India Immunoglobulin Market Analysis

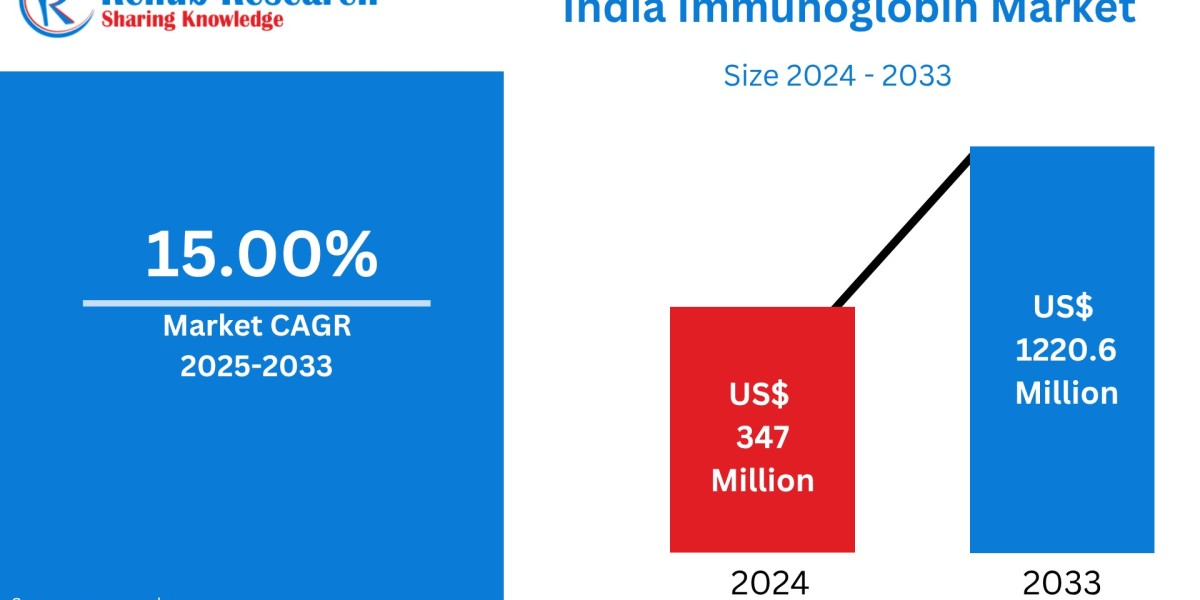

According to Renub Research India immunoglobulin market was valued at US$ 347 million in 2024 and is projected to reach US$ 1,220.6 million by 2033, expanding at a robust CAGR of 15.00% from 2025 to 2033. This strong growth trajectory is driven by the rising prevalence of immunodeficiency and autoimmune disorders, increasing adoption of plasma-derived therapies, favorable government initiatives, expanding healthcare awareness, and rapid growth in domestic plasma fractionation and manufacturing capabilities.

Together, these factors are significantly improving access to immunoglobulin therapies across India and broadening their clinical use in both acute and chronic disease management.

India Immunoglobulin Market Overview

Immunoglobulins, also known as antibodies, are specialized proteins produced by the immune system to identify and neutralize pathogens such as bacteria, viruses, and toxins. They play a fundamental role in immune defense by binding to specific antigens and triggering immune responses. Therapeutically, immunoglobulins are used to treat a wide range of conditions including primary immunodeficiency disorders, autoimmune diseases, neurological disorders, and certain infections.

There are five main classes of immunoglobulins—IgG, IgA, IgM, IgE, and IgD—each with distinct biological functions. Most therapeutic formulations are derived from human plasma and are administered intravenously or subcutaneously to patients with impaired or dysfunctional immune systems. In India, growing diagnostic capabilities and expanding healthcare infrastructure are accelerating the clinical adoption of immunoglobulin therapy.

Request a free sample copy of the report:https://www.renub.com/request-sample-page.php?gturl=india-immunoglobin-market-p.php

India Immunoglobulin Industry Overview

The immunoglobulin industry in India is undergoing rapid transformation, supported by advancements in plasma fractionation technologies, improved regulatory frameworks, and increasing domestic production. Historically dependent on imports, India is now witnessing significant investments in local manufacturing facilities, helping reduce supply constraints and treatment costs.

Rising awareness among healthcare professionals and patients, combined with improved access to specialty care, has led to earlier diagnosis and treatment of immune-related disorders. Government initiatives supporting biotechnology development and rare disease treatment are further strengthening the market ecosystem, making immunoglobulin therapy more accessible nationwide.

Growth Drivers for the India Immunoglobulin Market

The market’s growth is fueled by rising disease burden, technological advancements, healthcare modernization, and policy support. Increasing demand for long-term immune therapies is positioning immunoglobulins as a critical component of India’s evolving healthcare landscape.

