Executive Summary

The Consumer Appliances Market is a substantial and resilient industry, projected for steady growth driven by technological upgrades and emerging economies.

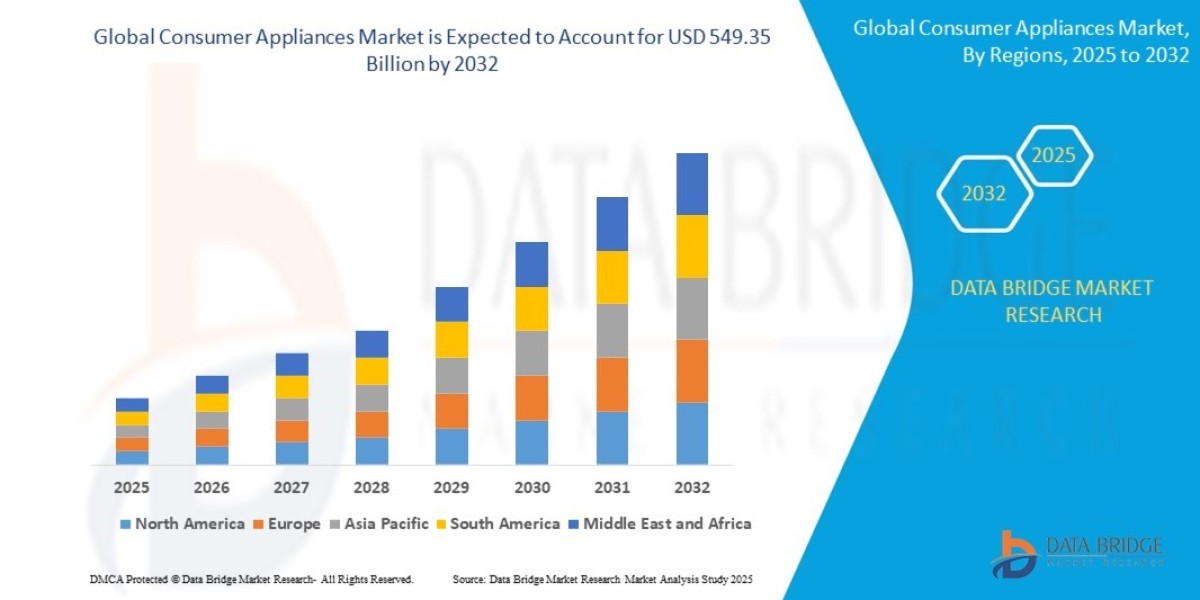

- The global consumer appliances market size was valued at USD 398.33 billion in 2024 and is expected to reach USD 549.35 billion by 2032, at a CAGR of 4.10% during the forecast period

Market Overview

Defining the Consumer Appliances Market

The Consumer Appliances Market primarily includes devices designed for household use, segmented into two main categories:

Major Appliances (White Goods): Large, essential household items like refrigerators, washing machines, dishwashers, cooking ranges/ovens, and air conditioners/HVAC systems. These typically have long replacement cycles.

Small Appliances (Brown/Other Goods): Compact, portable devices such as vacuum cleaners, coffee makers, blenders, air fryers, food processors, and hair styling tools. These are characterized by shorter replacement cycles and higher impulsivity in purchasing.

Key Segments and Dynamics:

| Segmentation Factor | Dominant Segment (2024) | Key Growth Catalyst |

| Product Type | Major Appliances ($\approx 89.5\%$ Share) | Small Appliances ($\text{CAGR} \approx 6.4\%$) |

| Technology | Conventional Appliances | Smart Appliances ($\text{CAGR} \approx 18.7\% \text{ to } 19.2\%$) |

| End-Use | Residential ($\approx 70\%$ Share) | Commercial ($\text{CAGR} \approx 5.8\%$) |

| Distribution Channel | Electronic Stores (Largest Revenue Share) | Online/E-commerce (Fastest Growth, $\text{CAGR} \approx 7.6\%+$) |

Drivers and Current Dynamics

Urbanization and Nuclearization of Families: The rapid growth of urban populations, particularly in $\text{APAC}$, and the trend toward smaller, nuclear families drives demand for compact, multifunctional, and space-saving appliances (a key driver for small appliances).

