Executive Summary

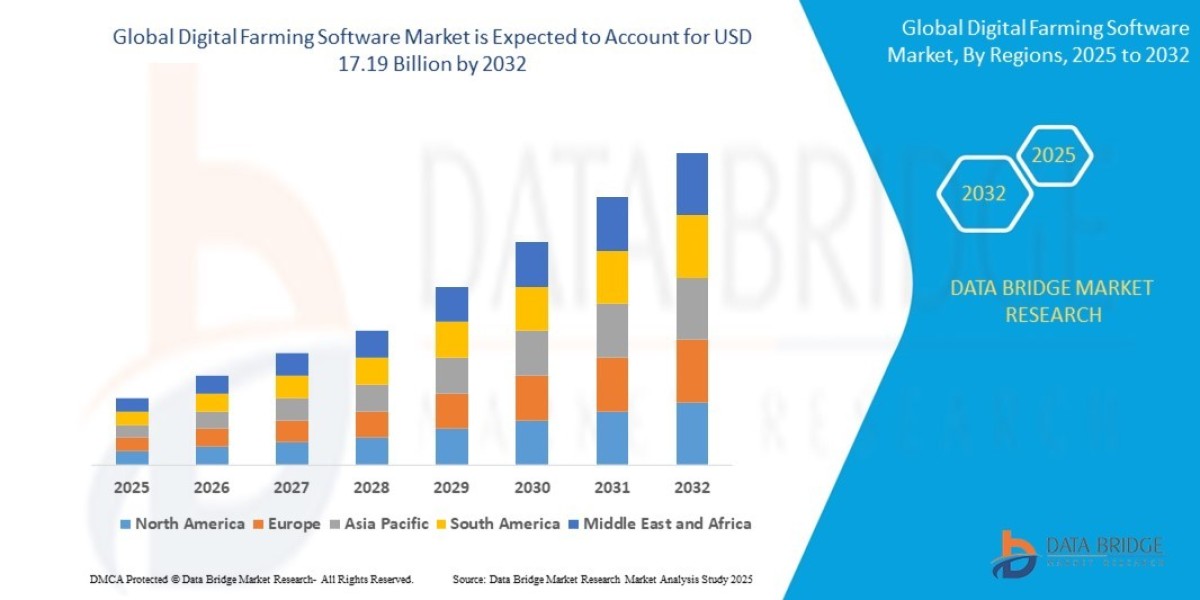

- The global digital farming software market size was valued at USD 6.42 billion in 2024 and is expected to reach USD 17.19 billion by 2032, at a CAGR of 13.1% during the forecast period

Market Overview

The Digital Farming Software Market comprises a range of solutions—often delivered via Software-as-a-Service (SaaS)—that integrate data from various sources (satellites, drones, sensors, weather stations) to provide farmers and agribusinesses with actionable insights. This market is shifting agriculture from traditional, generalized methods to predictive, prescriptive farming.

Defining the Market and Key Segments

Digital farming software can be broadly categorized into several functional segments:

Farm Management Systems (FMS): Core platforms for managing records, inventory, accounting, labor, and compliance. This forms the operational backbone of digital agriculture.

Precision Agriculture Software: Solutions focused on spatial data analysis, including Variable Rate Technology (VRT) applications for precise input dispersal (seed, fertilizer, chemicals).

Livestock Management Software: Tools for monitoring animal health, feeding schedules, herd tracking, and performance analysis.

Supply Chain Management/Traceability Software: Platforms that track produce from "farm to fork," ensuring provenance, quality control, and meeting consumer demand for transparency.

Market Drivers

Global Food Security and Population Growth: The necessity of increasing yield per acre while minimizing environmental impact is the foundational driver. Software provides the means to maximize efficiency.

Climate Change and Resource Scarcity: Increasing weather volatility and the scarcity of water and arable land necessitate precision tools to optimize irrigation and manage disease outbreaks preemptively.

Technological Integration: The sharp decline in the cost of sensors, IoT devices, and drone technology makes the necessary hardware infrastructure affordable, feeding vast amounts of real-time data into the software platforms.

Regulatory Compliance: Governments globally are mandating stricter environmental and sustainability reporting (e.g., carbon sequestration, nitrogen runoff limits), which requires sophisticated software for accurate data capture and audit trails.

Current Dynamics

The market is currently characterized by consolidation and a focus on interoperability. Large agricultural machinery manufacturers (OEMs) are acquiring tech startups to integrate software deeply with their hardware (tractors, sprayers), creating proprietary ecosystems. Simultaneously, independent software vendors (ISVs) are focusing on open APIs to integrate seamlessly with multiple hardware brands, challenging the OEM-centric approach. A major dynamic is the shift from descriptive analytics ("What happened?") to prescriptive analytics ("What should I do now?"), driven by machine learning.

