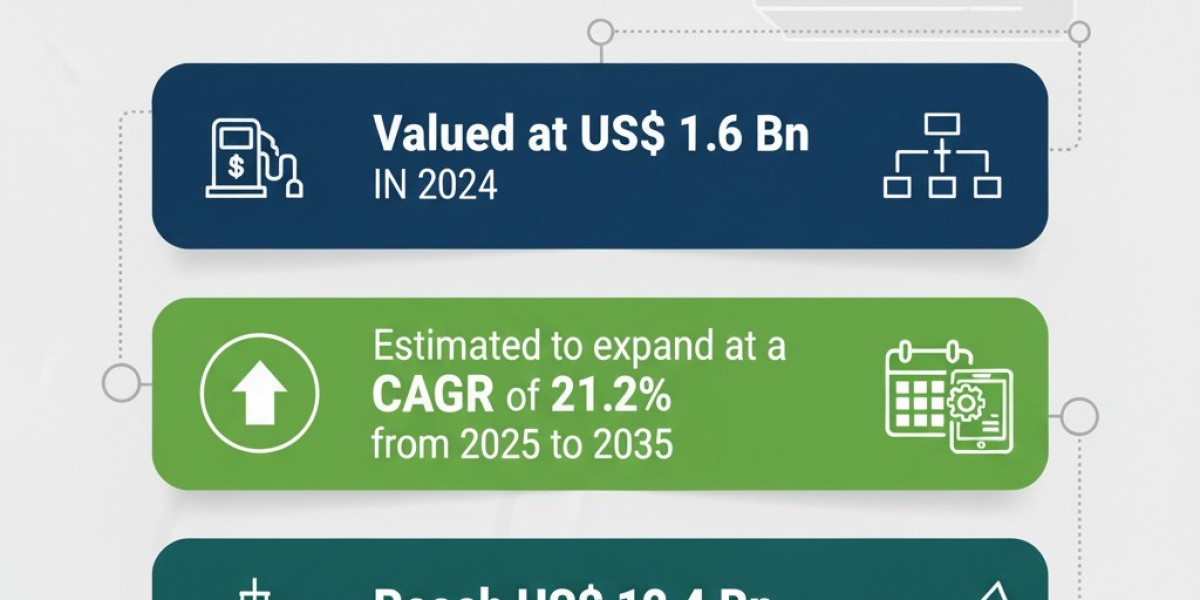

The global LNG bunkering market is entering a phase of dynamic transformation, fueled by the maritime industry's accelerating shift toward cleaner and more sustainable fuel alternatives. Valued at US$ 1.6 billion in 2024, the market is projected to expand at a robust CAGR of 21.2% from 2025 to 2035, reaching an estimated US$ 12.4 billion by 2035. The rapid rise in demand for liquefied natural gas (LNG) as a marine fuel is largely driven by tightening international emission regulations and the industry's long-term decarbonization commitments. As ports, shipping companies, and governments align to meet sustainability targets, LNG bunkering is evolving from a niche service to a mainstream marine fuel infrastructure solution.

Decarbonization and Emission Regulations Drive Growth

One of the most significant factors driving LNG bunkering market expansion is the global push to reduce maritime emissions. The International Maritime Organization (IMO) has implemented strict regulations such as IMO 2020, which limits sulfur content in marine fuels to 0.5%. These rules, combined with long-term goals to cut greenhouse gas emissions by 50% by 2050, have accelerated the adoption of LNG as a transitional fuel. LNG’s ability to reduce sulfur oxide (SOx) emissions by nearly 100%, nitrogen oxides (NOx) by up to 85%, and CO₂ emissions by around 20% makes it an attractive choice for shipping operators. Consequently, LNG is being widely recognized as a viable bridge fuel that can help the industry move toward carbon neutrality.

Infrastructure Expansion: Ports Leading the LNG Transition

The growth of LNG bunkering depends heavily on the availability of bunkering infrastructure, including storage tanks, refueling vessels, and onshore terminals. Over the past few years, major ports in Europe, Asia-Pacific, and North America have invested heavily in LNG bunkering facilities to support this shift. Leading ports such as Rotterdam, Singapore, Yokohama, and Jacksonville have established themselves as LNG bunkering hubs, offering ship-to-ship, truck-to-ship, and terminal-to-ship refueling operations. As global trade routes evolve and more vessels adopt LNG propulsion systems, new infrastructure projects are emerging in regions such as India, the Middle East, and Southeast Asia, ensuring broader geographical coverage and accessibility.

