overview

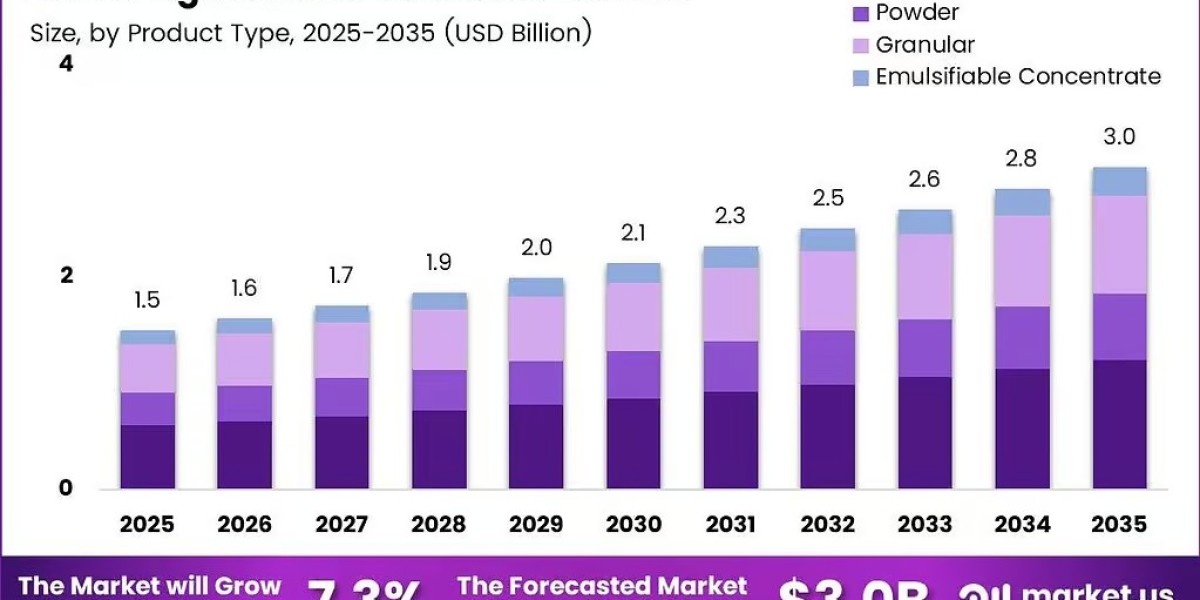

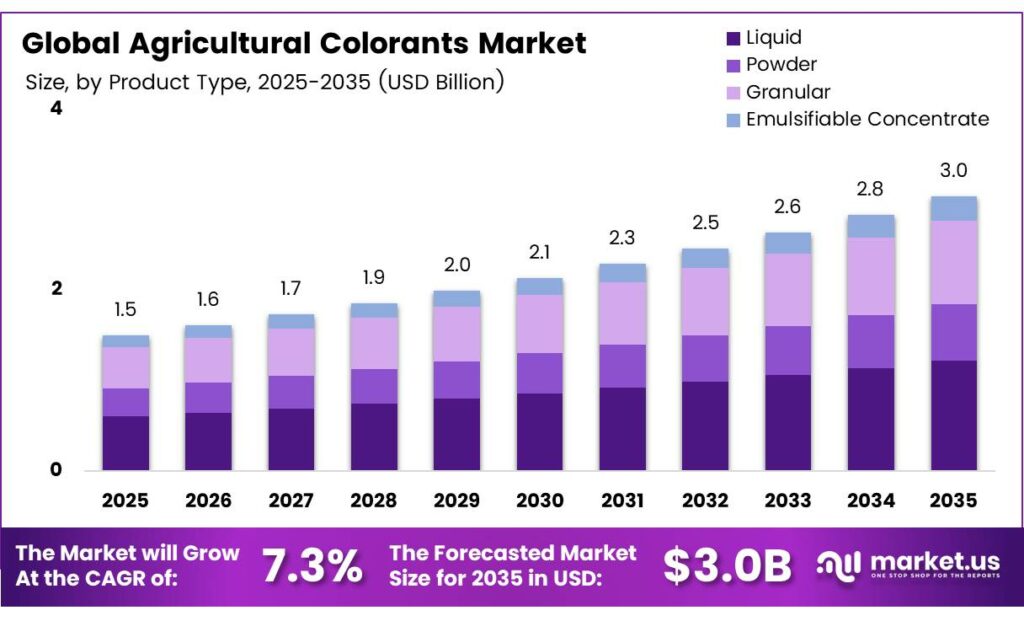

The Agricultural Colorants Market is projected to reach USD 3.0 billion by 2035 from USD 1.5 billion in 2025, growing at a 7.3% CAGR. Market expansion is supported by increasing demand for treated seeds, stricter compliance standards, and advancements in precision agriculture. Strong export activity from major producing regions continues to strengthen global supply chains.

Click to explore more: https://market.us/reports/food-and-beverages/

Key Takeaways

- The Global Agricultural Colorants Market was valued at USD 1.5 billion in 2025 and is projected to reach USD 3.0 billion by 2035, growing at a CAGR of 7.3%.

- Synthetic Colorants dominated the market, accounting for 67.8% of the total share in 2025.

- Liquid formulations held the largest share among formulation types, capturing 44.2% of the market.

