There’s a phrase making rounds in enterprise tech right now: “Agentic AI is a moment of strategic divergence.” McKinsey said it. And while the mortgage industry has always been slow to absorb big technology shifts, the appraisal management sector is about to find out what “strategic divergence” really means the hard way.

For years, AMCs competed on turn time, panel size, and compliance track records. Those still matter. But a new competitive layer is forming beneath those basics, and it’s being built by AI that doesn’t wait to be told what to do.

This is the era of agentic AI, and it’s rewriting what operational excellence looks like for an AMC.

What Exactly Is Agentic AI and Why Should AMC Operators Care?

Agentic AI isn’t a chatbot. It’s not a dashboard. It’s a class of autonomous systems that observe, reason, decide, and act across multiple workflows without a human issuing command at each step.

Think of traditional AMC software: it automates rules. “If an order comes in for ZIP code X, assign appraiser Y.” That’s a rule-based automation of a checklist executed by a machine.

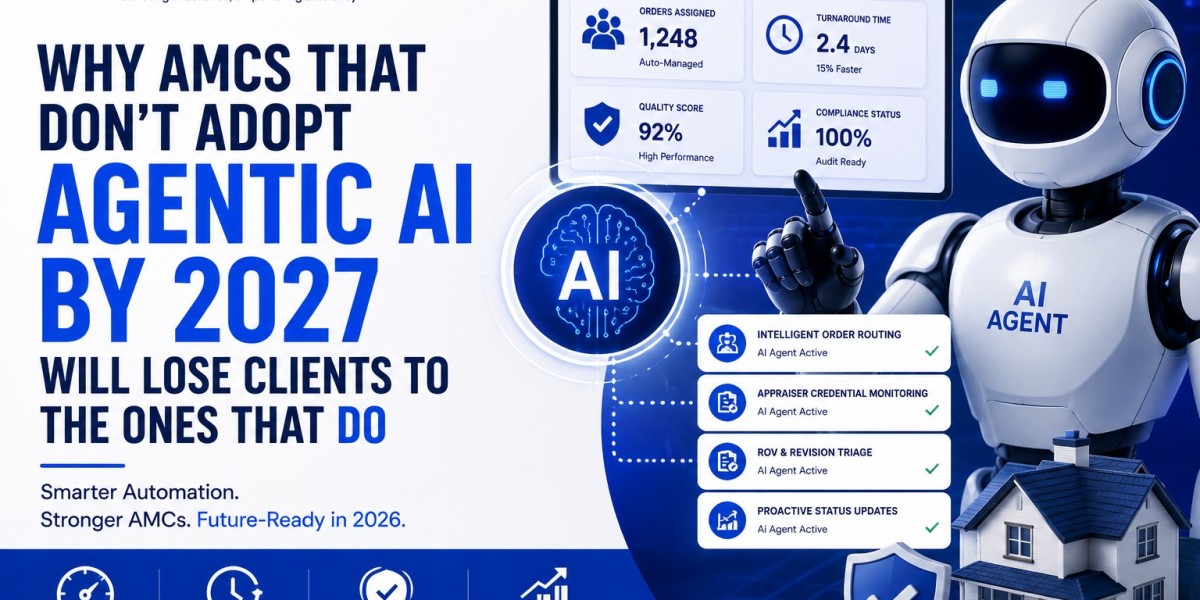

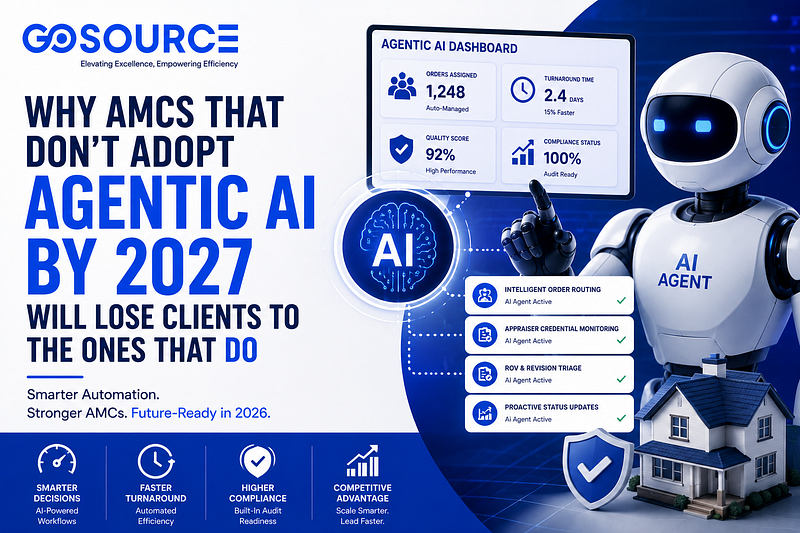

Agentic AI is different. It pursues goals. It can receive a high-level objective like “ensure all active orders are assigned within 4 hours while maintaining an appraiser quality score above 85%” and then independently route orders, monitor appraiser capacity, flag capacity crunches, escalate stalled orders, and re-route if quality thresholds dip, all without a coordinator touching the queue.

