MARKET OVERVIEW

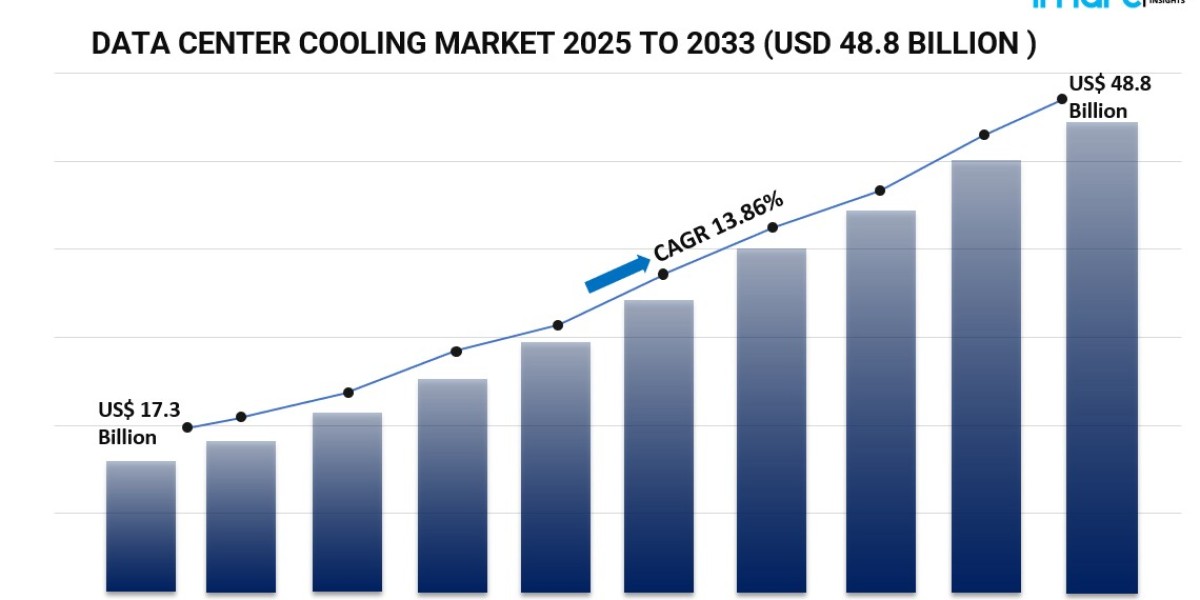

The global Data Center Cooling Market was valued at USD 17.3 Billion in 2024 and is projected to reach USD 48.8 Billion by 2033. The market is expected to grow at a CAGR of 13.86% during the forecast period 2025-2033. This growth is driven by rising demand for energy-efficient data centers, the proliferation of cloud computing, and the need to maintain optimum temperature and humidity for high-performance computing infrastructure.

STUDY ASSUMPTION YEARS

- Base Year: 2024

- Historical Years: 2019-2024

- Forecast Year/Period: 2025-2033

DATA CENTER COOLING MARKET KEY TAKEAWAYS

- Current Market Size: USD 17.3 Billion in 2024

- CAGR: 13.86%

- Forecast Period: 2025-2033

- Increasing demand for cooling solutions helps data centers reduce carbon footprint and operational costs.

- Growing cloud computing and edge computing adoption enhance the market outlook.

- Asia Pacific dominates the market due to digital infrastructure expansion.

- Challenges include high energy consumption and upfront costs.

- Opportunities lie in advanced, energy-efficient cooling technologies such as free cooling and advanced liquid cooling.

Request for sample copy of this report: https://www.imarcgroup.com/data-center-cooling-market/requestsample

MARKET GROWTH FACTORS

The data center cooling market is driven by the growing need to reduce the carbon footprint and operate cost of data centers and make them sustainable. The performance of the server, networking equipment, and other data center infrastructure components heavily depends on the temperature and humidity of the data center. As server density increases and workload requirements increase it has become increasingly important to cool them.

Cloud computing has prompted the construction of many data centers, which together hold 60% of the world's corporate data and consume 3% of the world's energy. With 90% of large companies using multi-cloud, data centers with advanced cooling systems which manage to extract heat from a greater density of servers are expected to continue showing strong growth in the market.

Another driving factor for the growth of the market is the exponential increase in the number of Internet of Things (IoT) devices, which will almost double in the next few years, from ~15 billion in 2023 to over 32 billion by 2030 and over 8 billion IoT devices in China by 2033. Such a huge amount of data generation requires improved data processing and storage capacity along with improved heat dissipation, which drives the demand in the market.

MARKET SEGMENTATION

By Solution:

- Air Conditioning: Dominates the market; essential for maintaining equipment operating conditions by removing generated heat.

- Chilling Units

- Cooling Towers

- Economizer Systems

- Liquid Cooling Systems

- Control Systems

- Others

By Services:

- Consulting

- Installation and Deployment: Holds the largest share; critical for setting up systems to ensure efficient operation.

- Maintenance and Support

By Type of Cooling:

- Room-Based Cooling: Largest segment; focuses on cooling specific spaces to enhance energy efficiency.

- Row-Based Cooling

- Rack-Based Cooling

By Cooling Technology:

- Liquid-Based Cooling: Largest share; uses coolant fluid circulating through components to efficiently dissipate heat.

- Air-Based Cooling

By Type of Data Center:

- Mid-Sized Data Centers

- Enterprise Data Centers: Largest share; centralized facilities managing IT resources for organizations.

- Large Data Centers

By Vertical:

- BFSI

- IT and Telecom: Largest sector; requires stable cooling due to high-performance computing equipment.

- Research and Educational Institutes

- Government and Defense

- Retail

- Energy

- Healthcare

- Others

By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

REGIONAL INSIGHTS

Asia Pacific dominates the global Data Center Cooling Market, holding the largest market share. This dominance is attributed to rapid digital infrastructure development, increasing adoption of cloud computing, and proliferation of IoT devices. For instance, in April 2024, GDS partnered with Gaw Capital Partners to build a 40-megawatt data center campus in Tokyo, Japan, exemplifying significant regional investment and growth.

RECENT DEVELOPMENTS & NEWS

- September 2024: Gates launched the Data Master Data Center Cooling Hose, enhancing cooling system components.

- August 2024: Airedale introduced its Cooling System Optimizer in the U.S., an intelligent control layer integrating chiller and CRAH controls with building management systems.

- June 2024: Petronas Lubricants International collaborated with Iceotope to launch a novel data center cooling fluid, advancing cooling technology options.

KEY PLAYERS

- Airedale International Air Conditioning

- Asetek

- Black Box Corporation

- Climaveneta Climate Technologies

- Coolcentric

- Emerson Electric

- Fujitsu

- Hitachi

- Netmagic

- Nortek Air Solutions, LLC

- Rittal

- Schneider Electric

- STULZ GmbH

- Vertiv

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

https://www.imarcgroup.com/request?type=report&id=1974&flag=E

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: [email protected],

Tel No: (D) +91 120 433 0800,

United States: +1-201-971-6302