Overview

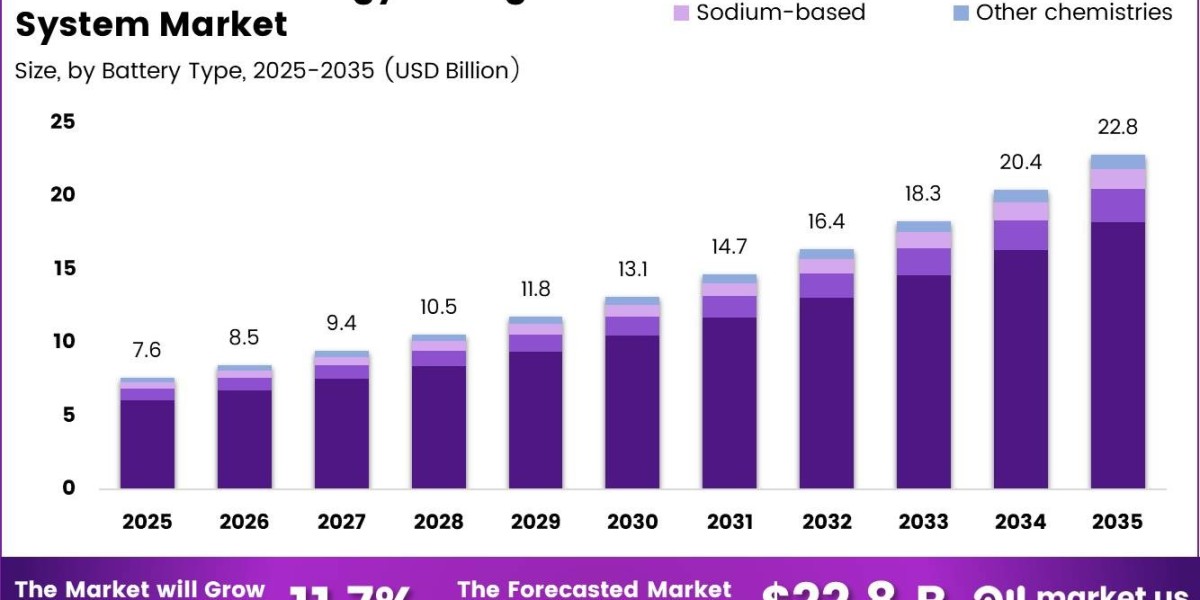

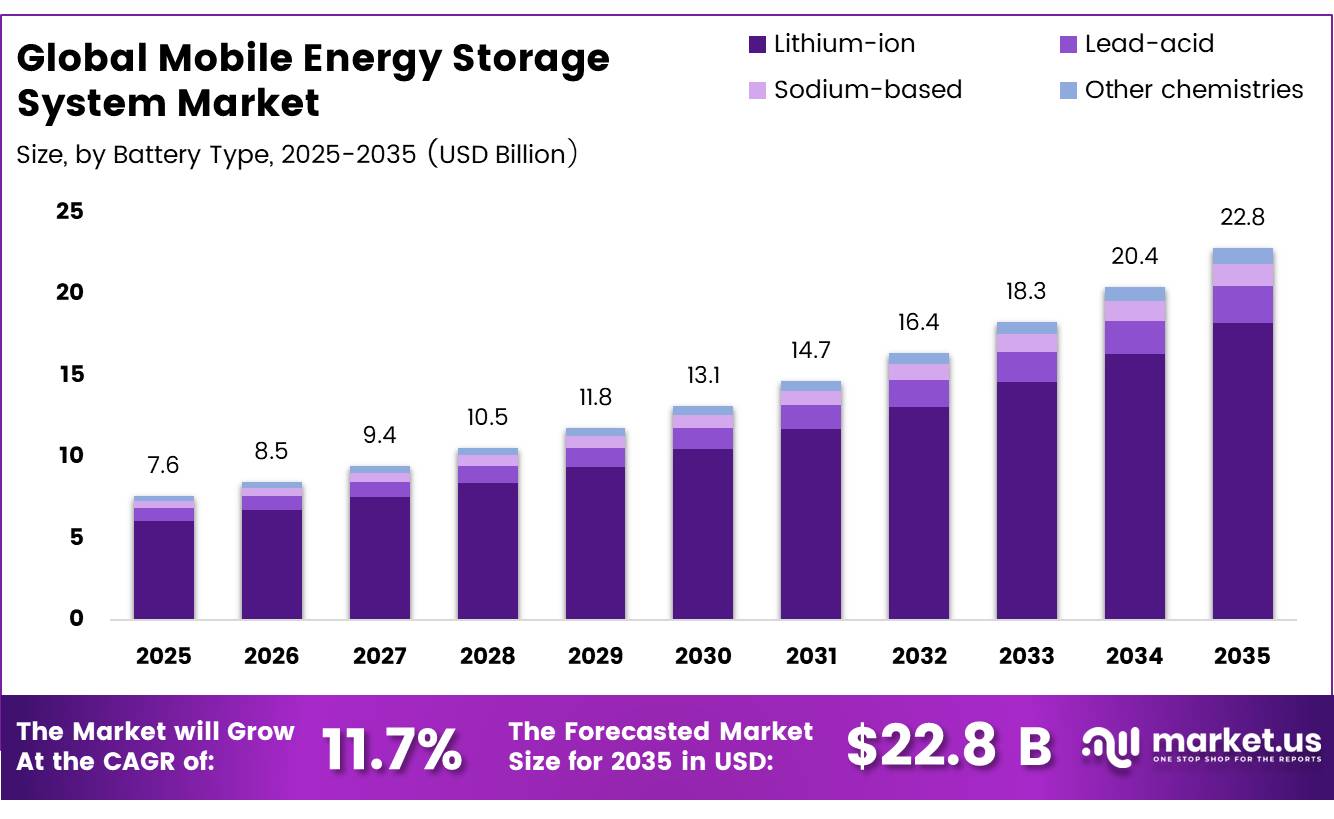

The Mobile Energy Storage System Market is expanding rapidly due to increasing demand for portable and scalable energy solutions. Valued at USD 7.6 billion in 2025, the market is expected to reach approximately USD 22.8 billion by 2035, registering a CAGR of 11.7% from 2026 to 2035. Growth is supported by battery cost reductions, renewable energy integration, EV charging expansion, and the need for dependable temporary power solutions. North America captured the highest market share of 30.1% in 2025.

Key Takeaways

- The Global Mobile Energy Storage System Market was valued at USD 7.6 billion in 2025.

- The global Mobile Energy Storage System Market is projected to grow at a CAGR of 11.7% and is estimated to reach USD 22.8 billion by 2035.

- Based on Battery Type, Lithium-Ion (Li-Ion) dominated the market, accounting for 79.9% of the total market share.

- Based on Power Capacity, the 100–500 kW / 3,000–10,000 kWh segment dominated the Mobile Energy Storage System Market, accounting for approximately 45.1% of total revenue.

- Based on Source, Trailer-mounted systems led the market, accounting for approximately 45.4% share.

- Among Applications, C&I peak-shaving / temporary power held the largest share in the Mobile Energy Storage System Market, representing 30.3% of the market.

- In 2025, North America was the dominant region in the Mobile Energy Storage System Market, accounting for 30.1% of the global market with revenue of USD 2.3 billion.

Battery Type Analysis

Lithium-Ion (Li-Ion) Mobile Energy Storage System Represents Dominant Segment

Lithium-Ion (Li-Ion) batteries maintained the leading position in the Mobile Energy Storage System Market, accounting for 79.9% of total market share due to their high performance, declining costs, and extensive application across electric mobility and mobile power solutions. According to the International Energy Agency, the energy sector represented more than 90% of annual lithium-ion battery demand, compared with 50% in 2016. Lithium-ion batteries provide an energy density of approximately 150–250 Wh/kg, significantly higher than the less than 40 Wh/kg offered by lead-acid batteries.