The business case is striking. Gartner projects that by the end of 2026, 40% of enterprise applications will include task-specific AI agents, and by 2028, 15% of day-to-day work decisions across industries will be made autonomously through agentic AI systems. AMC operations, which are fundamentally high-volume, rule-governed, decision-intensive workflows,

The Four AMC Workflows That Agentic AI Will Automate First

1. Intelligent Order Routing Beyond Round-Robin

Most AMCs still rely on geographic rotation logic to assign orders. It’s simple, defensible, and increasingly inadequate. Agentic order routing systems can simultaneously evaluate appraiser license status, current workload, historical turn time by property type, GSE-specific acceptance rates, and recency of rural market experience then make an assignment that a human coordinator couldn’t compute in 30 minutes of manual review, in under 3 seconds.

This is especially critical for heading into the UAD 3.6 mandatory deadline. UAD 3.6, mandated starting November 2, 2026, for conventional loans, is designed to standardize appraisal data in a more structured format and reduce unstructured free text, which makes automation easier and more reliable for lenders, the GSEs, and technology vendors. As data becomes more structured, agentic routing engines will have richer inputs to work with, making smarter assignment decisions at even greater speed.

2. Appraiser Panel Credential Monitoring

License expirations, E&O lapses, and geographic coverage gaps are perennial AMC compliance risks. Today, most platforms handle this with automated alerts, which still require a human to act. Agentic systems close to that loop. They don’t just alert; they remove the appraiser from the active assignment pool, notify the appraiser directly, and flag the coverage gap to operations all before the expiration date, which causes a compliance failure.

3. ROV and Revision Triage

Reconsideration of Value requests are one of the highest-touch, most time-intensive tasks in an AMC’s workflow. Agentic AI systems can be trained to classify incoming ROV requests by type (comparable selection dispute vs. condition error vs. market conditions argument), route them to the appropriate reviewer, and pre-populate relevant comparable data cutting the average ROV handling time by a significant margin.

4. Lender Communication and Status Updates

Lender portals help, but proactive outreach still falls on coordinators. Agentic AI can monitor every active order, detect orders at risk of missing SLA windows, and dispatch customized status updates to lender contacts without a coordinator drafting a single email.

The Competitive Threat AMCs Are Not Watching Closely Enough

Here’s the part that should genuinely concern AMC operators: the disruption isn’t only coming from software vendors. It’s coming from lenders themselves.

A new appraisal management platform called PAM allows mortgage lenders to manage appraisal workflows internally while tracking compliance and AIR rotation, claiming it can reduce appraisal fees by 25% to 40% with a flat $99 per-order charge. The pitch to lenders is blunt: why pay an AMC markup when you can run the workflow yourself?

The answer, right now, is operational complexity. Lenders don’t want to manage appraiser panels, credential tracking, quality review, and USPAP compliance. That’s the AMC’s value. But as agentic platforms make those functions automatable by non-specialists, the argument for outsourcing weakens unless AMCs are delivering something genuinely beyond what a lender-run system can replicate.

The AMCs that survive this shift will be the ones that use agentic AI not just to automate the routine, but to deliver analytical depth and quality outcomes that a lender’s internal team simply cannot match.

What “Human in the Loop” Actually Means in an Agentic AMC Model

One important clarification for AMC operators exploring agentic AI: this isn’t about removing human oversight. Industry leaders have emphasized that as modernization accelerates, human oversight remains an essential part of the process. The differentiator among valuation providers will be analytics and evidence, not just speed.

The right model is supervising autonomy agents to handle high-volume, rules-based, time-sensitive decisions; humans handle judgment calls, exceptions, client relationships, and quality escalations. This mirrors how leading enterprises are deploying agentic systems in other regulated industries, where governance requirements include transaction limits, human approval for high-risk actions, and complete audit logs that record every action and the reasoning behind it.

For AMCs operating under AIR, Dodd-Frank, and state-level AMC registration requirements, that audit trail isn’t optional; it’s the backbone of compliance for the entire operation.

How Go Source Valuation Approaches Operational Automation

At Go Source Valuation, operational support for AMCs is built around exactly this principle: scalable, intelligent workflow support that frees AMC operators from coordination bottlenecks without sacrificing compliance or quality oversight. As agentic AI capabilities continue to mature, AMCs that have already invested in streamlined back-office infrastructure will integrate these tools far more effectively than those still running manual processes.

If your AMC is evaluating how to position its operations for the agentic AI era, from smarter panel management to ROV workflow, redesign and explore how Go Source Valuations AMC management solutions are built to scale alongside emerging automation technology.

FAQ: Agentic AI for Appraisal Management Companies

Q: Is agentic AI the same as automated valuation models (AVMs)?

No. AVMs generate property value estimates using statistical models and property data. “Agentic AI” refers to autonomous workflow systems that manage processes like order routing, credential monitoring, and status of communication across an AMC’s operation. They serve very different functions.

Q: Does agentic AI raise compliance risks for AMCs?

Managed correctly, it reduces them. The key is ensuring audit trails, human escalation paths, and clear governance frameworks are built into any agentic system. AMCs should evaluate vendors on their compliance infrastructure, not just their automation claims.

Q: How does UAD 3.6 interact with agentic AI adoption?

UAD 3.6’s structured data format makes it significantly easier for agentic systems to process appraisal data automatically. AMCs that prepare their workflows for UAD 3.6 compliance are simultaneously building the data infrastructure that agentic AI needs to function effectively.

Q: What’s the first agentic AI use case AMCs should pilot?

Appraiser panel credential monitoring is typically the lowest-risk, highest-ROI starting point. It’s rule-governed, the stakes of failure are clear, and the volume of monitoring tasks makes automation immediately impactful.