Market Size & Forecast

- The global digital farming software market size was valued at USD 6.42 billion in 2024 and is expected to reach USD 17.19 billion by 2032, at a CAGR of 13.1% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-digital-farming-software-market

Key Trends & Innovations

The innovation landscape in digital farming is rapidly evolving, merging traditional agronomic expertise with cutting-edge digital technologies.

1. Artificial Intelligence and Predictive Modeling

AI is moving beyond simple image processing for weed detection. Advanced machine learning models are now analyzing vast historical data (soil composition, hyper-local weather patterns, historical yield data) to provide highly accurate prescriptive advice on planting densities, optimal fertilizer blends, and even predicting commodity price fluctuations tied to local yield estimates.

2. Hyper-Local Data Collection via IoT and Edge Computing

The proliferation of low-cost IoT devices (soil moisture probes, weather stations, animal-worn sensors) creates massive, high-frequency datasets. Edge computing is a crucial trend, processing this sensor data directly on farm equipment (e.g., tractors, harvesters) to make real-time decisions (like adjusting seed depth) without latency caused by cloud communication.

3. Robotics and Autonomy Integration

As autonomous tractors and robotic harvesters become commercially viable, the software connecting them becomes paramount. Digital farming software is evolving into the operating system for autonomous equipment, managing path planning, ensuring safety compliance, and coordinating fleets of automated machines.

4. Carbon Farming and Sustainability Software

Driven by corporate and regulatory Net-Zero commitments, new software platforms are emerging to help farmers measure, verify, and monetize sustainable practices (e.g., no-till farming, cover cropping). These platforms use remote sensing and complex models to estimate carbon sequestration, facilitating participation in voluntary carbon credit markets. This creates a powerful new revenue stream for farmers and a key strategic focus for software providers.

5. Increased Interoperability and Open Platforms

There is growing farmer fatigue with proprietary platforms that lock in their data. The trend is moving toward open-source or highly interoperable platforms (facilitated by initiatives like Agri-Data Sharing Frameworks) that allow farmers to choose best-in-class software components from different vendors without fear of data isolation.

Competitive Landscape

The Digital Farming Software Market is highly fragmented, featuring a complex mix of global industrial giants and agile, specialized tech startups.

Major Players

The competitive structure is categorized by their core offering:

Agricultural Equipment OEMs (Full Stack Providers): Companies like John Deere (via Operations Center) and Bayer Crop Science (via Climate FieldView) leverage their massive distribution networks and hardware integration to offer comprehensive, end-to-end platforms. Their strategy is often hardware-led, using software to enhance equipment value.

Pure-Play FMS Providers: Companies such as Granular (Corteva Agriscience) and Trimble Agriculture focus primarily on data management, farm record-keeping, and financial analysis, often remaining hardware-agnostic.

Specialized Analytics Providers: Smaller, innovative startups focusing on niche areas like specific disease modeling (e.g., vine disease) or satellite imagery analysis, offering highly technical, subscription-based tools.

Competitive Strategies

Ecosystem Lock-in (OEMs): John Deere’s strategy involves making its Operations Center the central data hub for all equipment, effectively creating high switching costs for farmers using their machinery.

Data Aggregation and Openness (Pure-Plays): Companies like Climate FieldView focus on integrating data from any source (any tractor, drone, or sensor) to become the single source of truth for the farmer's field data, competing on the quality and comprehensiveness of their analytics.

SaaS Model Expansion: The most profitable strategy involves shifting from perpetual software licenses to subscription-based SaaS models, ensuring recurring revenue and enabling continuous feature updates.

M&A Activity: Expect continued consolidation, with large seed/chemical companies and machinery OEMs acquiring AI and sensor startups to rapidly integrate cutting-edge technology into their existing platforms.

Regional Insights

Market maturity varies dramatically by region, largely depending on farm size, average farmer age, connectivity infrastructure, and government support for precision agriculture subsidies.

North America (NA)

North America holds the largest market share due to large-scale commercial farms, high technology adoption rates, and early penetration by major OEMs. High internet and mobile penetration enable sophisticated cloud-based solutions. The region leads in prescriptive analytics adoption and the integration of carbon management tools.

Europe

Europe is a mature market driven by strict Environmental, Social, and Governance (ESG) standards and the Common Agricultural Policy (CAP). Growth is robust, particularly in Western Europe, focusing on resource efficiency (water, nitrogen) and traceability software. The market is highly diverse, requiring tailored solutions for smaller, varied farm sizes compared to the US.