Rising Disposable Incomes in Emerging Markets: Expanding middle-class populations in China, India, and Southeast Asia are transitioning from first-time appliance buyers to repeat/upgrade buyers, fostering demand for premium, smart, and feature-rich models.

Smart Home Ecosystem Penetration ($\text{IoT}$): The integration of $\text{IoT}$, $\text{Wi-Fi}$, and $\text{AI}$ into appliances is moving from novelty to expectation. Consumers seek interoperability with platforms like Amazon Alexa, Google Home, and Samsung SmartThings.

Governmental Energy Efficiency Mandates: Strict regulatory frameworks (e.g., $\text{EU}$ Ecodesign, energy labeling programs in the $\text{US}$, India, and China) compel consumers to adopt high-efficiency appliances (e.g., inverter ACs, A+++ rated machines) during replacement cycles, boosting value sales.

Health and Wellness Focus: Increased consumer focus on air quality, food safety, and healthy cooking drives demand for products like smart air purifiers ($\text{CAGR} \approx 19.2\%$), high-performance blenders, and air fryers.

Market Size & Forecast

The market shows stable foundational growth with high-velocity segments driving premium value.

- The global consumer appliances market size was valued at USD 398.33 billion in 2024 and is expected to reach USD 549.35 billion by 2032, at a CAGR of 4.10% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-consumer-appliances-market

Key Trends & Innovations

Innovation is focused on digitizing user experience, enhancing sustainability, and delivering tangible functional benefits.

1. The $\text{AIoT}$ and Interoperability Mandate

True $\text{AI}$-Driven Personalization: $\text{AI}$ moves beyond simple voice control. Smart refrigerators use internal cameras and $\text{AI}$ to track inventory, suggest recipes based on available ingredients, and auto-order groceries. Washing machines learn fabric types and water hardness to optimize cycles without user input.

Cross-Ecosystem Interoperability (Matter/Thread): The industry is consolidating around open standards like Matter, aiming to solve the fragmentation barrier where appliances from different brands couldn't seamlessly communicate. This shift is critical for accelerating mass consumer adoption of smart homes.

Predictive Maintenance and Diagnostics: Connected appliances self-monitor their components, predict potential failures before they occur, and automatically schedule technician visits, shifting the service model from reactive to proactive.

2. Deep Sustainability and Circular Economy

Repairability and Durability: Driven by regulatory pressure (e.g., $\text{EU}$'s Right to Repair) and Millennial/Gen $\text{Z}$ consumer demand, manufacturers are designing appliances with modular components and committing to parts availability for longer periods, emphasizing longevity over frequent replacement.

Focus on $\text{Embodied}$ $\text{Carbon}$: Beyond energy use, brands are marketing the use of recycled materials in casing and components, and tracking the $\text{ESG}$ profile of their supply chains.

Home Energy Management Systems ($\text{HEMS}$): Appliances are becoming key components of $\text{HEMS}$, optimizing energy consumption by running high-draw tasks (like laundry or dishwashing) during off-peak electricity hours, driven by utility incentives and high energy costs.

3. Hyper-Specialization in Small Appliances

Wellness and Hygiene Appliances: The post-pandemic focus on in-home health fuels demand for sophisticated air purifiers (with $\text{HEPA}$/carbon filters), smart water purification systems, and robotic vacuum cleaners with advanced mapping capabilities.

Multifunctionality and Compactness: For smaller living spaces, appliances combining multiple functions (e.g., combination microwave/air-fryer/steam ovens) or offering versatile use (e.g., modular kitchen systems) command a premium.

Competitive Landscape

The market is characterized by moderate concentration, dominated by a few global powerhouses, yet highly fragmented by regional and niche players.

