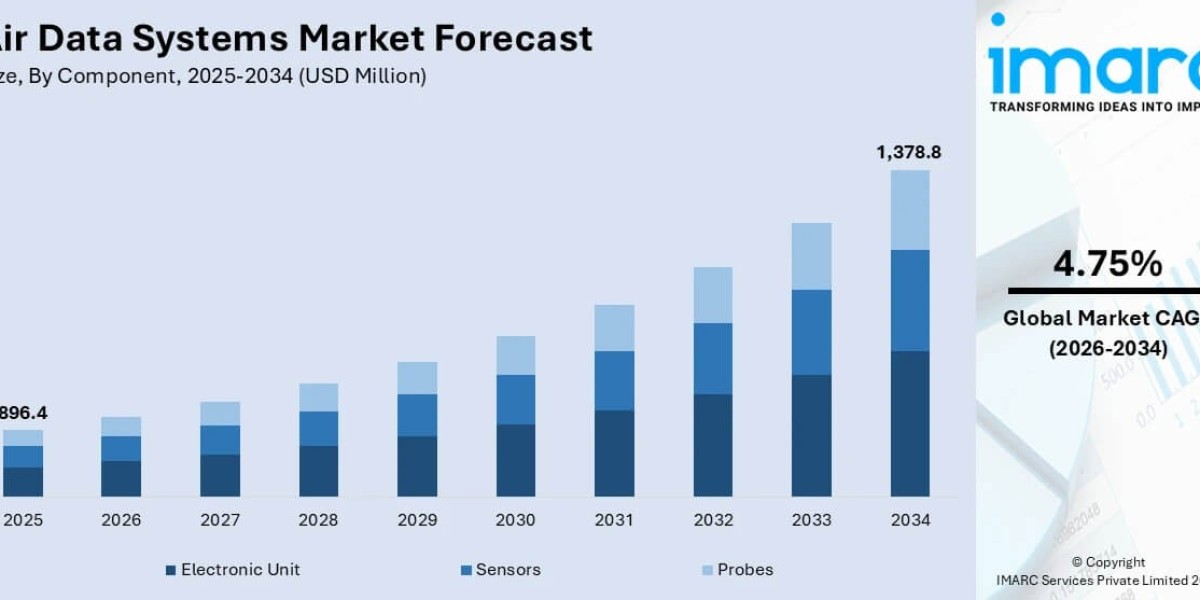

The global air data systems market size reached USD 896.4 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,378.8 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 4.75% during 2026-2034. The market is being driven by the growing need for precise flight data, rising adoption of unmanned aerial vehicles (UAVs) across military and commercial applications, and increasing investments in the global aerospace industry. In addition, the growing use of air data systems in civil aviation, military aircraft, and next-generation aircraft platforms is strengthening market growth. These systems play a critical role in delivering real-time information such as airspeed, altitude, angle of attack, temperature, and pressure, enabling safer and more efficient aircraft operations worldwide.

Market At a Glance

- Base Year: 2025

- Forecast Period: 2026-2034

- Market Size (2025): USD 896.4 Million

- Market Forecast (2034): USD 1,378.8 Million

- CAGR (2026-2034): 4.75%

- Leading Region: North America

Request for a Sample Report for Detailed Evaluation: https://www.imarcgroup.com/air-data-systems-market/requestsample

Key Highlights of the Air Data Systems Market Report

- Market Size & Growth: The global air data systems market was valued at USD 896.4 Million in 2025 and is projected to reach USD 1,378.8 Million by 2034, registering a CAGR of 4.75% during the forecast period.

- Regional Leadership: North America dominates the global air data systems market, supported by rising commercial aircraft production, growing partnerships among aerospace manufacturers, and strong investments in advanced aviation technologies.

- By Component – Electronic Unit: Electronic units hold the leading position in the component segment as they are essential for processing, analyzing, and calculating collected air data while enhancing aircraft performance and safety.

- By Aircraft Type – Narrow Body Aircraft: Narrow body aircraft represent the dominant aircraft type segment due to their widespread use in short-haul domestic and international travel, lower operational costs, and fuel-efficient performance.

- By End User – Civil: The civil segment accounts for the largest market share, driven by increasing global air travel, rising tourism activity, growing demand for commercial aircraft, and expanding passenger traffic worldwide.

- Key Market Drivers: Rising demand for accurate flight performance data, growing adoption of UAVs in military and commercial applications, and increasing aerospace investments are the primary factors supporting market expansion.

