Overview

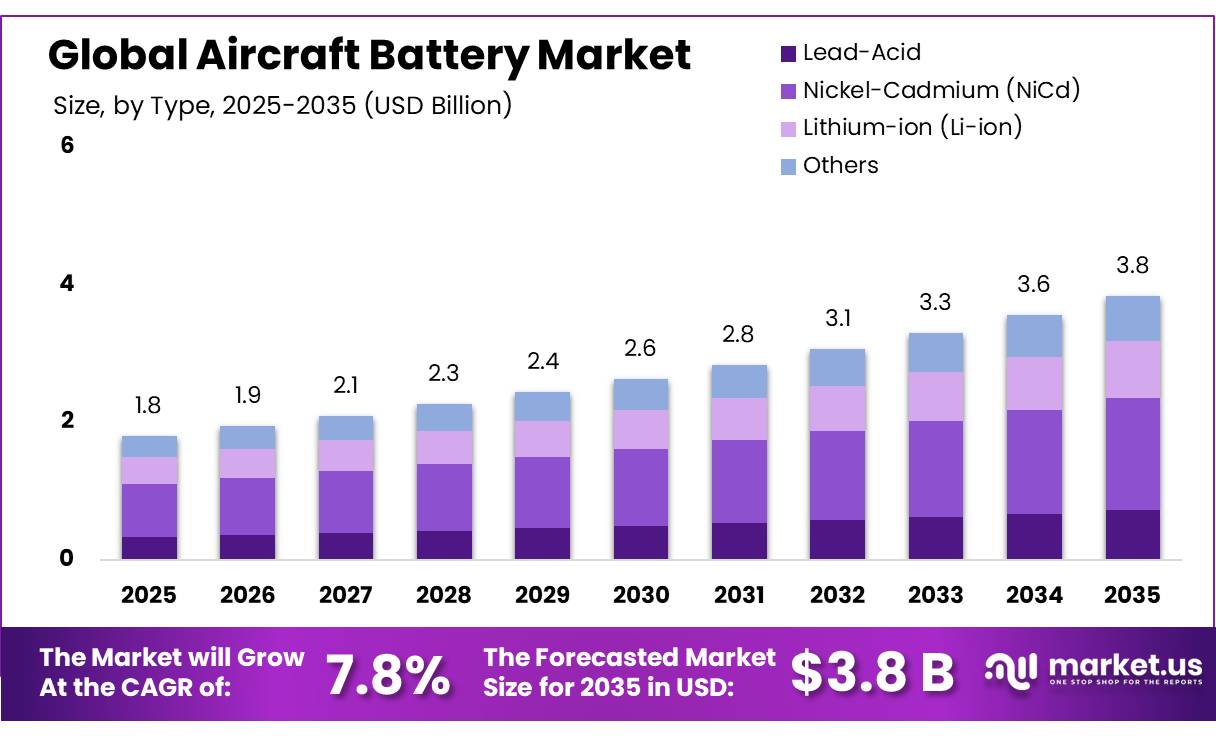

Aircraft Battery Market is expanding as aviation operators increasingly adopt efficient energy storage systems for commercial, military, and unmanned aircraft. The market size is projected to rise from USD 1.8 Billion in 2025 to USD 3.8 Billion by 2035, advancing at a CAGR of 7.8%. In 2025, North America accounted for 35.2% of the market and generated USD 0.6 Billion. Growing electrification and advancements in battery chemistry continue to drive industry demand.

Key Takeaways

The global Aircraft Battery Market was valued at USD 1.8 Billion in 2025 and is expected to reach USD 3.8 Billion by 2035, expanding at a CAGR of 7.8%. North America accounted for 35.2% of global revenue in 2025. By type, Nickel-Cadmium (Ni-Cd) Batteries led with 42.6% market share. By capacity, Above 20 Ah Batteries represented 56.3% of demand. The 100–300 Wh/kg segment accounted for 40.9% of the market by power density. Commercial Aviation captured 43.8% share among aircraft types, while Auxiliary Power Units (APU) held 29.4% of application revenue.

Type Analysis

Nickel-Cadmium (Ni-Cd) Batteries Dominated the Market

Nickel-Cadmium (Ni-Cd) Batteries accounted for 42.6% of the market due to their proven reliability in aviation environments. These batteries perform effectively across wide temperature ranges, support high discharge rates, and withstand significant mechanical stress. Such characteristics make them suitable for safety-critical aircraft operations.

The segment continues to benefit from extensive deployment across commercial aviation, military aviation, and general aviation platforms. Their ability to maintain stable voltage output and deliver consistent performance through multiple charge-discharge cycles supports long-term adoption. Established certification standards and compatibility with existing aircraft systems further reinforce their market position despite growing interest in lithium-ion technologies.

Capacity Analysis

Above 20 Ah Batteries Held the Largest Share

The Above 20 Ah segment represented 56.3% of total market demand. These batteries are widely used in commercial and military aircraft where high-load applications require dependable and sustained power output.

