When a Frozen Account Becomes a Financial Emergency

Not every frozen bank account is a minor inconvenience. For many people, a sudden account freeze can spiral into a genuine financial emergency within hours. Rent is due tomorrow. A medical bill needs to be paid today. Your family depends on that account for daily groceries and essential needs.

If you are in that situation right now, this guide is written specifically for you. We will not waste your time with background theory. Instead, we will focus on the fastest and most effective actions you can take right now to unfreeze your bank account before the situation gets worse.

Time is critical — so let us get straight to it.

Why Urgency Changes Everything in a Bank Account Freeze

Most general guides treat a frozen bank account as a routine administrative matter. But when you have financial obligations pressing down on you from every direction, routine timelines are not acceptable.

The good news is that urgency actually works in your favor if you use it correctly. Banks have provisions for emergency fund access, expedited reviews, and hardship considerations that most customers never know to ask about. The key is knowing how to communicate your situation effectively and to the right people.

Understanding this distinction is what separates someone who waits two weeks to unfreeze their bank account from someone who resolves it in 48 hours.

Common Reasons Behind an Urgent Bank Account Freeze

Before taking emergency action, spend five minutes identifying the most likely cause. This shapes everything that follows.

Sudden Fraud Alert

Your bank's automated fraud detection system flagged a recent transaction as suspicious. This is actually the most common cause of unexpected freezes — and often one of the fastest to reverse once you confirm your identity and verify the transaction in question.

Unverified or Expired Identity Documents

Many banks conduct periodic KYC audits. If your documents were flagged as expired or inconsistent during a routine check, your account may have been restricted without you receiving a clear notification.

Creditor-Initiated Legal Action

An outstanding debt that escalated to a court order can result in an immediate account freeze. This type of freeze requires both financial resolution and legal steps, but can sometimes be partially lifted for basic living expenses through a court application.

Inactive or Dormant Account Status

If you have not used your account in over a year, the bank may have classified it as dormant and restricted access. This is one of the quickest types of freezes to reverse — often resolved within one to two business days.

Error or Mistaken Identity

Banks occasionally freeze the wrong account due to clerical errors, name similarities, or data mismatches. If you have no outstanding debts or compliance issues, this could be your situation — and it is typically resolved quickly once identified.

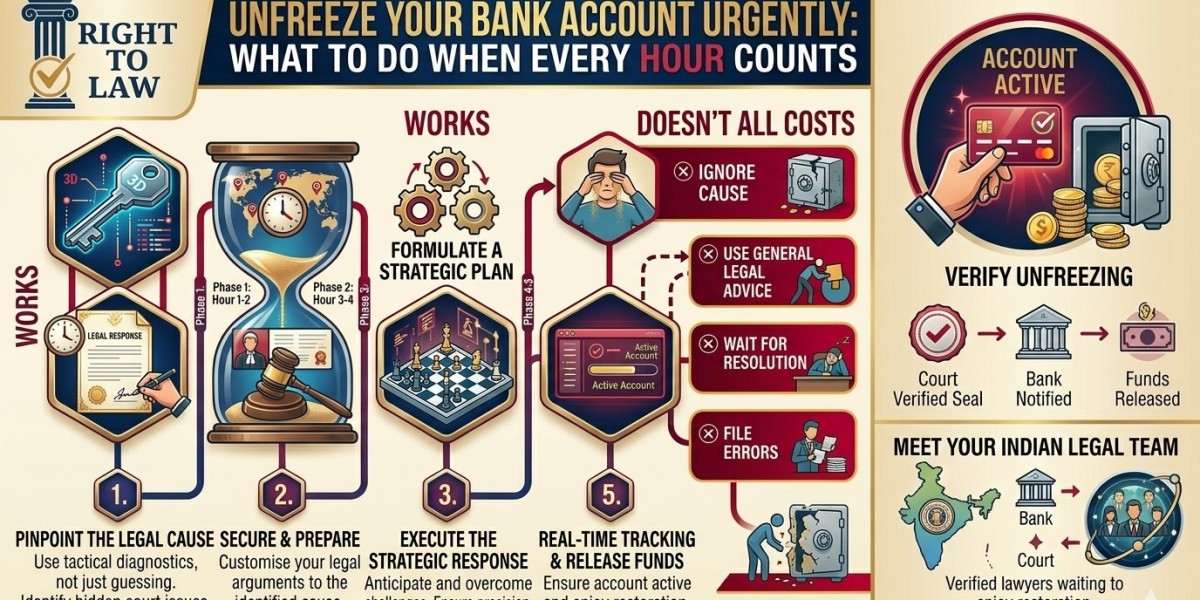

Emergency Steps to Unfreeze Your Bank Account Right Now

Step 1: Call the 24/7 Emergency Banking Helpline Immediately

Every major bank has a round-the-clock customer helpline for urgent matters. Call it now. Do not wait for branch opening hours. Explain that you have an urgent financial need and ask them to escalate your case immediately to the fraud or account review team. Use the words "urgent" and "financial hardship" clearly — these trigger priority handling protocols at most banks.