This advantage makes them suitable for electric vehicles, portable industrial equipment, mobile charging units, and field-based power systems. Global battery demand exceeded 1 TWh in 2024, while EV battery demand surpassed 950 GWh, increasing 25% year over year. In 2025, global lithium-ion battery deployment reached 6 times the level recorded in 2020, with electric vehicles accounting for more than 70% of deployments. Battery pack prices also declined below USD 100/kWh in 2024 after falling nearly 90% since 2010. Lead-acid batteries continue to maintain a smaller but stable position, especially in UPS, telecom backup, and industrial standby systems. Their advantages include mature recycling infrastructure and lower initial costs. The U.S. EPA reported a 99.3% recycling rate, while the U.S. Department of Energy reported recycling rates above 99%. New lead-acid batteries can contain around 80% recycled material. These factors support their approximately 10% share in the Mobile Energy Storage System Market, although lower energy density limits their growth in mobile applications.

Power Capacity Analysis

100–500 kW / 3,000–10,000 kWh Segment Leads the Market

In 2025, the 100–500 kW / 3,000–10,000 kWh capacity segment held a dominant position in the global Mobile Energy Storage System Market, accounting for approximately 45.1% of total revenue. Its growth is supported by demand from commercial and industrial users, including manufacturing plants, logistics centers, data centers, EV charging sites, and large commercial facilities. Global battery storage additions reached 108 GW in 2025, increasing 40% year over year and nearly 11 times compared with 2021. Battery projects focused on energy shifting increased from around 40% in 2015 to more than 90% in 2025, highlighting the growing value of storing lower-cost electricity and using it during peak demand periods.

Global electricity demand is expected to exceed 29,000 TWh by 2026, supported by industrial electrification, data center expansion, and growing EV charging infrastructure. The COP29 pledge targets 1,500 GW of global energy storage capacity by 2030, while long-term storage requirements are projected to increase from 416 GW in 2025 to 2,530 GW by 2035. Battery costs have declined by 93% since 2010, reaching approximately USD 192 per kWh in 2024, improving affordability for medium-capacity mobile storage systems. The Less than 100 kW / under 3,000 kWh category remains the fastest-growing segment by deployment volume. Demand is increasing across SMEs, telecom towers, construction sites, remote communities, humanitarian operations, and smaller backup power applications. Australia’s behind-the-meter battery additions increased from nearly 0.2 GW in 2024 to approximately 3.4 GW in 2025, while the United States added close to 3 GW. Battery-based UPS capacity also increased by 30% to reach 45 GW in 2025.

Source Analysis

Trailer-Mounted Systems Lead Mobile Energy Storage Deployment

Trailer-mounted systems led the global Mobile Energy Storage System Market with an estimated 45.4% share due to easy transportation, rapid installation, and broad usage across construction, utilities, defense, and emergency services.

Global battery energy storage deployments reached a record 108 GW in 2025, increasing 40% year over year, while cumulative capacity expanded to more than 11 times the 2021 level. This growth is increasing demand for movable power solutions that avoid permanent infrastructure requirements. The global construction industry is projected to increase from US$11.39 trillion in 2024 to US$16.11 trillion by 2030, supporting demand for temporary and remote-site electricity solutions. Disaster-response requirements also contribute to market expansion, with direct global disaster losses estimated at nearly US$202 billion annually. In the United States, 10.4 GW of battery storage capacity was added in 2024, increasing cumulative utility-scale capacity above 26 GW. Self-driving and vehicle-integrated systems represent the fastest-growing segment. U.S. utility-scale storage capacity is projected to approach 65 GW by the end of 2026. AI-based energy arbitrage represented more than 90% of BESS project applications in 2025, supporting increased adoption of automated mobile storage solutions.