Asia-Pacific (APAC)

APAC is projected to be the fastest-growing market (highest CAGR). While adoption in countries like India and China is currently lower due to fragmented landholdings and lower average farm size, government initiatives, particularly in Japan and Australia, promoting smart agriculture and drone use are accelerating growth. The focus here is often on affordable, mobile-first solutions and managing complex tropical and semi-arid cropping systems.

Latin America (LATAM)

Driven by the massive soy, corn, and beef production sectors (Brazil, Argentina), LATAM is a rapidly developing market. Adoption is high among large corporate farms seeking to optimize massive land areas. Connectivity remains a challenge in remote areas, driving demand for edge computing and offline data processing capabilities.

Challenges & Risks

The pathway to full market potential is hindered by several significant barriers:

Digital Divide and Connectivity: In many rural areas globally, poor internet connectivity remains the single largest impediment to the effective deployment of real-time, cloud-based digital farming software.

Data Literacy and User Adoption: Many traditional farmers lack the technical literacy to fully utilize complex software interfaces. Adoption often fails if the solution is not intuitive, mobile-friendly, and immediately demonstrates a clear return on investment (ROI).

High Initial Cost: The combined capital expenditure for necessary hardware (sensors, drones, smart equipment) and the recurring subscription costs for premium software can be prohibitive for small and mid-sized farms.

Data Ownership and Privacy Concerns: Farmers are increasingly wary of sharing proprietary yield and soil data with third-party software providers, fearing that this data may be leveraged against them in commodity markets or by seed/chemical suppliers. Addressing trust is critical for market expansion.

Opportunities & Strategic Recommendations

The underlying market opportunity is vast: turning agricultural uncertainty into predictive certainty. Strategic entry and growth must focus on lowering barriers to entry and capitalizing on the sustainability mandate.

Opportunities

Micro-Farming and Vertical Agriculture: Develop software specifically tailored for the intense, controlled environment data sets generated by indoor/vertical farms, optimizing HVAC, light spectrum, and nutrient delivery with unparalleled precision.

Financializing Sustainability: The $7.1 billion market projection does not fully account for the value created by carbon sequestration tracking. Software that accurately verifies and trades carbon credits represents a multi-billion dollar opportunity.

AI-as-a-Service for Agronomy: Offer expert, AI-driven prescriptive advice (e.g., customized nitrogen application plans) as a premium service layer above basic FMS, providing high-margin, recurring revenue.

Strategic Recommendations for Stakeholders

For Software Startups (ISVs): Focus on building user interfaces that are as simple as consumer mobile apps (high UX/UI priority) and embrace open API architecture to ensure maximum hardware compatibility. Solve the connectivity problem by prioritizing offline and edge computing capabilities.

For Large Agribusinesses/OEMs: Accelerate the development of the "Data Trust" model. Implement transparent data privacy policies that clearly define data ownership (firmly with the farmer) and demonstrate how data is aggregated anonymously to benefit the entire ecosystem (e.g., better regional yield models).

For Investors: Prioritize investment in early-stage companies focused on predictive modeling (especially climate/disease risk) and sustainability verification software. These platforms offer high scalability and strong SaaS margins, unlike hardware-dependent solutions. Furthermore, invest in solutions that specifically target the massive APAC market with mobile-first, localized language interfaces and minimal connectivity requirements.

Browse trending Reports :

Global Nanomedicine in Central Nervous System Injury and Repair Market

Global Glucose Syrup Market

Global Agile IoT Market

Global Recycled Carbon Fiber Market

Global Automotive Embedded Systems in Automobile Market

Global Laser Cleaning Market

Global Skydiving Equipment Market

Asia-Pacific Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

Global Intestinal Pseudo Obstruction Treatment Market

Global Programmable Application Specific Integrated Circuit (ASIC) Market

Asia-Pacific Lung Cancer Diagnostics Market

Global B-cell lymphoma treatment Market

Global Portable Patient Isolation Market

Global Foodborne Trematodiases Disease Market

North America MDI, TDI, Polyurethane Market

Global Ozone Generator Market

Europe Specialty Gas Market

Global Automotive Seat Heater Market

Asia-Pacific Testing, Inspection, and Certification (TIC) Market for Building and Construction – Industry Trends and Forecast to 2028

Global Thrombocytopenia Market

Global Polyester Stick Packaging Market

Global Cloud Storage Market

Global Hammocks Market

Global Ready to Drink Alcoholic Tea Market

Middle East and Africa Flotation Reagents Market

Middle East and Africa Plastic Compounding Market

Global Potato Processing Market

North America q-PCR Reagents Market

Asia-Pacific Rowing Boats and Kayaks Market

Global Water Soluble NPK Fertilizers Market

Global Rowing Boats and Kayaks Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- [email protected]