- The Fertilizers segment led by application, representing 37.9% of the market.

- Crop Protection emerged as the leading end-use sector, securing a 44.7% market share.

- North America dominated the global market with a 33.6% share, valued at approximately USD 0.5 billion in 2025.

By Type Analysis

Synthetic Colorants dominate with 67.8% due to cost efficiency, chemical stability, and wide compatibility with agrochemical formulations.

In 2025, Synthetic Colorants held a dominant position in the Agricultural Colorants Market, accounting for 67.8% of the By Type segment. Their strong market presence is supported by cost-effectiveness, excellent stability, and compatibility with various agricultural formulations. Meanwhile, Natural Colorants are gaining attention due to increasing demand for sustainable and organic farming solutions, although higher costs and limited color options continue to restrict wider adoption.

Formulation Analysis

Liquid formulation dominates with 44.2% due to ease of mixing, superior compatibility with seed treatment machinery, and uniform coating performance.

In 2025, Liquid formulations held a dominant position in the Agricultural Colorants Market, capturing 44.2% of the By Formulation segment. Their popularity is driven by easy integration with automated seed treatment systems, efficient mixing, and consistent coating performance. Powder formulations remain important for cost-sensitive applications due to their storage stability and transport efficiency. Granular formulations are widely used in fertilizer and soil treatment applications, offering improved handling and safety benefits. Meanwhile, Emulsifiable Concentrates support pesticide and herbicide applications, with growing adoption in precision farming and advanced spraying technologies.

By Application Analysis

Fertilizers dominate with 37.9% due to mandatory color-coding standards and high global fertilizer consumption volumes.

In 2025, Fertilizers held a dominant position in the Agricultural Colorants Market, accounting for 37.9% of the By Application segment. Growth is driven by mandatory color-coding requirements, product differentiation needs, and widespread fertilizer use across global agriculture. Pesticides also represent a major application area, where colorants support product identification and regulatory compliance. Seeds utilize colorants for treatment verification and variety recognition, while Herbicides rely on colorants to improve product differentiation, reduce application errors, and enhance operational safety in farming activities.

By End-Use Analysis

Crop Protection dominates with 44.7% due to mandatory treatment marking requirements and high-volume agrochemical application across global farmlands.

In 2025, Crop Protection held a dominant position in the Agricultural Colorants Market, capturing 44.7% of the By End-Use segment. Demand is supported by regulatory requirements for treated product identification and the widespread use of agrochemicals across major crop categories. Horticulture utilizes colorants in specialty coatings and ornamental applications, benefiting from growth in premium crop production. Forestry relies on colorants for tree marking, seedling identification, and application tracking, while Aquaculture represents a growing niche segment where colorants support feed identification and monitoring through specialized water-stable formulations.

Key Market Segments

By Type

- Synthetic Colorants

- Natural Colorants

By Formulation

- Liquid

- Powder

- Granular

- Emulsifiable Concentrate

By Application

- Fertilizers

- Pesticides

- Seeds

- Herbicides

By End-Use

- Crop Protection

- Horticulture

- Forestry

- Aquaculture

Emerging Trends

Biodegradable Formulations and Smart Traceability Technologies Reshape Agricultural Colorant Demand

The Agricultural Colorants Market is witnessing growing demand for biodegradable and plant-based colorants as sustainability and organic farming gain momentum. Regulatory support for eco-friendly agricultural inputs is encouraging the adoption of bio-based alternatives. At the same time, liquid formulations continue to gain preference due to their compatibility with automated seed treatment systems and efficient application performance.

Drivers

Strict Seed Labeling Regulations and Precision Farming Adoption Drive Agricultural Colorant Market Growth

The Agricultural Colorants Market is driven by strict global seed labeling regulations requiring color-coded treated seeds across major regions. Strong agrochemical trade, including USD 268.1 million exports from the US in 2024, supports steady supply and demand. Growth in agrochemical use and companies like Bayer further strengthens consumption. Additionally, rising adoption of precision farming and drone-based spraying increases demand for advanced fluorescent colorants for accurate field application and monitoring.

Restraints

Raw Material Cost Volatility and Environmental Regulations Constrain Agricultural Colorant Market Expansion

The Agricultural Colorants Market is constrained by volatile petrochemical-based raw material costs, which pressure margins and disrupt pricing stability. A 11.1% decline in Consumer Protection segment sales in 2024 also indicates softer agrochemical demand. Additionally, strict environmental rules limiting heavy metals and VOCs increase compliance costs and slow product approvals, particularly impacting smaller manufacturers.

Growth Factors

Circular Economy Initiatives and High-Value Seed Market Expansion Accelerate Agricultural Colorant Growth

Circular economy adoption is boosting demand for agro-waste-derived natural pigments, including extracts from fruit skins, plant waste, and algae biomass. These sustainable sources support net-zero farming goals and reduce reliance on petrochemical inputs. At the same time, strong agrochemical activity is driving market expansion, with Agricultural Solutions sales reaching €9,798 million in 2024, including €1,135 million from Asia. Growth in high-value hybrid seeds, ornamental horticulture, and turf management is also increasing demand for advanced colorant systems, while UV-fluorescent technologies enhance digital monitoring and compliance in modern agriculture.