Overview

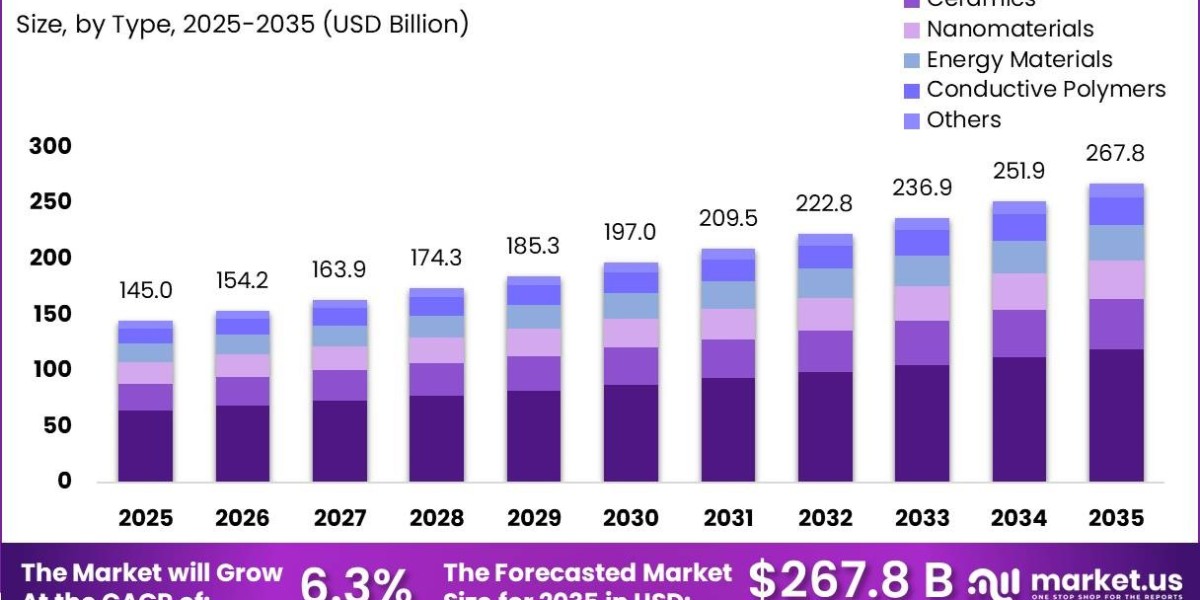

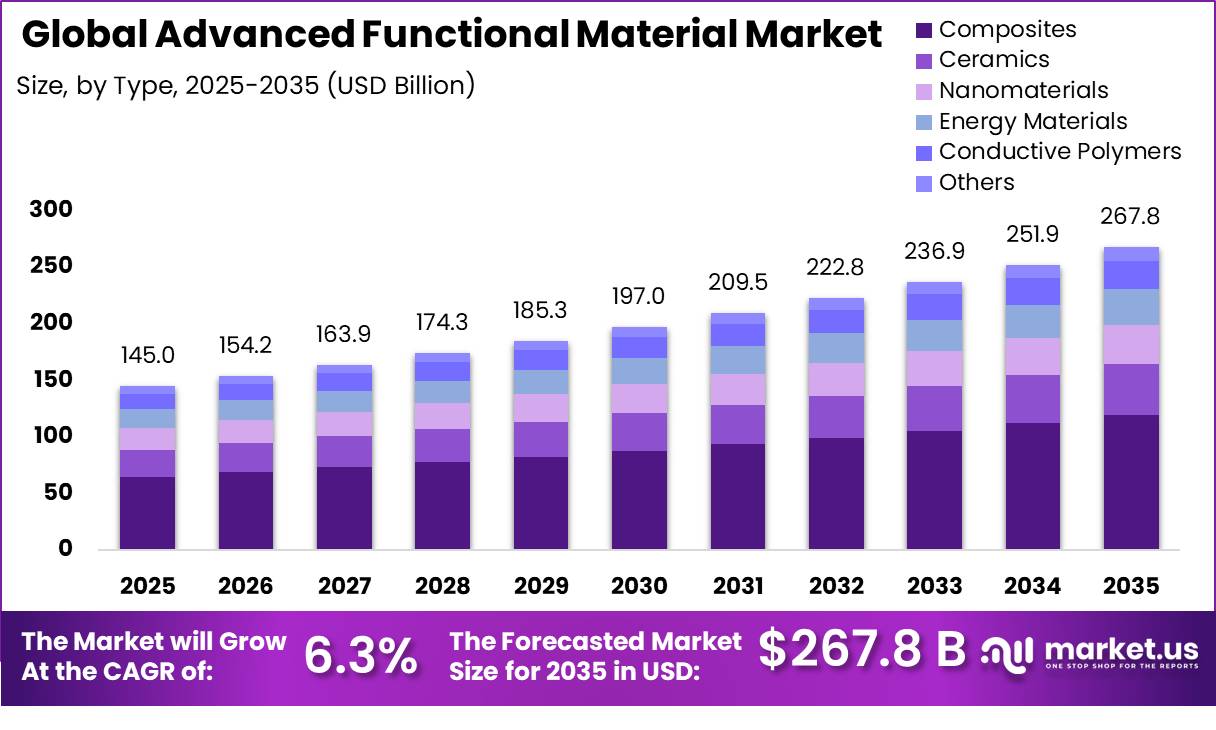

Advanced Functional Material Market is expanding steadily as advanced ceramics, composites, nanomaterials, and conductive polymers become increasingly important in modern industrial applications. The market was valued at USD 145.0 Billion in 2025 and is expected to reach USD 267.8 Billion by 2035, advancing at a CAGR of 6.3%. Dominated by Asia-Pacific with more than 45.0% share, the market is supported by growth in EV batteries, semiconductors, artificial intelligence infrastructure, and renewable energy systems.

Click to explore more: https://market.us/reports/chemical-and-materials/

Key Takeaways

The Global Advanced Functional Material Market was valued at USD 145.0 Billion in 2025.

The market is expected to reach USD 267.8 Billion by 2035, growing at a CAGR of 6.3% during the forecast period.

Composites emerged as the leading material type, accounting for 44.7% of the market in 2025.

The Electrical and Electronics sector dominated end-user demand with a market share of 35.0%.

Asia-Pacific held the largest regional share of more than 45.0%, generating USD 65.25 Billion in revenue during 2025.

Growing deployment of electric vehicles, expansion of semiconductor manufacturing, and increasing investments in advanced battery technologies continue to drive market growth.

Analysis Sections

Type Analysis