- Key Market Trends: Key trends include growing integration of advanced air data computers in modern aircraft, increased use of lightweight and digital monitoring systems, rising deployment in UAV platforms, and ongoing product innovation by major aerospace component manufacturers.

- Key Market Challenges: Major challenges include high integration and maintenance costs, stringent aviation certification requirements, and the technical complexity of ensuring high reliability across commercial, defense, and unmanned aircraft platforms.

- Key Players: Leading companies profiled in the report include Aeroprobe Corporation, Ametek Inc., Collins Aerospace, Curtiss-Wright Corporation, Honeywell International Inc., Meggitt (UK) Ltd., and Shadin Avionics.

Market Drivers, Challenges & Opportunities

Major Market Drivers

Growing Need for Accurate Flight Performance Data

Air data systems are essential for delivering precise information on airspeed, altitude, pressure, temperature, and angle of attack, all of which are critical to safe and efficient aircraft operation. As airlines, business jet operators, and military fleets increasingly prioritize flight accuracy, safety, and predictive maintenance, the demand for advanced air data systems continues to rise.

Expanding UAV Deployment Across Civil and Defense Applications

The rapid growth of UAVs for military surveillance, border security, mapping, agriculture, and industrial inspection is creating a strong demand for compact and reliable air data systems. These systems help UAV operators monitor flight conditions, improve stability, and enhance mission efficiency.

Rising Aerospace and Defense Investments

Governments and aerospace companies worldwide are investing heavily in commercial aircraft, fighter jets, transport aircraft, and avionics modernization. This is driving the integration of advanced air data systems into new aircraft platforms and retrofit programs across civil and military aviation.

Key Challenges

High Certification and Integration Complexity

Air data systems must meet strict aviation safety and certification standards, which increases development timelines and product integration complexity. Ensuring high reliability across different aircraft platforms also raises engineering and compliance costs.

Maintenance and Upgrade Costs

Modern air data systems require periodic calibration, maintenance, and compatibility with evolving avionics architectures. For operators managing large fleets, the cost of maintaining and upgrading these systems can be significant.

Emerging Opportunities

Next-Generation Digital Air Data Computers

The shift toward lightweight, digital, and more integrated air data computers offers a major opportunity for suppliers. These systems can improve flight performance monitoring, reduce aircraft weight, and enhance system reliability.

UAV and Advanced Military Aircraft Programs

As governments expand procurement of advanced UAVs, surveillance aircraft, and modern fighter platforms, demand for compact, high-accuracy air data systems is expected to increase substantially.

Commercial Fleet Modernization

Ongoing replacement of aging commercial aircraft with newer, more fuel-efficient narrow body and wide body platforms creates strong retrofit and OEM opportunities for air data system manufacturers.

What Is Driving Air Data Systems Market Growth in 2026?

Rising Demand for Precise Flight Data and Real-Time Aircraft Performance Monitoring

The increasing requirement for accurate and real-time flight data is one of the most important structural drivers of the global air data systems market. Modern aircraft operations rely heavily on highly precise measurements of altitude, airspeed, temperature, pressure, and angle of attack to ensure flight safety, fuel efficiency, navigation accuracy, and system reliability. Air data systems provide this critical information to pilots and onboard avionics systems, helping them make real-time operational decisions during takeoff, cruise, descent, and landing. As commercial airlines, cargo operators, business jet owners, and military aviation programs continue prioritizing safety, aircraft performance optimization, and predictive maintenance, the need for reliable air data systems is expanding steadily.

The importance of precise flight data has grown even further with the increasing complexity of modern aircraft. Today’s aircraft are equipped with sophisticated flight management systems, autopilot systems, digital cockpit interfaces, and integrated avionics suites that depend on accurate air data inputs to function effectively. Any deviation in altitude or airspeed calculations can affect route optimization, fuel burn, flight stability, and safety compliance. As a result, airlines and aircraft manufacturers are increasingly investing in high-performance air data computers, advanced sensors, and digital air data modules that can deliver more accurate and continuous readings under varying flight conditions. In both commercial and military aviation, this growing emphasis on operational reliability and flight safety is translating directly into higher adoption of advanced air data systems across new and retrofit aircraft programs.

Air data systems are also gaining importance because they contribute to fault detection and performance optimization. By monitoring pressure, temperature, and airflow characteristics in real time, these systems help pilots and maintenance teams identify anomalies before they escalate into larger mechanical or operational issues. This capability is particularly valuable for airlines and fleet operators focused on reducing unscheduled downtime, improving maintenance planning, and ensuring aircraft remain compliant with strict aviation safety regulations. As the global aviation industry continues to recover and expand, the need for dependable air data solutions that enhance flight accuracy, efficiency, and safety is expected to remain a key market growth driver through 2034.