Rising Adoption Across Vessel Segments

The uptake of LNG-fueled ships across diverse vessel categories—such as container ships, tankers, ferries, and bulk carriers—has created a strong foundation for market growth. Shipowners are increasingly investing in LNG-powered vessels due to regulatory pressures, operational savings, and brand sustainability commitments. In 2024 alone, the number of LNG-capable vessels surpassed 1,000 globally, with many new builds already being delivered with dual-fuel engine systems. LNG’s competitive pricing compared to traditional marine fuels also provides a long-term cost advantage. The rising number of LNG-ready vessels directly correlates with the increased demand for bunkering services, reinforcing a cycle of growth between infrastructure and vessel adoption.

Technological Advancements in Bunkering Operations

Advancements in LNG bunkering technology are enhancing safety, efficiency, and reliability across operations. Modern LNG bunkering systems now incorporate automated fueling processes, advanced leak detection systems, and cryogenic transfer technologies that minimize risk and operational downtime. The adoption of digital monitoring tools and remote-control bunkering systems further enhances precision and safety compliance. Additionally, the integration of hybrid bunkering solutions—where LNG is combined with bio-LNG or synthetic methane—is gaining momentum as companies look to further reduce lifecycle emissions. These innovations not only optimize performance but also prepare the market for the next phase of clean fuel evolution.

Europe and Asia-Pacific: Leading the Global LNG Bunkering Landscape

Europe currently dominates the global LNG bunkering market, supported by strong policy frameworks, port collaborations, and environmental awareness. The region’s extensive LNG infrastructure, particularly in countries such as Norway, the Netherlands, Spain, and France, continues to attract international vessel operators. Meanwhile, Asia-Pacific is emerging as a key growth engine, with countries like Singapore, Japan, China, and South Korea rapidly scaling up LNG bunkering capabilities. Singapore, in particular, has positioned itself as a global leader in LNG bunkering services, handling a significant share of global bunkering operations. In North America, regulatory support and investments in LNG liquefaction and terminal capacity are driving market expansion along major coastlines and inland waterways.

Economic and Environmental Advantages of LNG Bunkering

The economic viability of LNG bunkering lies in its ability to offer cost-efficient and cleaner marine fuel alternatives compared to conventional heavy fuel oils. While the initial investment in LNG infrastructure and vessel retrofitting can be high, the operational savings and long-term compliance benefits far outweigh these costs. LNG’s lower maintenance requirements and extended engine life contribute to reduced operating expenses. From an environmental standpoint, LNG’s role in reducing global maritime pollution and meeting Environmental, Social, and Governance (ESG) objectives positions it as a critical enabler of sustainable shipping.

Challenges and Emerging Opportunities

Despite strong growth prospects, the LNG bunkering market faces challenges such as high infrastructure costs, limited storage capacity, and fluctuating LNG prices. However, industry collaborations and technological innovations are helping mitigate these issues. The growing interest in bio-LNG and e-LNG—renewable forms of liquefied natural gas—presents a major opportunity for the future. These sustainable alternatives can be integrated seamlessly into existing LNG supply chains, enabling a gradual transition toward zero-carbon fuels. Moreover, as carbon pricing and emission trading systems expand globally, LNG is expected to gain further economic competitiveness.

Competitive Landscape and Key Players

The LNG bunkering market features a competitive mix of energy companies, terminal operators, and logistics providers. Leading players include Royal Dutch Shell plc, TotalEnergies SE, Gasum Oy, ENGIE SA, Korea Gas Corporation, and Bomin Linde LNG GmbH & Co. KG. These companies are actively expanding their bunkering fleets, forming strategic alliances with port authorities, and investing in renewable LNG solutions. The increasing collaboration between shipowners and fuel suppliers is also fostering a robust supply ecosystem to meet growing demand across global shipping lanes.

Future Outlook: LNG as a Bridge to Carbon-Neutral Shipping

Looking ahead, the LNG bunkering market is expected to remain one of the fastest-growing segments in marine energy. The ongoing transition toward alternative fuels such as ammonia, hydrogen, and bio-LNG will further enhance LNG’s relevance as a bridge technology. With major maritime players committing to net-zero emissions and global ports adopting clean energy policies, LNG bunkering will continue to play a central role in the industry’s sustainability roadmap.

By 2035, the market’s projected value of US$ 12.4 billion underscores its critical role in redefining the future of marine fueling. As global shipping accelerates its green transition, LNG bunkering will stand as a cornerstone of the cleaner, smarter, and more sustainable maritime industry of tomorrow.