Overview

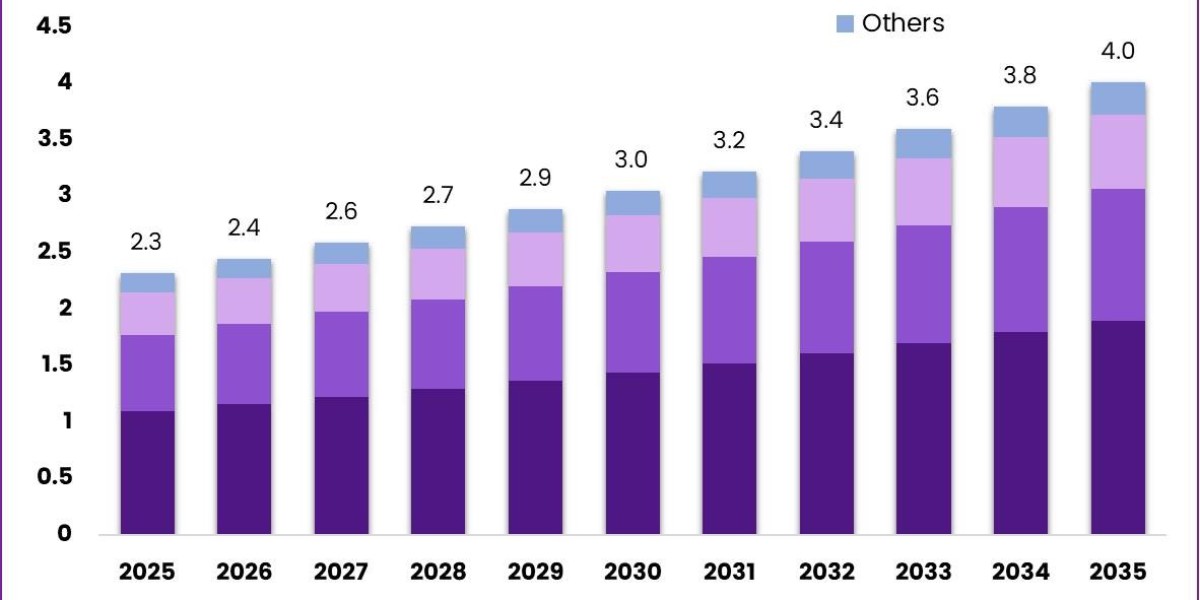

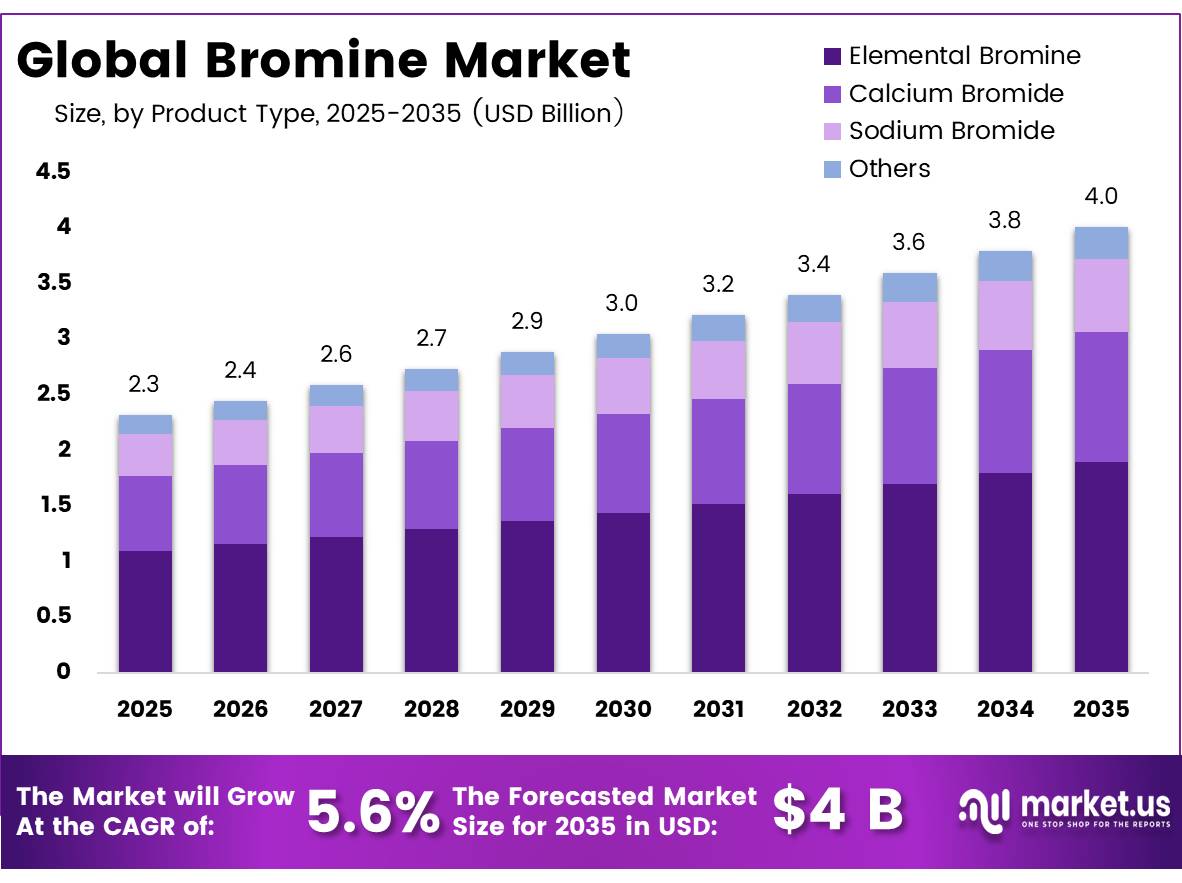

Bromine Market reached USD 2.3 billion in 2025 and is forecast to attain USD 4 billion by 2035, registering a CAGR of 5.6% over 2026–2035. In 2025, Europe accounted for more than 42.7% of the market, generating USD 0.99 billion in revenue. The UN Global E-waste Monitor 2024 reported 62 million metric tons of e-waste in 2022, projected to reach 82 million metric tons by 2030. Europe's construction sector employs around 15 million people and contributes nearly 10% of regional GDP. Global bromine production increased from approximately 400,000 metric tons in 2024 to nearly 430,000 metric tons in 2025. Israel expanded production from approximately 140,000 metric tons to 200,000 metric tons, while China maintained output of around 90,000–100,000 metric tons. Global upstream oil and gas investment exceeded US$600 billion in 2024, and coal accounts for more than 40% of worldwide electricity generation.

Key Takeaways

- The global Bromine Market was valued at USD 2.3 billion in 2025.

- The market is projected to grow at a CAGR of 5.6% and reach approximately USD 4 billion by 2035.

- By product type, Elemental Bromine accounted for 47.3% of the global market.

- By form, Liquid Bromine held the largest share at 81.9%.

- By end-user industry, the Chemical segment represented 31.8% of total market demand.

- In 2025, Europe held a dominant market position with a 42.7% market share and USD 0.99 billion in revenue.

Product Type Analysis

Elemental Bromine remained the leading product segment, accounting for 47.3% of the global market. Its dominance is attributed to its role as the primary raw material used to manufacture nearly all bromine derivatives. It serves as the foundation for brominated flame retardants, clear brine drilling fluids, water treatment chemicals, and numerous industrial intermediates. Strong demand from electronics manufacturing, construction materials, and oil and gas drilling continues to reinforce its leading market position.

According to the USGS Mineral Commodity Summaries 2026, brominated flame retardants and clear brine fluids remain the largest global applications for bromine. Global bromine production reached approximately 440,000 metric tons in 2024, with Israel producing about 190,000 metric tons, making it the world's largest producer. U.S. imports of bromine and bromine compounds totaled 58,300 metric tons in 2024, while Israel supplied approximately 89% of these imports through mid-2025.

Growing oil production also supports demand for bromide-based completion fluids. According to the U.S. Energy Information Administration (EIA), U.S. crude oil production averaged 13.4 million barrels per day in 2024 and increased to 13.6 million barrels per day in 2025, while active producing wells reached 918,481 and the Permian Basin produced 6.6 million barrels per day. These developments continue to increase demand for calcium bromide solutions used in high-pressure and high-temperature drilling operations.