Their adoption is driven by the need to support engine starting systems, emergency backup functions, and Auxiliary Power Units (APU). Growing aircraft electrification and increasing integration of advanced avionics systems continue to strengthen demand for higher-capacity batteries. Longer service life and reduced replacement frequency also contribute to improved operational efficiency for fleet operators.

Power Density Analysis

100–300 Wh/kg Batteries Led the Market

The 100–300 Wh/kg power density segment accounted for 40.9% of the market. This category offers an effective balance between energy output, weight reduction, and operational safety requirements.

The segment is closely associated with advanced lithium-ion battery systems increasingly deployed in modern aircraft and unmanned aerial vehicles (UAVs). Lower weight compared to traditional battery chemistries contributes to better fuel efficiency and enhanced aircraft range. Improvements in thermal management and battery management systems continue to support the adoption of batteries within this power density range.

Aircraft Type Analysis

Commercial Aviation Accounted for the Largest Share

Commercial Aviation represented 43.8% of total market demand. The large global passenger aircraft fleet and high utilization rates create substantial demand for reliable battery systems.

Aircraft batteries perform essential functions including engine starting, backup power supply, and avionics support. Fleet modernization initiatives and continued growth in air passenger traffic further contribute to battery demand. Increasing implementation of more-electric aircraft architectures is raising onboard electrical requirements, strengthening the role of advanced energy storage systems across commercial fleets.

Application Analysis

Auxiliary Power Units (APU) Generated Significant Demand

The Auxiliary Power Unit (APU) segment held 29.4% of market revenue. Aircraft batteries are critical for initiating APU operations, which provide electrical power, pneumatic pressure, and environmental control when aircraft engines are inactive.

Consistent use of APUs during flight cycles creates stable replacement demand and supports aftermarket consumption. Increasing aircraft electrification and stringent aviation safety requirements continue to reinforce the importance of dependable battery technologies capable of performing under diverse operational conditions.

Key Market Segments

By Type

- Lead-Acid

- Nickel-Cadmium (Ni-Cd)

- Lithium-ion (Li-ion)

- Others

By Capacity

- Up to 20 AH

- Above 20 AH

By Power Density

- Up to 100 WH/KG

- 100-300 WH/KG

- Above 300 WH/KG

By Aircraft Type

- General Aviation

- Commercial Aviation

- Military Aviation

- Unmanned Aerial Vehicles

By Application

- Propulsion

- Auxiliary Power Unit (APU)

- Emergency/Backup

- Avionics and Cabin

- Others

By End-User

- OEM

- Aftermarket

Driving Factors

Smart BMS and Predictive Maintenance Adoption

The adoption of Smart Battery Management Systems (BMS) is becoming an important growth factor for the market. Embedded monitoring capabilities improve safety, extend battery life, and enable data-driven lifecycle management. In Singapore, CAAS-approved modification pathways expanded to 12 aircraft types by 2025, while local MRO capacity utilization reached 87% in 2024, highlighting increasing integration of intelligent battery solutions.

Predictive monitoring helps reduce unscheduled battery removals, optimize spare inventory planning, and support premium service agreements. Suppliers with access to battery health data benefit from stronger aftermarket opportunities and higher customer retention. This trend is expected to contribute approximately +0.9 percentage points to long-term market growth.

Restraining Factors

Thermal Runaway Risk

Thermal runaway remains a major challenge for aviation battery adoption. The FAA recorded 93 lithium battery air incidents in 2025, representing an increase of approximately 4.5% compared with 2024. In response, IATA strengthened handling requirements during 2025–2026, including limits on battery state of charge and additional transport provisions effective from January 1, 2026.

These safety concerns contribute to longer certification timelines, higher containment and monitoring costs, increased logistics complexity, and cautious insurance assessments. As a result, aviation battery system costs may rise by 8–15%, potentially reducing adoption rates and lowering forecast growth by approximately 1.6 percentage points.

Growth Opportunity

Recycling and Second-Life Battery Ecosystems

Battery recycling and second-life utilization represent a significant future opportunity for the Aircraft Battery Market. Although retirement volumes remain limited today, growing numbers of aircraft and eVTOL batteries reaching end-of-life are expected to create new opportunities in material recovery and energy storage reuse during the early 2030s.

Broader battery industry trends indicate strong potential. EV battery recycling is projected to increase from $3.82 billion in 2025 to $4.88 billion in 2026. Research also shows repurposed batteries can retain 70–80% of their original capacity and reduce storage costs by approximately 40% in suitable stationary applications. Recovering valuable materials such as lithium, cobalt, nickel, and manganese can improve lifecycle profitability, while economically reusing 10–15% of retired aviation batteries could increase gross profit per original battery pack by 5–9% and support approximately +1.0 percentage point of long-term market growth.