In 2025, Composites accounted for a dominant 44.7% share of the Advanced Functional Material Market. Their leadership position is attributed to their superior strength-to-weight ratio, corrosion resistance, durability, and design flexibility. These materials are widely used across aerospace, automotive, wind energy, and electrical applications where performance optimization and weight reduction are critical.

The growing use of carbon fibre reinforced polymer composites, glass fibre composites, and ceramic matrix composites has significantly expanded their application base. Advanced composite technologies are increasingly being adopted to improve energy efficiency and structural performance. According to initiatives led by DOE’s IACMI institute, efforts are underway to develop lower-cost manufacturing techniques and recycling processes for advanced composites. In automotive applications, composites can provide approximately 25–70% mass reduction compared with traditional steel structures, further strengthening their market demand.

End-User Industry Analysis

The Electrical and Electronics industry represented the largest end-user segment, accounting for 35.0% of the market in 2025. This dominance is supported by the industry's growing requirement for highly specialized materials capable of delivering superior electrical, thermal, magnetic, and mechanical performance.

Advanced functional materials are extensively used in semiconductor substrates, printed circuit boards, conductive polymers, insulating ceramics, and electromagnetic shielding composites. The ongoing trend toward electronics miniaturization, coupled with increasing deployment of artificial intelligence, high-performance computing, and advanced consumer devices, continues to increase demand for next-generation material solutions.

