A mortgage calculator is a valuable instrument that helps prospective homeowners determine their regular mortgage obligations based on numerous factors. By inputting details like the loan amount, interest rate, loan expression, and sometimes property fees or insurance premiums, the calculator may quickly estimate exactly what a borrower can expect to pay for each month. This instrument is especially useful for first-time homebuyers who might not have a definite comprehension of how mortgage obligations are structured or what they are able to afford. By using a mortgage calculator, people may gain a clearer picture of the financial obligations and greater plan their budget accordingly.

The principal purpose of a mortgage calculator is always to determine the regular payment. Including not only the primary and interest but may also integrate additional charges like house fees, homeowners insurance, and actually personal mortgage insurance (PMI) if the borrower puts down significantly less than 20% of the home's value. These additional expenses can considerably influence the full total monthly cost, so it's important to factor them in when assessing affordability. Some sophisticated mortgage calculators actually let consumers to account for homeowners association (HOA) fees, which can differ with regards to the neighborhood.

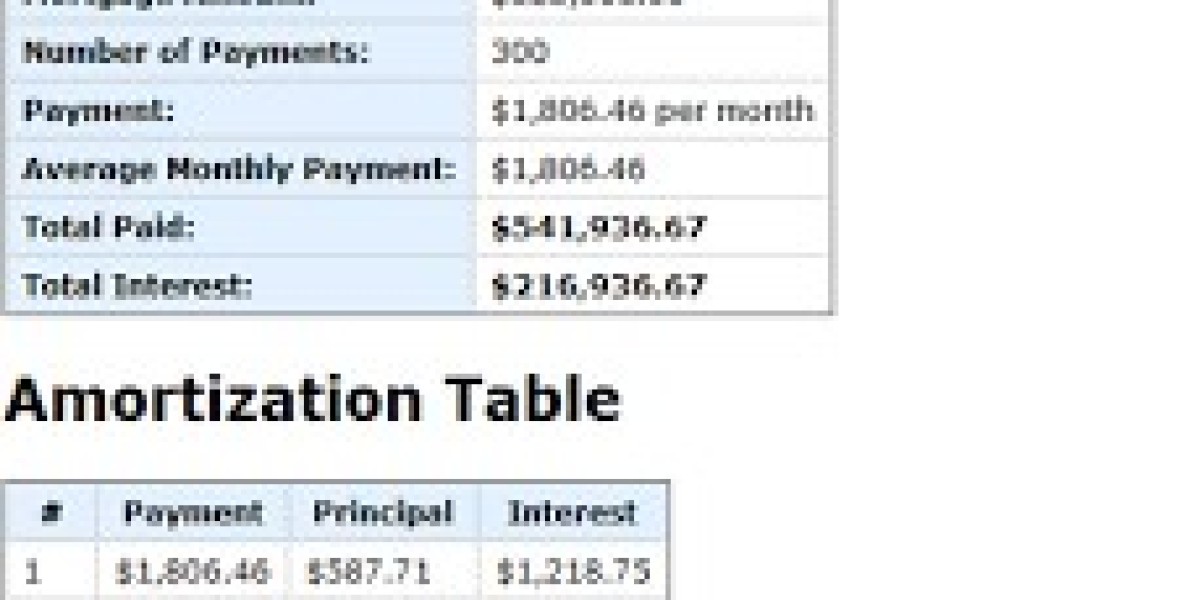

Understanding how a regular payment is damaged down is yet another critical benefit of using a mortgage calculator. In early decades of a loan, a larger part of the payment goes toward curiosity rather than principal. With time, however, the principal portion raises since the loan harmony decreases. A mortgage calculator often provides an amortization schedule, which shows this dysfunction over living of the loan. This assists borrowers know how significantly of these regular payment is going toward reducing the loan balance, and how much is essentially only spending the lender for the usage of their money.

Among the main factors in determining mortgage obligations could be the fascination rate. The rate at which the loan is financed straight affects simply how much a borrower will probably pay over the life of the loan. Small changes in fascination prices may have a large impact on monthly payments. For instance, a greater fascination rate raises the expense of borrowing, indicating larger regular payments and more compensated in curiosity around time. Alternatively, a lowered charge decreases the monthly payment and the overall charge of the mortgage. Mortgage calculators let customers to try with different curiosity costs to see how changes will impact their payments.

Mortgage calculators may also be ideal for comparing different loan options. For example, a borrower may choose to assess the regular cost on a 15-year loan versus a 30-year loan. The monthly payment for a 15-year mortgage may an average of be larger because of the shorter repayment time, but the total interest paid over living of the loan will undoubtedly be lower. With a mortgage calculator, borrowers can mimic different scenarios and decide which loan expression most readily useful fits their budget and long-term economic goals.

Along with helping borrowers determine obligations, mortgage calculators also can function as something for qualifying for a loan. Lenders frequently use specific requirements, like debt-to-income percentage (DTI), to assess whether a borrower are able a mortgage. A mortgage calculator provides an estimate of the borrower's DTI by factoring in their money and monthly debt obligations. By inserting inside their revenue and Mortgage Calculator debts, consumers can easily see if they meet the normal DTI demands for certain loan.

Another function that many mortgage calculators contain is the capacity to estimate just how much a borrower are able to afford based on the ideal monthly payment. This really is ideal for audience who've a group budget in your mind but aren't positive how much home they can afford. By inputting a goal monthly cost, the calculator can back-calculate the loan amount they might qualify for, factoring in the expected curiosity charge and loan term. This provides customers a notion of the purchase price selection they must be contemplating when shopping for a home.

Eventually, mortgage calculators aren't just for homebuyers—they're also ideal for homeowners that are contemplating refinancing their existing mortgage. A refinance mortgage calculator can help determine the impact of refinancing on monthly obligations, interest prices, and the sum total loan term. It may also show whether refinancing will save you money in the long term or whether the expenses of refinancing outnumber the benefits. With the capability to regulate loan terms and fascination costs, homeowners can examine whether refinancing is really a financially sound decision based on the recent

![[2023 To 2030] DIN 2353 Tube Fittings Market Size, Trend, Research Report](https://zekond.s3.amazonaws.com/upload/photos/2023/11/AkVsQRyd9Yqf3b81RqyQ_15_43f666e31c60d553a27e8939391c9afb_image.jpg)