Major Players and Strategic Focus

| Company | Core Strength | Strategic Competitive Move |

| Haier Group (Haier, GE Appliances, Fisher & Paykel) | Largest volume, diversification across regions | Global $\text{M\&A}$ strategy; focus on establishing leadership in the $\text{Smart Home}$ $\text{Ecosystem}$ via its $\text{U}-Home$ platform. |

| Samsung Electronics Co. Ltd. | Technology, $\text{AI}$ integration, Brand Equity | Aggressive integration of $\text{AI}$ into its $\text{Family Hub}$ refrigerators and $\text{SmartThings}$ ecosystem; leading the push for interoperability. |

| LG Electronics Inc. | Premiumization, Design, $\text{HVAC}$ Strength | Focus on $\text{ThinQ}$ platform and $\text{GenAI}$ features; strategically acquiring smart home firms (e.g., Athom) to enhance ecosystem integration. |

| Whirlpool Corporation | North American market depth, $\text{Major}$ $\text{Appliances}$ | Focus on portfolio simplification (divesting European business); strategic partnerships (e.g., Beko Europe B.V.) to consolidate manufacturing and R&D. |

| Midea Group | Cost leadership, $\text{Small}$ $\text{Appliances}$ $\text{Volume}$ | Dominance in $\text{APAC}$ and strong $\text{OEM}$/export position; rapidly scaling up connected appliance portfolio. |

Competitive Strategies

Ecosystem Lock-in: The central competition is not just appliance-to-appliance, but ecosystem-to-ecosystem. Brands like Samsung (SmartThings) and LG (ThinQ) strive to be the dominant platform that connects all other devices in the home, creating strong brand loyalty.

$\text{DTC}$ and Omnichannel Shift: Manufacturers are moving beyond traditional retailer models by developing robust $\text{DTC}$ (Direct-to-Consumer) online stores, enhancing virtual showrooms ($\text{AR}$ visualization), and offering integrated post-sale service packages, including installation and maintenance.

Price vs. Value Segmentation: The market is bifurcated: a strong price war in the mass-market/conventional segment (especially in $\text{APAC}$) and intense competition on premium value in developed markets, where innovation, design, and sustainability justify higher prices.

$\text{M\&A}$ for Capability Gaps: Large players consistently acquire smaller, innovative startups focused on niche technology (e.g., $\text{AI}$ software, specialized sensor technology) or regional distribution to rapidly bridge technology or market gaps.

Regional Insights

??/?? Asia-Pacific (APAC) - The Engine of Volume and First-Time Purchases

Market Dynamics: $\text{APAC}$ is the largest and fastest-growing region ($\text{CAGR} \approx 6.30\% \text{ to } 6.5\%$). Driven by the highest number of first-time buyers, construction booms, and rapid income growth. China is the largest country market, while India shows the highest future CAGR ($\approx 5.29\%$) due to low appliance penetration rates and government incentives (e.g., $\text{PLI}$ schemes for local manufacturing).

Opportunity: Massive demand for affordable, yet energy-efficient $\text{HVAC}$ and refrigeration units. Online sales (rising at $\approx 6.54\%$ $\text{CAGR}$) are critical for reaching tier-2/3 city consumers.

?? North America - Premium and Smart Penetration

Market Dynamics: Mature, replacement-driven market with high $\text{smart home}$ penetration. Demand is focused on premiumization, large capacity units, and advanced energy efficiency. Housing renovations and consumer preference for connected living drive growth.

Opportunity: High acceptance of flexible financing and Home-as-a-Service models, including appliance rental and subscription services for features/software.

?? Europe - Sustainability and Regulatory Compliance Leader

Market Dynamics: Highly regulated market, prioritizing environmental compliance ($\text{Ecodesign}$, energy labeling) and durability. Growth is concentrated in the built-in appliance segment and high-rated energy-efficient models.

Opportunity: Strong demand for solutions that reduce food waste (smart refrigeration) and minimize water/energy usage in washing and dishwashing cycles.

Challenges & Risks

Supply Chain Volatility and Raw Material Costs: The market is highly susceptible to price spikes in key raw materials (steel, aluminum, copper, and specialized components like semiconductors/compressors). Geopolitical events and trade tariffs exacerbate these cost pressures, forcing price increases on consumers.