Step 2: Visit the Branch the Moment It Opens

If your phone call does not resolve the freeze, be at the bank branch the moment doors open. In-person visits carry significantly more weight than phone calls in urgent situations. Ask specifically to speak with the branch manager — not a teller or general customer service representative. Managers have greater authority to initiate expedited reviews.

Step 3: Submit an Emergency Hardship Request

Most people are unaware that banks offer emergency hardship provisions. If your account is frozen and you genuinely cannot meet basic living expenses, you can formally request emergency access to a limited portion of your funds. Ask the branch manager or compliance officer about your bank's hardship fund release policy and submit a written request immediately.

Step 4: Provide Complete Documentation on the Spot

Do not leave the branch to gather documents and return the next day. Walk in prepared. Bring your original government-issued photo ID, two recent proofs of address, your account details, and a brief written statement explaining your urgent financial need. Handing over a complete package on the spot dramatically reduces processing time.

Step 5: Request Same-Day Escalation to the Compliance Team

Politely but firmly request that your case be escalated to the compliance or risk management department on the same day. Ask for a direct callback from the compliance officer handling your case. Set a clear expectation — you need a response within 24 hours given your financial circumstances.

Step 6: Send a Formal Urgent Written Notice to the Bank

While at the branch or immediately after, send a formal email to the bank's official customer grievance address. State your account number, the reason for urgency, the financial impact of the freeze, and a reasonable deadline for resolution. Mark it clearly as urgent. A written communication creates a legal paper trail and signals to the bank that you are serious about escalating if needed.

If the Bank Cannot Help Immediately — Your Backup Options

While working to resolve the freeze, explore these emergency financial alternatives:

Use a Secondary Bank Account: If you have another account at a different bank, redirect all incoming payments there immediately. Notify your employer and anyone who regularly transfers money to you.

Request an Emergency Cash Advance: Some banks allow a limited cash advance from a frozen account for essential expenses. Ask specifically about this option at the branch.

Contact Family or Friends Temporarily: While not ideal, borrowing a small amount from a trusted person while your account is being unfrozen gives you breathing room without incurring debt from a lender.

Use a Prepaid Card or Digital Wallet: If you have funds accessible through a digital payment platform or prepaid card, use these to cover immediate necessities while the freeze is being resolved.

How to Prevent an Urgent Freeze Situation in the Future

Once you successfully unfreeze your bank account, put these safeguards in place immediately:

- Enable real-time SMS and email transaction alerts so you catch issues the moment they arise

- Keep a secondary bank account active at all times for emergencies

- Update your KYC documents with your bank every twelve months without waiting to be asked

- Maintain a small emergency cash reserve outside of digital banking for unexpected disruptions

- Set calendar reminders to make at least one transaction per quarter to prevent dormancy flags

Frequently Asked Questions

Can I get emergency access to my frozen account funds?

Yes, in certain circumstances. Banks have hardship provisions that may allow limited access to funds for essential living expenses. Ask your branch manager directly about this option and submit a written hardship request.

What is the fastest way to unfreeze a bank account?

The fastest approach is a combination of an immediate phone call to the emergency helpline followed by a same-day in-person branch visit with complete documentation ready to submit.

Can a frozen account affect my pending bill payments?

Yes. Automated bill payments and standing orders linked to a frozen account will fail. Contact your service providers and arrange alternative payment methods immediately to avoid late fees or service interruptions.

Conclusion: Act Now — Every Hour Matters

When your financial life depends on immediate access to your funds, waiting is not an option. The steps outlined in this guide are designed specifically for urgent situations where standard timelines simply will not do.

Call your bank right now, go to the branch first thing in the morning, request emergency hardship access, and submit a complete documentation package on the spot. Escalate aggressively but professionally, put everything in writing, and do not stop until you have a confirmed resolution in hand.

You have every right to unfreeze your bank account — and with the right approach, you can make it happen faster than you think.