Overview

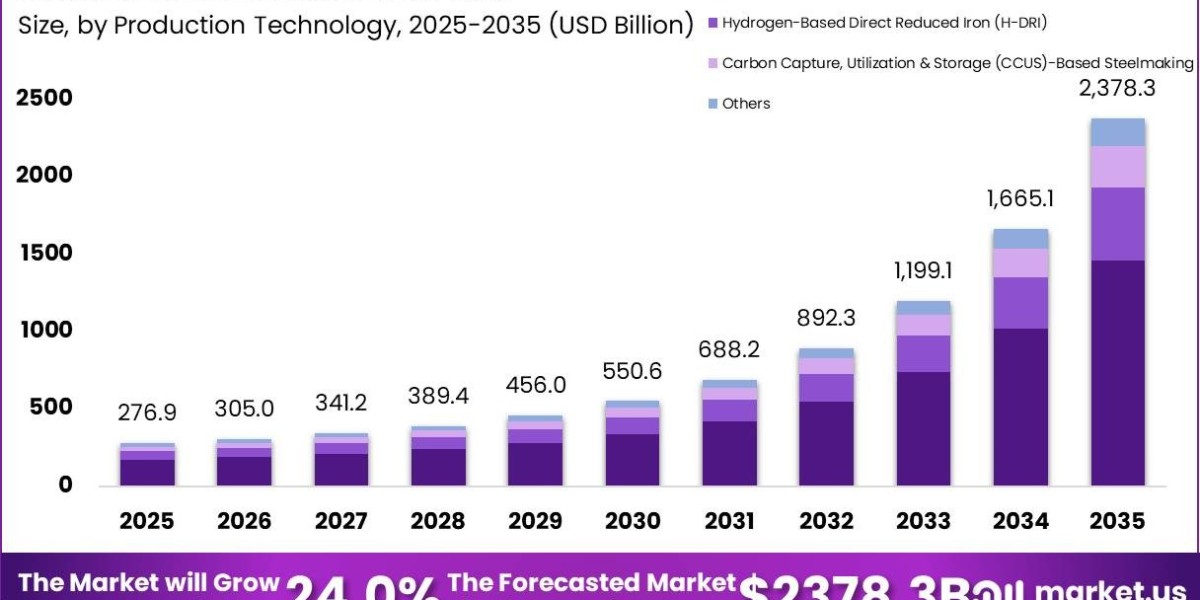

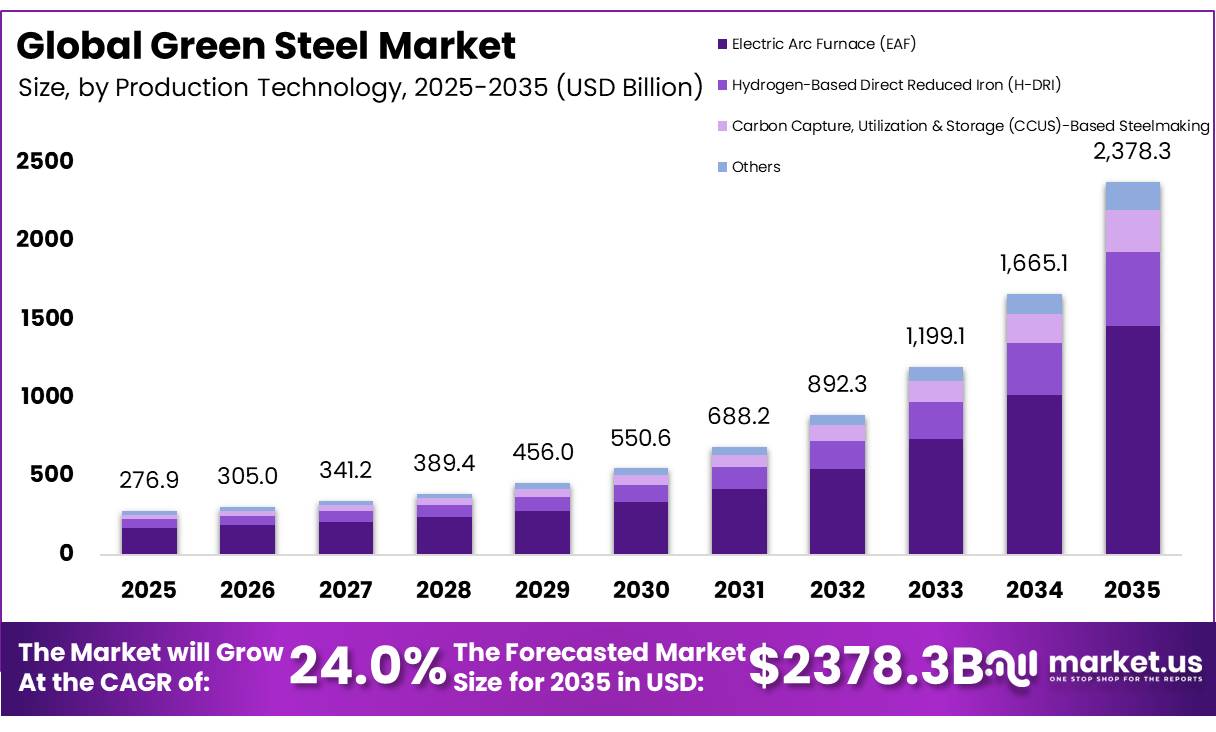

Green Steel Market is gaining momentum as governments and industries focus on reducing emissions from steel production through advanced low-carbon technologies. The market was valued at USD 276.9 billion in 2025 and is estimated to reach USD 2378.3 billion by 2035, expanding at a CAGR of 24.0% during 2026–2035. Europe accounted for a leading position in 2025 with over 39.8% market share and revenue of USD 110.22 Billion. Increasing investment in H₂ DRI-EAF, renewable energy-powered steelmaking, and carbon reduction initiatives is driving long-term market development.