Form Analysis

Liquid Bromine dominated the market with an 81.9% share due to its unique physical property as the only non-metallic element that remains liquid at room temperature. This characteristic makes it highly suitable for industrial processing, transportation, and a broad range of manufacturing applications.

The majority of bromine-consuming industries, including brominated flame retardants and clear brine drilling fluids, primarily utilize bromine in liquid form. Global production reached approximately 440,000 metric tons in 2024, led by Israel (190,000 MT), Jordan (112,000 MT), and China (100,000 MT). Additionally, U.S. imports of bromine and bromine compounds reached 58,300 metric tons during 2024, with liquid bromide solutions accounting for most traded volumes.

The increasing adoption of bromine-based mercury emission control technologies, capable of achieving mercury reduction efficiencies exceeding 90%, along with expanding electronics manufacturing and stricter fire safety regulations, is expected to sustain strong demand for both liquid bromine and downstream solid bromine compounds over the forecast period.

End User Analysis

The Chemical industry represented the largest end-use segment, accounting for 31.8% of global bromine consumption. Bromine serves as a critical feedstock for brominated flame retardants, industrial intermediates, water treatment chemicals, and numerous specialty chemicals.

According to the U.S. Geological Survey (USGS), bromine production increased from approximately 395,000 metric tons in 2023 to about 400,000 metric tons in 2024, reflecting steady industrial demand. Bromine is widely used in the production of Tetrabromobisphenol-A (TBBPA) and Decabromodiphenyl Oxide, which are essential for electronics, printed circuit boards, construction materials, and textiles.

The American Chemistry Council (ACC) reported global chemical production growth of 3.5% in 2024, with an additional 3.1% increase expected in 2025, supporting continued bromine consumption across industrial manufacturing.

The oil and gas industry remains the fastest-growing end-use segment as deepwater and high-pressure drilling activities expand. According to the EIA, crude oil production in the Gulf of America reached 1.77 million barrels per day in 2024 and is projected to increase to 1.80 million barrels per day in 2025 and 1.81 million barrels per day in 2026, while 13 new offshore fields are expected to begin production during 2025–2026.

Key Market Segments

By Product Type

- Elemental Bromine

- Calcium Bromide

- Sodium Bromide

- Others

By Form

- Liquid Bromine

- Bromine Powder

By End User Industry

- Chemical

- Oil & Gas

- Electronics & Electrical

- Construction

- Automotive

- Healthcare & Pharmaceuticals

- Agriculture

- Energy & Utilities

- Textile

- Others

Driving Factors

Growing investment in renewable energy and stationary energy storage systems is creating new opportunities for bromine derivatives. Increasing deployment of battery energy storage systems between 2025 and 2035 is encouraging the adoption of alternative chemistries such as bromine-based flow batteries, particularly where safety, long cycle life, and extended storage duration are critical.

Bromine producers can expand beyond traditional commodity applications by supplying electrolyte solutions, partnering with energy storage manufacturers, and developing integrated battery platforms. These strategies provide opportunities to secure long-term supply agreements while benefiting from the rapid expansion of global stationary energy storage infrastructure.

Restraining Factors

The global bromine industry remains highly dependent on geographically concentrated brine resources located primarily in Israel, Jordan, China, and limited production areas in the United States and India. This concentration increases supply chain risks and exposes the market to production disruptions, geopolitical uncertainty, transportation issues, and price volatility.

During 2025–2026, bromine prices in China rose sharply due to reduced domestic output, environmental inspections, declining inventories, and uncertain Middle East supply conditions. These fluctuations increase raw material costs for downstream manufacturers, encourage product reformulation, and support the search for substitute materials, limiting long-term market expansion.

Growth Opportunity

The expansion of zinc-bromine, vanadium-bromine, and hybrid bromine flow battery technologies presents a significant long-term growth opportunity for the Bromine Market.

By developing flow battery technologies, securing long-term utility contracts, and offering energy storage solutions alongside bromine supply, producers can move beyond commodity sales into higher-value infrastructure markets. If even 5–10% of global stationary energy storage installations adopt bromine-based technologies by 2035, integrated market participants could benefit from meaningful additional bromine demand and stronger long-term revenue growth.