Increasing Adoption of UAVs Across Military, Surveillance, and Commercial Applications

The rapid expansion of unmanned aerial vehicles (UAVs) is creating a powerful growth opportunity for the air data systems market. UAVs increasingly rely on air data systems to measure airspeed, pressure, temperature, altitude, and atmospheric conditions that influence flight stability and performance. These systems enable UAV operators to maintain better control over flight behavior, improve navigation accuracy, and reduce data entry or performance monitoring errors. As UAVs become more sophisticated and mission-critical across defense, border security, surveying, agriculture, mapping, disaster response, and industrial inspection applications, the need for compact, reliable, and high-precision air data systems continues to rise.

In military applications, UAVs are now used extensively for intelligence, surveillance, reconnaissance, border patrol, and counter-terrorism missions. These missions often require long-endurance flights, high-altitude operations, and precise maneuverability in dynamic weather conditions, making accurate air data measurement essential. Air data systems provide UAV operators and mission control teams with better visibility into flight performance, helping them manage fleet operations more efficiently and safely. In addition, military modernization programs across North America, Europe, Asia-Pacific, and the Middle East are driving procurement of advanced UAV platforms, which directly supports demand for air data sensors, probes, and electronic processing units.

Commercial UAV adoption is also accelerating rapidly, creating a broader addressable market for air data systems. Drones are increasingly used for aerial mapping, surveying, infrastructure inspection, logistics, environmental monitoring, and agriculture. These applications require precise environmental awareness and flight performance data to ensure safe operations and optimal mission execution. Air data systems help drone platforms adjust to temperature fluctuations, wind changes, and altitude variations while improving data collection reliability. As governments continue formalizing drone regulations and as industries expand UAV deployment for cost-efficient operations, the integration of air data systems into both fixed-wing and rotary UAV platforms is expected to become a significant long-term growth engine for the market.

Growing Aerospace Investments and Expansion of Commercial and Military Aircraft Programs

Increasing investment in the aerospace industry is another major factor supporting the growth of the air data systems market. Aircraft manufacturers, avionics suppliers, defense contractors, and governments are investing heavily in next-generation aircraft platforms, fleet modernization programs, and advanced flight technologies. As new commercial, business, and military aircraft are designed with more integrated digital avionics and performance monitoring systems, the demand for high-quality air data systems continues to expand. These systems are now a core part of the broader aircraft instrumentation and flight control ecosystem, enabling reliable flight performance monitoring across civil, cargo, military, and unmanned platforms.

In civil aviation, the expansion of passenger traffic, cargo transportation, and tourism is driving demand for both narrow body and wide body aircraft. Airlines are increasingly seeking aircraft that can deliver better fuel efficiency, lower operating costs, and improved passenger safety. This is creating sustained demand for modern air data systems that can support enhanced performance monitoring, real-time cockpit information, and more efficient flight operations. At the same time, the increasing production of high-capacity aircraft for long-haul passenger and freight transportation is supporting the integration of advanced air data sensors, air data computers, and monitoring modules across aircraft fleets.

Military aviation investment is also contributing significantly to market expansion. Governments worldwide continue increasing defense budgets to procure fighter jets, transport aircraft, surveillance platforms, and UAVs equipped with modern avionics and mission-critical flight systems. Air data systems are essential in these aircraft because they provide real-time insights that support tactical flight performance, navigation, and combat readiness. In addition, research and development spending across aerospace programs is accelerating the introduction of compact, lightweight, and more reliable air data technologies, including digital pressure monitoring systems, integrated sensor probes, and advanced analog-to-digital conversion modules. As aerospace investment remains strong across both civil and defense aviation, the air data systems market is expected to benefit from sustained equipment demand and long-term fleet modernization activity.

Air Data Systems Market Segmentation Analysis

By Component

- Electronic Unit

- Sensors

- Probes

Electronic Unit Represents the Largest Component Segment

Electronic units account for the largest share of the global air data systems market because they serve as the central processing and analytical core of the system. These units collect raw information from sensors and probes, process it through onboard computing logic, and convert it into actionable flight parameters such as airspeed, altitude, temperature, and pressure readings. In modern aircraft, the electronic unit plays a critical role in managing, calculating, and distributing air data to pilots, flight management systems, cockpit displays, and other avionics components. Its ability to improve flight accuracy, detect anomalies, and support safer aircraft operations makes it the most valuable component segment in the market.