Interoperability and Security Barriers for Smart Appliances: Despite the hype, consumer adoption of smart appliances is hampered by complex setup, lack of true interoperability between different brands, and rising concerns over data privacy and cyber-security of connected home devices.

Intense Price Competition: Especially in high-volume, mass-market segments (like refrigerators in $\text{APAC}$), intense competition from regional and low-cost manufacturers squeezes margins for major global players, making sustained $\text{R\&D}$ investment challenging.

E-Waste Management and Regulatory Compliance: The increasing volume of electronic waste (e-waste) and stricter take-back and disposal regulations pose significant operational and financial challenges for manufacturers, particularly in the $\text{EU}$.

Opportunities & Strategic Recommendations

1. Opportunities

Home-as-a-Service ($\text{HaaS}$) Models: Transitioning the revenue model from a one-time product sale to a recurring service model (e.g., appliance rental, subscription access to $\text{AI}$-driven software features, or predictive maintenance contracts).

Food Waste Reduction $\text{Tech}$: Developing smart refrigeration and food storage solutions that actively monitor food spoilage and manage inventory to tap into the massive consumer demand for reducing household food waste.

$\text{DTC}$ for Small Appliances: Leveraging the high $\text{CAGR}$ of online sales for small appliances by focusing on a $\text{DTC}$ model with personalized marketing, flexible payment options, and exclusive online-only models.

2. Strategic Recommendations

| Stakeholder Group | Strategic Recommendation | Rationale |

| Established Manufacturers | Decisively Invest in Cross-Brand Interoperability. | Proactively support open standards (Matter) and simplify setup. Interoperability is the key to unlocking mass adoption of the high-value smart segment and securing ecosystem loyalty. |

| Startups/New Entrants | Focus on a Niche 'Wellness' Appliance. | Avoid competing with giants in the major appliance space. Instead, specialize in high-margin, functional niches like advanced water filtration, smart air quality control, or specialized cooking tools to gain market traction via digital channels. |

| Retailers (Electronic Stores) | Transform the Store into an 'Ecosystem Experience Center'. | Focus on demonstrating the interconnectedness of smart appliances from different brands, allowing consumers to test $\text{IoT}$ integration, which addresses the "high investment/high uncertainty" barrier to smart appliance purchase. |

| Investors | Target Component Suppliers with Green $\text{Tech}$. | Invest in suppliers providing essential components like $\text{digital}$ $\text{inverter}$ $\text{compressors}$, $\text{recycled}$ $\text{plastics}$, or high-efficiency heat pumps, as these technologies are mandated by global regulations and are crucial for all manufacturers. |

Browse More Reports :

North America Data Integration Market

Middle East and Africa Small Molecule Sterile Injectable Drugs Market

Global Rail Fasteners Market

Global Monoterpenes Market

Global Point of Care Infectious Disease Market

Global Canned Berries Market

Global Immunomodulators Market

Global Cancer Gene Therapy Market

Global Solar Thermal Collector Market

Global Freeze-Dried Fruits Market

Global Network Security Software Market

Asia-Pacific Mass Notification Systems Market

Europe Dental Practice Management Software Market

Global Fractional Flow Reserve Market

Global Angiographic Catheter Market

Europe Heavy Metals Testing Market

North America Hand Holes Market

North America Indium Market

Global Skin Packaging Market

Global 3D Cell Culture Market

Global Micro Battery Market

Global Chitosan Market

Global Form-Fill-Seal (FFS) Films Market

Europe Surgical Power Tools Market

Middle East and Africa Flight Data Recorder Market

Global Transthyretin Amyloidosis Treatment Market

Global Flexographic Inks Market

Asia-Pacific Composite Bearings Market

Europe Feed Flavors and Sweeteners Market

Global Interventional Oncology Devices Market

Middle East and Africa Methylene Diphenyl Diisocyanate (MDI) Toluene Diisocyanate (TDI) and Polyurethane Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- [email protected]