Furthermore, the rapid growth of AI data centers is generating strong demand for advanced thermal management materials, high-frequency dielectric ceramics, and conductive polymer substrates that can support higher processing power and improved operational efficiency.

Key Market Segments

By Type

- Composites

- Ceramics

- Nanomaterials

- Energy Materials

- Conductive Polymers

- Others

By End-User Industry

- Electrical and Electronics

- Automotive

- Aerospace and Defense

- Healthcare

- Energy and Power

- Others

Driving Factors

One of the primary growth drivers for the Advanced Functional Material Market is the increasing convergence of additive manufacturing and smart materials. The global additive manufacturing market is estimated at approximately USD 28.27–31.48 billion in 2026 and is projected to reach USD 59.27–114.45 billion by 2030–2033, expanding at a CAGR of 20.3%–24.0%. Meanwhile, metal 3D printing is growing at more than 25% annually.

This growth is increasing demand for premium metallic powders such as titanium, Inconel 718, and cobalt-chrome, along with advanced polymers including PEEK and ULTEM, which command prices approximately 3–8 times higher than conventional materials.

The expansion of electric vehicle production also remains a major growth catalyst. According to the International Energy Agency, global electric car sales surpassed 17 million units in 2024, representing more than 20% of total global vehicle sales. Rising battery deployment and electrification are driving demand for cathode, anode, separator, electrolyte, thermal-management, and lightweight composite materials.

Additionally, the growth of the semiconductor sector is creating substantial opportunities. The Semiconductor Industry Association reported global semiconductor sales of US$627.6 billion in 2024. Increasing adoption of artificial intelligence, advanced computing technologies, and next-generation electronic devices is strengthening demand for specialty semiconductor materials, advanced substrates, and high-purity chemicals.

Government initiatives are also accelerating market development. The U.S. Department of Energy has allocated USD 3 billion under its Battery Materials Processing Grants program, while additional funding of up to USD 725 million has been proposed to support domestic battery materials and advanced battery technologies. Similar initiatives under the European Critical Raw Materials Act are encouraging local extraction, processing, and recycling capabilities.

Restraining Factors

A major challenge affecting market expansion is the increasing regulatory pressure on PFAS chemicals. These substances are commonly used in fluoropolymer coatings, membranes, and advanced dielectric materials, making them important components within several advanced functional material applications.

Under the proposed EU REACH restrictions, implementation is expected to begin from December 2026, with transition periods extending into 2027. The regulations target fluorinated materials exceeding 25 ppb for individual PFAS substances and 250 ppb for combined concentrations.

Compliance creates substantial financial burdens for manufacturers. Reformulation costs are estimated between USD 50,000–500,000 per product line, while total compliance expenditures for mid-sized producers may range from USD 5–20 million. Furthermore, qualification cycles lasting approximately 12–36 months for PFAS-free alternatives could delay commercialization and slow market growth through 2029.

Growth Opportunity

The development of the blue economy and carbon capture technologies presents a significant long-term growth opportunity for the Advanced Functional Material Market. Government-backed sustainability initiatives and increasing investment in environmental technologies are supporting demand for specialized advanced materials.

In 2026, the EU Sustainable Blue Economy Partnership funded 24 research and innovation projects with a combined investment of €40 million. This funding is creating opportunities for advanced anti-biofouling coatings, corrosion-resistant marine materials, and seawater electrolyzer components.

Carbon capture technologies also represent a promising avenue for future growth. The U.S. DOE 45Q tax credit offers up to USD 180 per tonne of permanently captured CO₂, encouraging adoption of advanced sorbent materials. As a result, the carbon capture sorbent materials market is projected to reach approximately USD 2.8–3.5 billion by 2030, creating attractive opportunities for early suppliers of advanced functional materials across emerging sustainability-focused industries.