Application Analysis

C&I Peak-Shaving / Temporary Power Holds Major Market Share

C&I peak-shaving / temporary power represented the leading application segment in the Mobile Energy Storage System Market, accounting for 30.3% share. Growth is supported by rising electricity demand, grid congestion, increasing commercial tariffs, and demand for flexible energy solutions. Global electricity demand increased by 4.3% in 2024 and is expected to grow by nearly 4% annually through 2027. Major contributors include warehouses, manufacturing plants, data centers, and logistics hubs. Mobile battery energy storage systems help reduce electricity costs by supplying stored power during peak-use periods. Global battery storage additions reached 108 GW in 2025, increasing 40% year over year. Additionally, 97.5% of commercial facilities experienced electricity-rate increases between 2020 and 2025, with a median annual growth rate of 5.9%, compared with the 3% increase commonly assumed in corporate energy budgets. For a typical 1 MW commercial load, annual capacity-related charges could increase from approximately US$10,000 in 2024 to more than US$120,000 by 2027. Mobile storage systems also support temporary EV fast charging. Global EV sales reached 17 million units in 2024 and 21.6 million units in 2025, representing approximately 1 in 4 new cars.

Key Market Segments

By Battery Type

- Lithium-Ion (Li-Ion)

- Lead Acid

- Sodium‑based

- Others Chemistries

By Power Capacity

- 100–500 kW / 3,000–10,000 kWh

- Less than 100 kW / <3,000 kWh

- Above 500 kW / >10,000 kWh

By Source Water

- Trailer‑mounted systems

- Standalone containerized solutions

- Self‑driving / vehicle‑integrated systems

By Application

- Construction sites and mining

- C&I peak‑shaving / temporary power

- On‑demand EV fast charging

- Events, disaster relief, remote/off‑grid

- Data centers and critical infrastructure

Driving Factors

Battery Cost Deflation Unlocking Mass-Market MESS Economics

According to BNEF data released in December 2025, the global average lithium-ion pack price reached a record low of USD 108/kWh, declining 8% from USD 115/kWh in 2024 and more than 93% below 2010 levels. Stationary storage segment prices reached USD 70/kWh in 2025, representing a 45% decline from the previous year. LFP chemistries averaged USD 81/kWh compared with USD 128/kWh for NMC packs, encouraging mobile energy storage developers to adopt cost-efficient battery technologies. These cost reductions have shortened project payback periods from 10–12 years to approximately 6–8 years in grid-service applications, supporting broader deployment of containerized and trailer-mounted systems.

Restraining Factors

Tightening Battery Regulatory Compliance and EPR Rules

The EU Battery Regulation (EU) 2023/1542 entered its enforcement phase in February 2026, introducing carbon-footprint declaration requirements for rechargeable industrial batteries above 2 kWh. By 2026, the regulation requires at least a 45% collection rate for portable batteries, increasing toward 73% by 2030. From late 2027, recovery requirements shift toward material recovery efficiency, including 90% recovery targets for cobalt, copper, lead, and nickel. The regulation also requires a digital battery passport for all EV and industrial batteries above 2 kWh by February 2027, requiring advanced battery management systems, cybersecurity infrastructure, and lifecycle data management.

Growth Opportunity

Second-Life Packs and Circular MESS Fleets

Second-life battery applications represent a major growth opportunity for the Mobile Energy Storage System Market. Companies such as Redwood Materials are directing some retired EV batteries toward stationary storage instead of direct recycling.

Battery packs retired from high-demand applications with 70–80% state of health can still support lower power-density applications including microgrids, festival power systems, and backup infrastructure. By 2030, tens of GWh of EV batteries are expected to reach end-of-first-life globally. Even if only 20–30% of this volume becomes technically and economically reusable, the available second-life battery pool could exceed cumulative mobile energy storage capacity deployed to date, creating new opportunities for circular mobile storage fleets.