Key Takeaways

- The Global Green Steel market was valued at USD 276.9 billion in 2025.

- The market is projected to grow at a CAGR of 24.0% and is estimated to reach USD 2378.3 billion by 2035.

- By production technology, Electric Arc Furnace (EAF) accounted for a leading 61.4% share of the market in 2025.

- By product type, Flat Steel accounted for a leading 38.6% share of the market in 2025.

- On the basis of end-use industry, Building & Construction accounted for a leading 36.7% share.

- On the basis of region, Europe accounted for a leading 39.8% share of the market in 2025.

Analysis Sections

The Green Steel Market includes the production, commercialization, and end-use adoption of steel manufactured through pathways that eliminate or near-eliminate fossil carbon emissions compared with the traditional blast furnace basic oxygen furnace (BF-BOF) process. The market focuses on low-carbon steel solutions that support industries such as automotive, construction, energy, heavy engineering, and consumer appliances.

According to the International Energy Agency (IEA, 2025), the steel industry requires significant investment in low-emissions production technologies through 2050 as global steel demand continues to grow, with industry forecasts projecting crude steel production of around 2–2.4 billion tonnes annually by mid-century.

In 2025, the world produced approximately 1,849 million tonnes of crude steel and consumed around 1,718.2 million tonnes of finished steel. Rising steel demand and increasing emission reduction requirements are accelerating the adoption of green steel technologies.

Production Technology Type Analysis

Electric Arc Furnace (EAF) represents the dominant segment in the Green Steel Market, accounting for a 61.4% share due to established recycling infrastructure and lower energy requirements compared with primary ore processing.

Recycled steel production requires up to 75% less energy than conventional blast furnace processing, allowing producers to reduce emissions from existing operations without relying on large-scale hydrogen production infrastructure.

According to World Steel Association data, EAFs accounted for 29.1% of global crude steel production. The average carbon intensity of scrap-based EAF steel was approximately 0.70 tonnes of CO₂ per tonne of crude steel, compared with 2.32 tonnes for the conventional blast furnace-basic oxygen furnace route.

Product Type Analysis

Flat Steel is the most widely used green steel product segment, accounting for 38.6% of the Green Steel Market in 2025. The segment is supported by strong demand from the automotive and appliance industries, where hot-rolled, cold-rolled, galvanized, and coated steel products are widely used.

In 2025, the World Steel Association reported that global apparent steel use is expected to reach 75 billion tonnes, with manufacturing industries remaining major consumers of flat steel products.

Long steel products, including structural beams, rebar, and wire rods, are expected to expand significantly between 2026 and 2035 due to policies promoting environmentally friendly materials in public projects and building codes requiring low-carbon materials.

End Use Industry Analysis

The Building & Construction sector represents the leading end-use industry segment in the Green Steel Market, accounting for 36.7% share. Growth is supported by increasing adoption of green building standards such as LEED and BREEAM and stricter carbon requirements across various countries. The Global Status Report for Buildings and Construction (UNEP/Global ABC) stated that the buildings and construction sector accounts for around 34% of global energy demand and 37% of energy- and process-related CO₂ emissions, highlighting the need for low-carbon materials such as green steel.

Key Market Segments

Production Technology

- Electric Arc Furnace (EAF)

- Hydrogen-Based Direct Reduced Iron (H-DRI)

- Carbon Capture, Utilization & Storage (CCUS)-Based Steelmaking

- Others

Product Type

- Flat Steel

- Long Steel

- Structural Steel

- Reinforcement Steel (Rebar)

- Others

End User Industry

- Building & Construction

- Automotive & Transportation

- Energy & Power

- Industrial Equipment

- Heavy Engineering

- Consumer Appliances

- Defense & Aerospace

- Others

Driving Factors

Automotive OEM Scope 3 mandates and green steel offtake agreements are major growth drivers for the Green Steel Market. Steel contributes 30–70% of a vehicle’s Scope 3 embedded emissions depending on model architecture, making it a major decarbonization focus for automotive manufacturers.

The automotive sector accounts for approximately 40% of green steel end-use demand in 2026, making it a major commercial demand catalyst. Volkswagen Group, Mercedes-Benz, BMW, and Volvo Cars have publicly committed to sourcing low-carbon or green steel as part of their Scope 3 emissions reduction strategies. Mercedes-Benz took an equity stake in H2 Green Steel in May 2021 to strengthen supply chain positioning.

Restraining Factors

The prohibitive CapEx burden and project financing bottlenecks remain major challenges for green steel adoption. Converting 30% of Europe’s listed steelmakers’ crude steel production to the H₂-DRI/EAF route requires between EUR 12.1 billion and EUR 20.2 billion in total capital investment.

First-of-kind H₂-DRI/EAF projects face financing challenges due to technology execution risk, hydrogen supply price risk, and offtake concentration risk. The weighted average cost of capital for project finance is estimated at 9–13% in Europe compared with 6–8% for equivalent BF-BOF brownfield capex.

Growth Opportunity

Carbon credit monetization through India’s live CCTS market presents a significant growth opportunity for the Green Steel Market. For a mid-sized integrated steel plant producing 2 MT/year that reduces emission intensity by 0.5 tCO₂e/tfs above its CCTS target, annual carbon credit generation is approximately 1 Mt CO₂e.

At an ICM exchange price of INR 800–1,200/tCO₂e, this represents INR 800–1,200 crore in incremental annual revenue per plant, improving the financial attractiveness of green steel projects. As of mid-2026, only 89 certified steel units have been awarded green steel status covering 12.34 MT of production, leaving opportunities for additional producers to achieve certification through process upgrades and renewable energy procurement.