The growing use of advanced avionics in commercial and military aircraft is reinforcing demand for more capable electronic units. Airlines and aircraft manufacturers increasingly prefer digital, lightweight, and high-reliability electronic units that can integrate seamlessly with modern flight control architectures. These systems improve data accuracy, enhance fault detection, and support predictive maintenance strategies that reduce operational risk and downtime. As aircraft become more software-driven and performance monitoring becomes more important, electronic units are expected to remain the dominant component category.

Sensors also represent a critical part of the market, as air data systems rely on angle of attack (AOA), total air temperature (TAT), and pressure sensors to measure surrounding air conditions and convert them into electrical signals for analysis. Probes are equally important in capturing environmental and airflow data directly from the aircraft exterior. Together, sensors and probes support the overall effectiveness of air data systems, but the electronic unit remains the central value-creation component because it transforms raw measurements into real-time flight intelligence used across the aircraft.

By Aircraft Type

- Narrow Body Aircraft

- Wide Body Aircraft

- Very Large Aircraft

- Regional Transport Aircraft

- Business Jet

- Fighter Jet

- Military Transport Aircraft

- Rotary Wing Aircraft

- Unmanned Aerial Vehicle (UAV)

Narrow Body Aircraft Dominate the Air Data Systems Market

Narrow body aircraft hold the leading share in the air data systems market due to their widespread use in domestic and short-haul international aviation. These aircraft are heavily deployed by airlines because they offer lower operating costs, better fuel efficiency, and strong suitability for high-frequency passenger routes. Since narrow body aircraft account for a large portion of global commercial aircraft fleets, they also generate substantial demand for air data systems that support safe, efficient, and reliable operations.

Air data systems are especially important in narrow body aircraft because these platforms are often used in dense route networks where operational efficiency, quick turnaround times, and precise flight performance monitoring are essential. As airlines continue modernizing fleets with next-generation narrow body models, the integration of more advanced electronic units, sensors, and probes is expected to strengthen demand in this segment.

Wide body aircraft also represent an important market segment, particularly for long-haul passenger transport and international cargo operations. Very large aircraft, military transport aircraft, and business jets add further demand by requiring highly reliable flight performance systems for specialized missions. In addition, UAVs are becoming an increasingly important aircraft type segment as air data systems gain traction across defense, surveillance, and commercial drone applications.

By End User

- Civil

- Military

Civil Segment Holds the Largest Market Share

The civil segment accounts for the largest share of the air data systems market, primarily due to the steady growth of global passenger air travel, tourism, cargo transportation, and business aviation. Commercial airlines rely on air data systems for safe navigation, real-time cockpit information, and operational efficiency, making these systems indispensable across civil aircraft fleets. The growing demand for new commercial aircraft, combined with increasing passenger volumes and expanding airline networks, is supporting continued adoption of advanced air data systems in this segment.

Rising disposable incomes, international tourism growth, and the expansion of low-cost airline networks are also driving demand for civil aircraft equipped with modern flight monitoring systems. As airlines prioritize safety, fuel efficiency, and fleet modernization, the civil segment is expected to remain the largest end-user category.

The military segment is also growing steadily as defense organizations invest in advanced fighter aircraft, surveillance platforms, transport aircraft, and UAVs. Air data systems in military aviation support tactical flight operations, combat readiness, and mission performance, making them a critical part of next-generation defense aircraft systems.

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

North America Leads the Global Air Data Systems Market

North America holds the leading position in the global air data systems market, supported by its strong aerospace manufacturing ecosystem, rising commercial aircraft production, and growing defense modernization programs. The region benefits from the presence of major aircraft OEMs, avionics manufacturers, and aerospace component suppliers that continue investing in next-generation flight systems and advanced aircraft instrumentation. Increasing air traffic, fleet expansion by commercial airlines, and the need for reliable flight performance monitoring systems are also supporting the widespread deployment of air data systems across civil and military aviation platforms.

The United States remains the primary growth engine within North America due to its extensive commercial aviation network, strong defense expenditure, and ongoing investments in modern aircraft technologies. Aircraft manufacturers and aerospace suppliers in the region are focusing on integrating more advanced air data computers, digital cabin monitoring systems, sensors, and lightweight electronic units into aircraft fleets. In addition, partnerships and collaborations among aerospace companies are helping accelerate innovation in digital flight data systems, cabin pressure monitoring, and next-generation avionics platforms.

Europe represents another important market, supported by strong aircraft manufacturing capabilities, defense aircraft programs, and rising emphasis on aviation safety and performance efficiency. Asia Pacific is expected to witness steady growth as aircraft production expands in countries such as China, India, and Japan, while regional governments continue investing in aviation infrastructure, commercial air travel, and aerospace manufacturing. Latin America and the Middle East & Africa are also gradually expanding their aviation ecosystems, creating incremental demand for air data systems in both civil and defense applications.