Rising Prevalence of Immunodeficiency Disorders

A major driver of market growth is the increasing prevalence of primary immunodeficiency diseases (PIDs) and autoimmune disorders in India. PIDs encompass more than 450 rare genetic conditions that weaken immune function, leading to recurrent infections and chronic illness. India’s estimated PID incidence of 1 in 10,000 live births is higher than the global average.

Despite this, underdiagnosis remains a major challenge, with nearly 70% of cases going undetected. As awareness improves and diagnostic programs expand, more patients are being identified and treated, driving sustained demand for immunoglobulin therapy and supporting long-term market expansion.

Advancements in Plasma-Derived Therapies

Technological progress in plasma collection, fractionation, and purification has significantly enhanced the quality, safety, and availability of immunoglobulin products. These advancements have improved manufacturing efficiency, reduced wastage, and lowered dependency on imports.

Increased domestic plasma processing capacity, supported by government policies and private investment, is helping meet growing demand while improving affordability. As plasma-derived therapies continue to evolve, they are enabling broader clinical applications and better patient outcomes across India.

Increasing Healthcare Awareness and Diagnosis Rates

Rising healthcare awareness among the general population and medical professionals is playing a crucial role in market growth. Public health campaigns, improved access to specialists, and advancements in diagnostic technologies are enabling earlier and more accurate identification of immune-related disorders.

Early diagnosis allows timely initiation of immunoglobulin therapy, reducing complications and improving quality of life. Government-led health initiatives and insurance coverage expansion are further supporting treatment access, reinforcing demand growth across urban and semi-urban regions.

Challenges in the India Immunoglobulin Market

Despite strong growth prospects, the market faces structural and economic challenges that can limit broader adoption and equitable access.

High Cost of Immunoglobulin Therapies

The high cost of immunoglobulin therapy remains one of the most significant barriers in India. Plasma-derived products require complex manufacturing processes, strict quality control, and extensive regulatory compliance, all of which increase production costs.

For many patients, especially in rural and low-income populations, treatment affordability remains a concern. Dependence on imported raw plasma and finished products further escalates costs. Expanding domestic production capacity, improving plasma donation infrastructure, and increasing government reimbursement support are essential to overcoming this challenge.

Regulatory and Quality Control Issues

Immunoglobulin products are subject to stringent regulatory and quality standards to ensure safety and efficacy. Navigating complex approval processes can delay product launches and increase operational costs for manufacturers.

Ensuring consistent quality across plasma sources and manufacturing facilities is another challenge. Strengthening regulatory oversight, harmonizing standards with global benchmarks, and investing in quality assurance systems are critical to maintaining patient trust and supporting sustainable market growth.

India Immunoglobulin Market Segmentation by Product Type

By product type, the market includes IgG, IgA, IgM, IgE, and IgD. IgG dominates the market due to its broad therapeutic applications in immunodeficiency, autoimmune, and neurological disorders, while other classes serve niche clinical indications.

India Immunoglobulin Market Segmentation by Mode of Delivery

Based on mode of delivery, the market is segmented into intravenous immunoglobulin (IVIG) and subcutaneous immunoglobulin (SCIG). IVIG holds the larger share due to hospital-based administration, while SCIG is gaining traction for long-term therapy due to convenience and home-based treatment options.

India Immunoglobulin Market Segmentation by Application

Key applications include immunodeficiency diseases, CIDP, hypogammaglobulinemia, congenital AIDS, chronic lymphocytic leukemia, myasthenia gravis, multifocal motor neuropathy, immune thrombocytopenic purpura (ITP), Kawasaki disease, and others. Immunodeficiency disorders account for the largest share, supported by rising diagnosis rates.

India Immunoglobulin Market Segmentation by Region

Regionally, the market is divided into North, South, East, and West India. Southern and western regions dominate due to advanced healthcare infrastructure and higher awareness, while northern and eastern regions offer strong growth potential as access to specialty care improves.

Competitive Landscape of the India Immunoglobulin Market

The Indian immunoglobulin market is moderately competitive, with global and domestic players focusing on capacity expansion, strategic collaborations, and technology upgrades. Key players include Baxter International Inc., Grifols S.A., Bayer Healthcare, Takeda Pharmaceutical Company Limited, PlasmaGen BioSciences Pvt. Ltd., Reliance Life Sciences, Biocon Limited, Bharat Serums and Vaccines, Biological E Limited, Intas Pharmaceuticals, and Kedrion Biopharma.

Companies are evaluated based on company overview, leadership, recent developments, strategic initiatives, and sales performance.

Conclusion

The India immunoglobulin market is set for rapid expansion through 2033, driven by rising disease prevalence, technological advancements in plasma-derived therapies, increasing healthcare awareness, and growing domestic production capacity. While challenges such as high treatment costs and regulatory complexity remain, supportive government policies and industry investments are expected to improve accessibility and affordability. Immunoglobulin therapy will continue to play a critical role in strengthening India’s immune healthcare landscape and addressing unmet medical needs.