Key Regional Insight: North America’s Aerospace Strength Continues to Anchor Market Leadership

North America’s dominance in the air data systems market is closely tied to its deep-rooted aerospace and defense capabilities. The region hosts a mature network of commercial aircraft manufacturers, avionics companies, component suppliers, and defense contractors that collectively support strong demand for advanced flight data technologies. As air traffic volumes continue to grow and fleet modernization remains a strategic priority for airlines and military operators, North America is expected to remain a major revenue contributor to the market through 2034.

The region is also benefiting from rising adoption of digital monitoring technologies, lightweight electronic units, and more integrated avionics platforms across both commercial and military aircraft. In addition, demand for UAVs, surveillance aircraft, and modern transport fleets is strengthening the need for reliable air data systems capable of delivering real-time operational insights. With continued innovation, strong defense budgets, and sustained aircraft production activity, North America is likely to preserve its leadership position in the global market over the forecast period.

Competitive Landscape in the Air Data Systems Industry

The global air data systems market is characterized by a competitive mix of established aerospace suppliers, avionics manufacturers, and specialized aircraft systems providers focused on product innovation, strategic partnerships, and performance enhancement. Companies are increasingly investing in advanced sensing technologies, digital air data computers, lightweight monitoring modules, and integrated avionics systems to strengthen their market position and meet the evolving requirements of commercial and military aviation customers.

A key competitive trend in the market is the development of compact, high-reliability air data systems that combine sensing probes, pressure sensors, electronic units, and digital processing capabilities into more integrated platforms. Manufacturers are also introducing analog-to-digital conversion modules and advanced temperature monitoring systems to improve data accuracy and operational efficiency. In parallel, partnerships with aircraft OEMs and defense contractors are helping market players expand their product portfolios and strengthen long-term supply relationships.

Another important competitive strategy involves the launch of next-generation digital monitoring systems and flight data solutions designed to reduce weight, improve reliability, and simplify aircraft maintenance. As airlines and defense operators increasingly prioritize safety, predictive maintenance, and system integration, companies with strong engineering capabilities and certified aerospace product portfolios are expected to maintain a competitive advantage.

Key Air Data Systems Market Players Include:

- Aeroprobe Corporation

- Ametek Inc.

- Collins Aerospace

- Curtiss-Wright Corporation

- Honeywell International Inc.

- Meggitt (UK) Ltd.

- Shadin Avionics

Latest News and Developments

- 2021: Honeywell International Inc. launched a next-generation digital cabin pressure control and monitoring system for commercial and military aircraft that is lighter, more reliable, and fully electrical.

- January 2023: Meggitt (UK) Ltd. announced a partnership with Airbus to develop an energy buffer (eBuffer) in support of the ZEROe aircraft demonstrator.

- March 2021: Shadin Avionics introduced the AIS-360 LoHi speed converter designed to transmit data at a faster rate and improve aircraft data performance.

People Also Ask

1. What is the current size of the air data systems market?

The global air data systems market reached USD 896.4 Million in 2025 and is projected to grow to USD 1,378.8 Million by 2034, at a CAGR of 4.75% during 2026-2034.

2. What is driving the growth of the air data systems market?

The market is primarily driven by the growing need for precise flight data, rising UAV adoption across defense and commercial applications, and increasing investment in commercial and military aerospace programs.

3. Which region dominates the air data systems market?

North America currently dominates the global air data systems market, supported by strong aerospace manufacturing capabilities, growing aircraft production, and rising defense modernization efforts.

4. Which segment holds the largest share in the air data systems market?

The electronic unit segment leads by component, narrow body aircraft dominate by aircraft type, and the civil segment accounts for the largest share by end user.

5. What are the major trends in the air data systems market?

Key trends include rising integration of digital air data computers, growing deployment in UAVs, increasing adoption of lightweight monitoring systems, and continuous innovation in aircraft sensors, probes, and avionics technologies.

About the Author

IMARC Group is a leading global market research company offering data-driven insights and strategic consulting services across a broad range of industries. The company provides comprehensive research reports covering aerospace, automotive, healthcare, technology, chemicals, consumer goods, packaging, and industrial sectors, helping organizations identify opportunities, evaluate market trends, and make informed business decisions.

Media & Sales Contact

IMARC Group

United States: +1-201-971-6302

India: +91-120-433-0800

United Kingdom: +44-753-714-6104